A Tale of Two Markets During a Rate Hike Cycle

Bonds and Term Deposits: How Do Interest Rates Affect Fixed-Income Investments?

For conservative investors who prefer fixed-income investments, the impact of interest rate changes is straightforward. As market interest rates rise, newly issued bonds and term deposits offer more attractive yields. Consequently, existing bonds with lower coupon rates become less attractive, causing their prices to fall. This is why bond prices move inversely to interest rates. For investors holding cash or approaching investment maturity, a rate hike cycle presents an opportunity to allocate funds into higher-yielding term deposits or bond investments.

How Australian Interest Rate Policy Affects Household and Personal Finances

Beyond the broader housing and investment markets, every RBA interest rate decision ultimately reaches household budgets, directly influencing savings, debt, and the relationship between interest rates and the cost of living.

Savings and Deposits: Will Your Bank Interest Earnings Increase or Decrease?

This is one of the most immediate benefits of rising interest rates. When the RBA raises rates, commercial banks generally increase the interest paid on savings accounts and term deposits to attract deposits. For conservative savers, this means their money earns higher returns, helping offset the erosion of purchasing power caused by inflation. After years of historically low interest rates, the relatively higher rate environment in 2026 has made savings accounts more attractive once again.

Credit Cards and Personal Loans: Changes in Your Borrowing Costs

Higher interest rates benefit savers but create additional burdens for borrowers. Credit card interest rates, car loans, and personal loans generally rise alongside official interest rates. This means individuals carrying credit card balances or personal debt face higher interest expenses and greater repayment pressure. During a rate hike cycle, managing and reducing high-interest debt becomes one of the most important personal financial priorities.

Cost of Living: How Do Interest Rates Indirectly Affect Inflation and Consumer Prices?

The RBA adjusts interest rates primarily to control inflation. The logic behind raising rates is simple: by increasing borrowing costs, business investment and consumer spending slow, cooling an overheated economy and easing upward pressure on prices. As households reduce spending due to higher mortgage repayments and more expensive borrowing, overall demand declines, making it harder for businesses to continue raising prices. Although this process takes time, it ultimately shows up in the Consumer Price Index (CPI). In essence, every RBA interest rate decision represents an ongoing effort to balance inflation control with sustainable economic growth.

Recommended Reading

Your Money Is Losing Value! Understanding How Inflation Affects the Purchasing Power of the Taiwan Dollar and Wealth Preservation

A Beginner’s Guide to Commodity Investing: Understanding Futures Trading, Volatility, and Inflation Protection

A Different Perspective: Opportunities and Challenges Across Industries

Fluctuations in interest rates and exchange rates create very different outcomes across industries. Some sectors may benefit from favorable conditions, while others face significant headwinds. Understanding these differences provides a deeper insight into the broader Australian economy.

Importers vs. Exporters: The Impact of a Stronger or Weaker Australian Dollar

The key issue here is the Australian dollar’s exchange rate. As discussed earlier, higher interest rates generally support the Australian dollar. For importers, a stronger Australian dollar is good news because it allows them to purchase more foreign currency with the same amount of Australian dollars, reducing the cost of importing goods and improving profit margins. For exporters (such as those in mining, agriculture, and tourism), the opposite is true. A stronger Australian dollar makes Australian products and services more expensive in international markets, reducing price competitiveness, potentially lowering demand, and weighing on revenue.

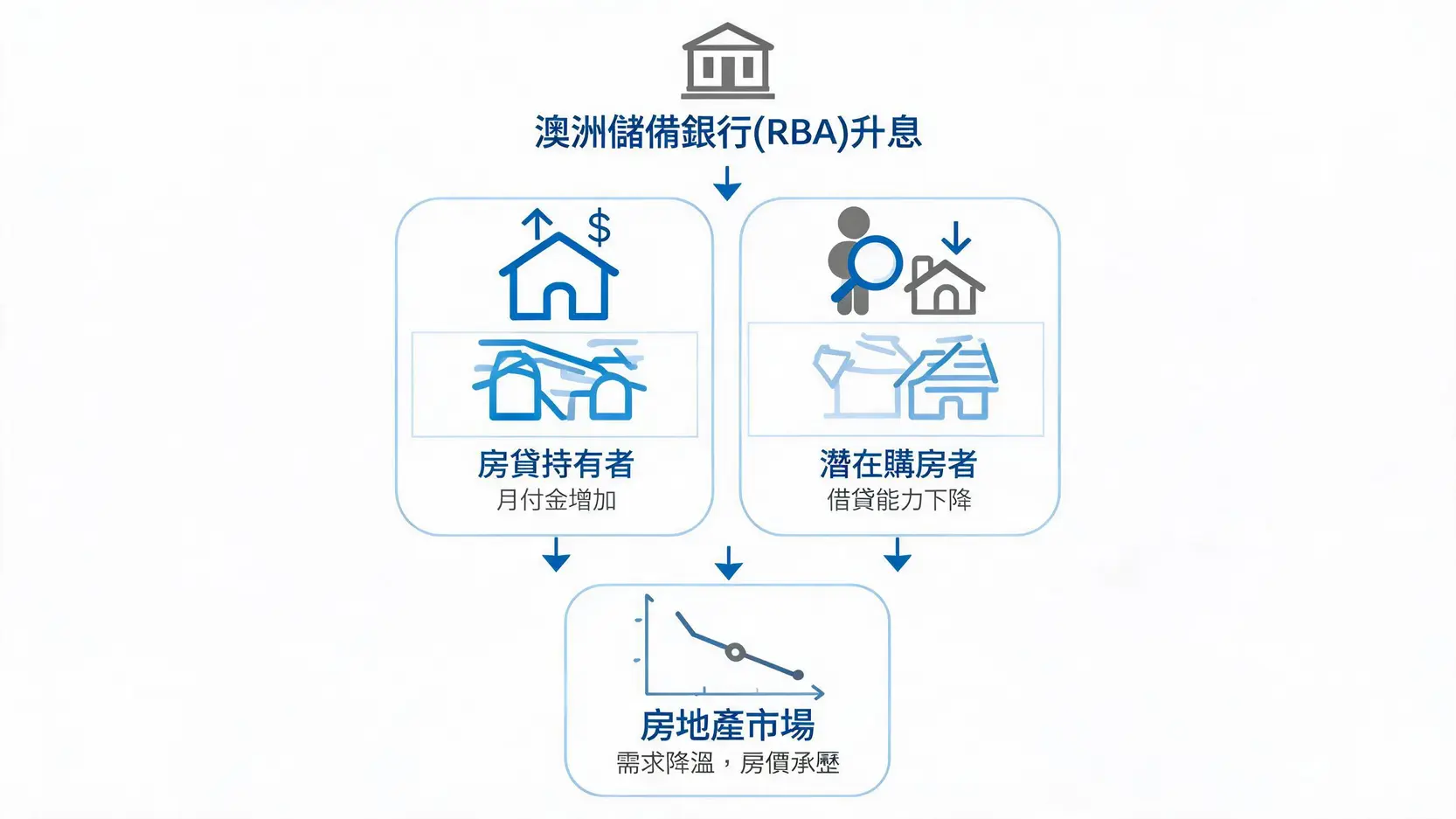

Construction and Retail: The Relationship Between Consumer Spending and Business Activity

Construction is one of the most interest rate-sensitive industries. Higher interest rates increase financing costs for developers while reducing demand from homebuyers, leading to fewer new housing starts and development projects. The retail sector, particularly discretionary spending categories (such as luxury goods, consumer electronics, travel, and entertainment) is directly affected by household disposable income. As mortgage repayments and other borrowing costs consume a larger share of household income, consumers naturally reduce non-essential spending, placing direct pressure on retail sales.

Banking: How Higher Interest Rates Affect Bank Profits

As mentioned earlier, the banking sector is typically one of the relative winners during a rate hike cycle. Its core business model, taking deposits and issuing loans, benefits directly from wider net interest margins. As long as the economy avoids a severe downturn that triggers widespread loan defaults, higher interest rates generally have a direct and positive impact on bank profitability. This is one reason why financial stocks often enjoy favorable market sentiment whenever the RBA is considering further rate hikes.

Conclusion

Overall, changes in Australian interest rates act as a highly precise economic policy tool, influencing virtually every aspect of the economy. Their impact is broad and far-reaching. Interest rates are not only a key driver of the Australian dollar but also a major force shaping mortgage repayments, stock market performance, and household spending. Whether you are a mortgage holder, a domestic or international investor, or an everyday consumer, understanding how these effects are transmitted throughout the economy is essential. Against the backdrop of a still challenging global economic environment in 2026, thorough analysis and careful preparation will help you protect and grow your wealth across different interest rate cycles while making financial decisions that best suit your circumstances.

Frequently Asked Questions (FAQ)

Q: Should I Choose a Fixed-Rate Mortgage When Interest Rates Are Rising?

A: It depends on your expectations for future interest rates and your tolerance for risk. Locking in a reasonable fixed interest rate early in a rate hike cycle can protect you from further increases and keep your monthly repayments stable. However, fixed-rate loans offer less flexibility, and if interest rates unexpectedly fall, you will not benefit from lower borrowing costs. A strategy that combines fixed and variable rates may provide a useful “hedge” strategy.

Q: Do Australian Interest Rates Affect My Overseas Investments?

A: Yes, primarily through exchange rates. RBA interest rate decisions directly influence the value of the Australian dollar. If your overseas assets are denominated in foreign currencies (such as the US dollar or Malaysian ringgit), a stronger Australian dollar means those assets will convert into fewer Australian dollars, and vice versa. Investors with international portfolios should therefore factor exchange rate risk into their investment decisions.

Q: What Is the Best Financial Strategy During Periods of Interest Rate Uncertainty?

A: Diversification and flexibility are key. First, build a diversified investment portfolio across multiple asset classes (including equities, bonds, cash, and commodities) to reduce exposure to market volatility. Second, review and optimize your debt position by prioritizing the repayment of high-interest debt (such as credit card balances). Finally, maintain sufficient cash reserves to cover unexpected expenses while preserving the ability to invest when attractive opportunities arise.

Q: How Often Does the Reserve Bank of Australia (RBA) Change Interest Rates?

A: Under the RBA’s current framework, introduced in 2024, the Board holds eight monetary policy meetings each year, approximately every six weeks. At the conclusion of each meeting, it announces whether the Official Cash Rate will be adjusted. Investors should closely monitor the meeting schedule and post-meeting statements to stay informed about the latest policy direction.

Q: Why Does the Australian Dollar Sometimes Fall Even After the RBA Raises Interest Rates?

A: There are several possible reasons. First, the market may have already “priced in” the expected rate hike, prompting investors to take profits once the announcement is made. Second, the RBA’s post-meeting statement may strike a “dovish” tone, for example by suggesting that the latest increase could be the final rate hike, causing expectations for future interest rates to decline. Third, rising global risk aversion, such as during major geopolitical events, may drive investors toward traditional safe-haven currencies like the US dollar. In such cases, the Australian dollar may weaken despite higher domestic interest rates.