Figure Two: Key Factors Driving the Bank of Japan’s Policy Normalization

- Inflation Target Achieved: After decades of deflation, Japan’s core Consumer Price Index (CPI) has finally remained steadily above the 2% target. This has provided the BOJ with the basic conditions for policy normalization.

- Wage Growth: More importantly, the BOJ has observed that a virtuous “wage-price” cycle is taking shape. Companies are willing to raise wages for employees, while higher employee income is driving consumption, further supporting moderate inflation.

- Shunto Results: The annual spring labor-management wage negotiations are a key indicator for observing wage growth momentum. The Shunto results in both 2025 and 2026 recorded the largest wage increases in decades, giving the BOJ sufficient confidence to confirm that wage growth is sustainable enough to support stable inflation.

Future Outlook: The BOJ’s Possible Rate Hike Path and Bond Purchase Reduction (QT) Plan

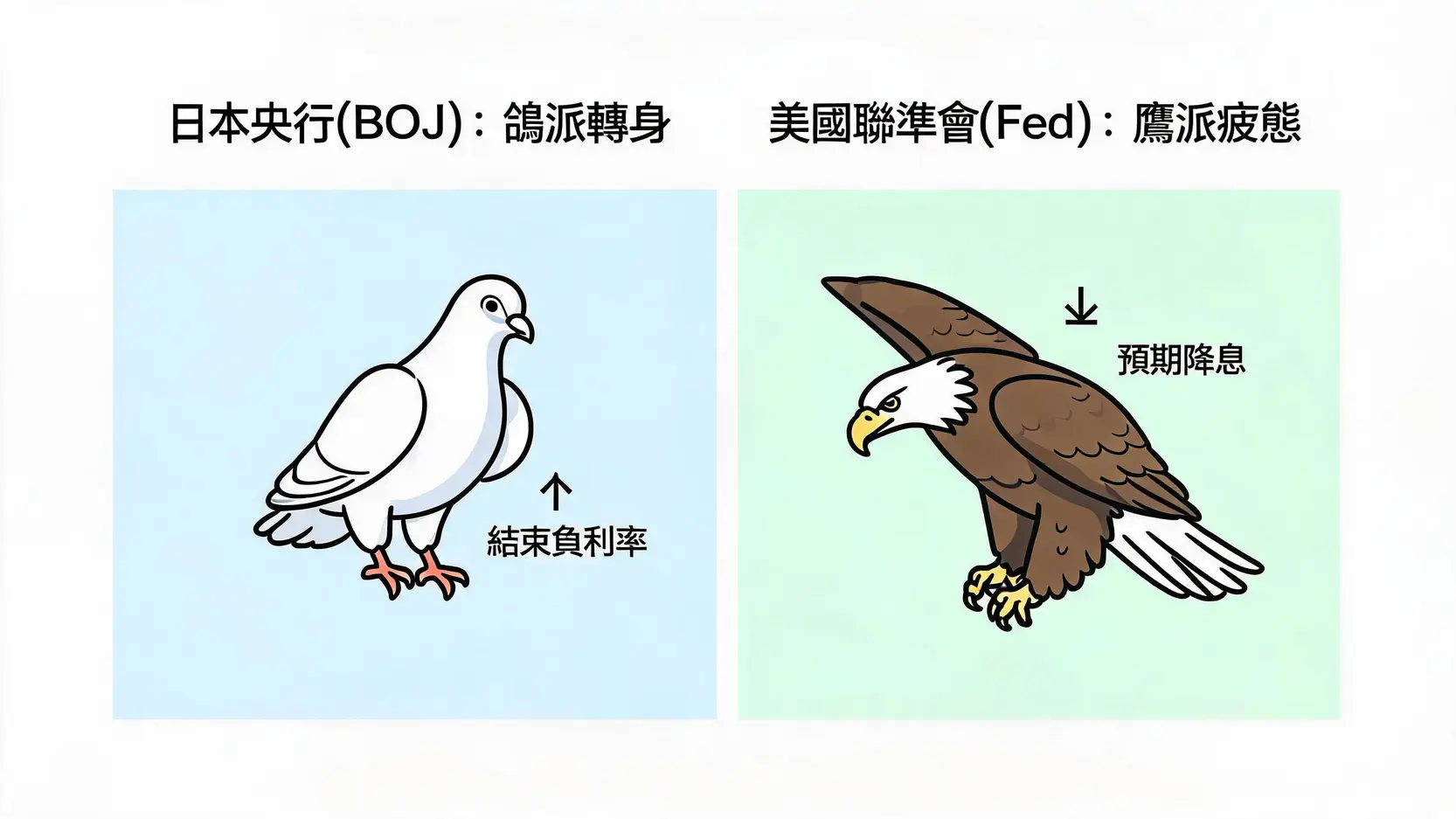

Ending negative interest rates and YCC is only the first step. The market’s current focus has shifted to the BOJ’s next move:

- Rate Hike Path: The market generally expects BOJ rate hikes to be slow and gradual. Governor Kazuo Ueda has repeatedly emphasized that the BOJ will carefully assess economic data to avoid tightening policy too quickly and hurting the fragile economic recovery. The pace of rate hikes will be far slower than that of major central banks in Europe and the US.

- Bond Purchase Reduction (QT): Although YCC has ended, the BOJ is still purchasing large amounts of government bonds in the market. The next step will be to gradually reduce the size of monthly bond purchases and eventually move toward “quantitative tightening” (QT), meaning a reduction in the central bank’s balance sheet. The impact of this step may be greater than interest rate adjustments, as it is directly related to market liquidity. For the latest developments from the Bank of Japan, you can follow its official website.

Further Reading (Highly Recommended)

Central Bank Balance Sheet Reduction Cheat Sheet: Understanding the Meaning and Process of Quantitative Tightening (QT), and Its Five Major Effects on the Stock Market

Is the US-Japan Interest Rate Differential Out of Control? Uncovering the Root Causes of Yen Depreciation and the Bank of Japan’s Policy Dilemma

Hawkish Fatigue: Observing the End of the US Federal Reserve’s (Fed) Rate Hike Cycle

In sharp contrast to the BOJ, the US Federal Reserve, which has played the role of “hawkish” leader over the past two-plus years, appears to be nearing the end of its powerful rate hike cycle. The market’s focus has shifted from “how high rates will rise” to “when rates will be cut”.

Historical Review: Rapid Rate Hikes and Quantitative Tightening (QT) in Response to Inflation

In the face of runaway inflation since 2022, the Fed adopted its most aggressive tightening policy in forty years:

- Rapid Rate Hikes: It raised the federal funds rate from near zero to above 5% within a short period, forcefully suppressing economic demand.

- Quantitative Tightening (QT): It also launched quantitative tightening (QT), reducing its balance sheet by tens of billions of dollars each month and withdrawing a large amount of liquidity released into the market during the pandemic.

This series of “hawkish” measures successfully brought inflation down from its peak, but also came at the cost of slower economic growth.

Judging the End of the Cycle: The Possibility of Rate Cuts Through CPI, PCE, and Nonfarm Payroll Data

The market’s judgment that the Fed’s rate hike cycle has ended is mainly based on changes in the following core data:

- Inflation Data (CPI & PCE): The Consumer Price Index (CPI) and Personal Consumption Expenditures Price Index (PCE), especially the core PCE favored by the Fed, have seen their annual growth rates fall significantly and continue to move toward the 2% target.

- Employment Data (Nonfarm Payrolls): Previously strong nonfarm payroll additions have begun to slow, while the unemployment rate has also edged up slightly from historical lows. This shows that the overheated labor market is cooling, reducing pressure from wage growth and helping to suppress inflation.

Once the trends of “cooling inflation” and “slowing employment” are established, the Fed will have the conditions to shift from a “restrictive” rate level toward a “neutral” or even “easing” stance, meaning the start of a rate-cutting cycle.

Future Outlook: Market Forecasts and Divisions Over the Timing of the Fed’s First Rate Cut

Although the direction is clear, there is major disagreement in the market over the “timing” of the Fed’s first rate cut. This mainly depends on how the data evolves:

- Dovish View: This view believes that signs of economic slowdown are becoming increasingly clear. To avoid a hard landing, the Fed should cut rates as early as possible, potentially starting in the third quarter of 2026.

- Hawkish View: This view believes that the “last mile” of inflation decline is the most difficult, and the labor market remains solid. Cutting rates too early could cause inflation to reignite. Therefore, the Fed will keep high rates in place for longer (Higher for Longer), and may not cut rates until the end of 2026 or even early 2027.

Fed Chair Powell’s stance is “data-dependent”, which also makes every inflation and employment report a key event that affects global market sentiment.

Differentiated Highlight: Comparing the Communication Art of BOJ and Fed “Forward Guidance”

Central bank decisions are certainly important, but how they “communicate” with the market is also an art. The BOJ and the Fed show completely different styles in this regard.

The BOJ’s Art of “Ambiguity”: Kazuo Ueda’s Communication Style and Market Interpretation

Bank of Japan Governor Kazuo Ueda, as an academic-style official, is known for a communication style marked by “caution” and “ambiguity”. He rarely gives a clear policy timetable, instead repeatedly emphasizing that the BOJ “needs to see more data” and will “continue patiently implementing easing”. The advantage of this style is that it preserves significant policy flexibility, but the disadvantage is that the market must spend considerable effort “interpreting” its subtext, increasing market volatility.

The Fed’s “Transparent” Strategy: How Powell’s Press Conferences and Dot Plot Guide Expectations

By contrast, the Fed’s communication strategy is much more “transparent”. Chair Powell holds a press conference after every rate decision, explaining the logic behind the decision in detail and answering questions from reporters. In addition, the Fed’s quarterly “Dot Plot” is a powerful tool for guiding market expectations. It shows each official’s forecast for future interest rate levels, allowing the market to clearly see the Fed’s internal policy leanings and possible path.

Why Understanding a Central Bank Governor’s “Subtext” Is Crucial for Trading

For forex traders, understanding the subtle differences in central bank communication is crucial. A change in wording or a shift in tone may foreshadow a major future policy change. For example, when Powell shifts from saying “continued rate hikes are appropriate” to saying “the policy rate has reached a restrictive level”, it means the rate hike cycle is ending. Similarly, when Kazuo Ueda begins mentioning the “virtuous wage-price cycle” more often, the market knows that the conditions for a policy shift are maturing. Learning to understand this “subtext” is essential for capturing trends and avoiding risks.

Conclusion

The policy divergence between the Bank of Japan and the US Federal Reserve is currently the most important trading theme in the forex market. Understanding the BOJ’s cautious pace as it shifts away from extreme easing, as well as the Fed’s data-dependent approach in seeking the right timing for rate cuts after completing its rate hike cycle, is key to forecasting the direction of the USD/JPY interest rate differential and grasping the yen’s medium- to long-term trend. Going forward, investors need to closely monitor inflation and employment data in both countries, as they are not only thermometers of the economy, but also the most important wind vanes for the central banks’ next policy decisions.

Frequently Asked Questions (FAQ) About Central Bank Policy Shifts

Q: What does the Bank of Japan ending YCC mean for the yen?

A: In the short term, ending YCC (Yield Curve Control) is usually seen as a signal of monetary tightening. In theory, this would push up the yield on Japan’s 10-year government bonds, narrow the interest rate differential with the US, and provide support for the yen (appreciation). However, the long-term impact is more complex and depends on the BOJ’s subsequent pace of rate hikes and changes in the broader global economic environment. If the pace of rate hikes is slow, the yen may return to depreciation pressure after the market’s positive expectations are priced in.

Q: What happens to the yen if the US Federal Reserve cuts rates later than expected?

A: If the Fed delays rate cuts due to stubborn inflation, it means the US dollar will maintain high interest rates for a longer period. This would cause the US-Japan interest rate differential to continue widening or remain at a high level, putting strong pressure on the yen and potentially pushing the USD/JPY exchange rate higher (meaning yen depreciation).

Q: Besides the BOJ and the Fed, does European Central Bank (ECB) policy affect the yen?

A: Absolutely. The global foreign exchange market is interconnected. If the ECB adopts a more hawkish policy than the Fed (such as cutting rates later), it would push up the euro. In carry trades, the yen is a major funding currency. A stronger euro may attract capital to shift from “long USD/JPY” to “long EUR/JPY”, thereby affecting the yen’s cross rates and indirectly influencing USD/JPY.

Q: What is “Shunto”, and why is it so important to the Bank of Japan’s decision-making?

A: “Shunto” refers to Japan’s nationwide labor-management wage negotiations held every spring. It is important because the negotiation results are the most critical leading indicator for measuring wage growth momentum in Japan. The Bank of Japan believes that to achieve a sustainable 2% inflation target, it must see continued wage growth supporting consumption. Therefore, strong “Shunto” results are the core basis for the central bank to judge whether a “virtuous wage-price cycle” has formed, and also the confidence behind its decision to exit negative interest rates and YCC policy.