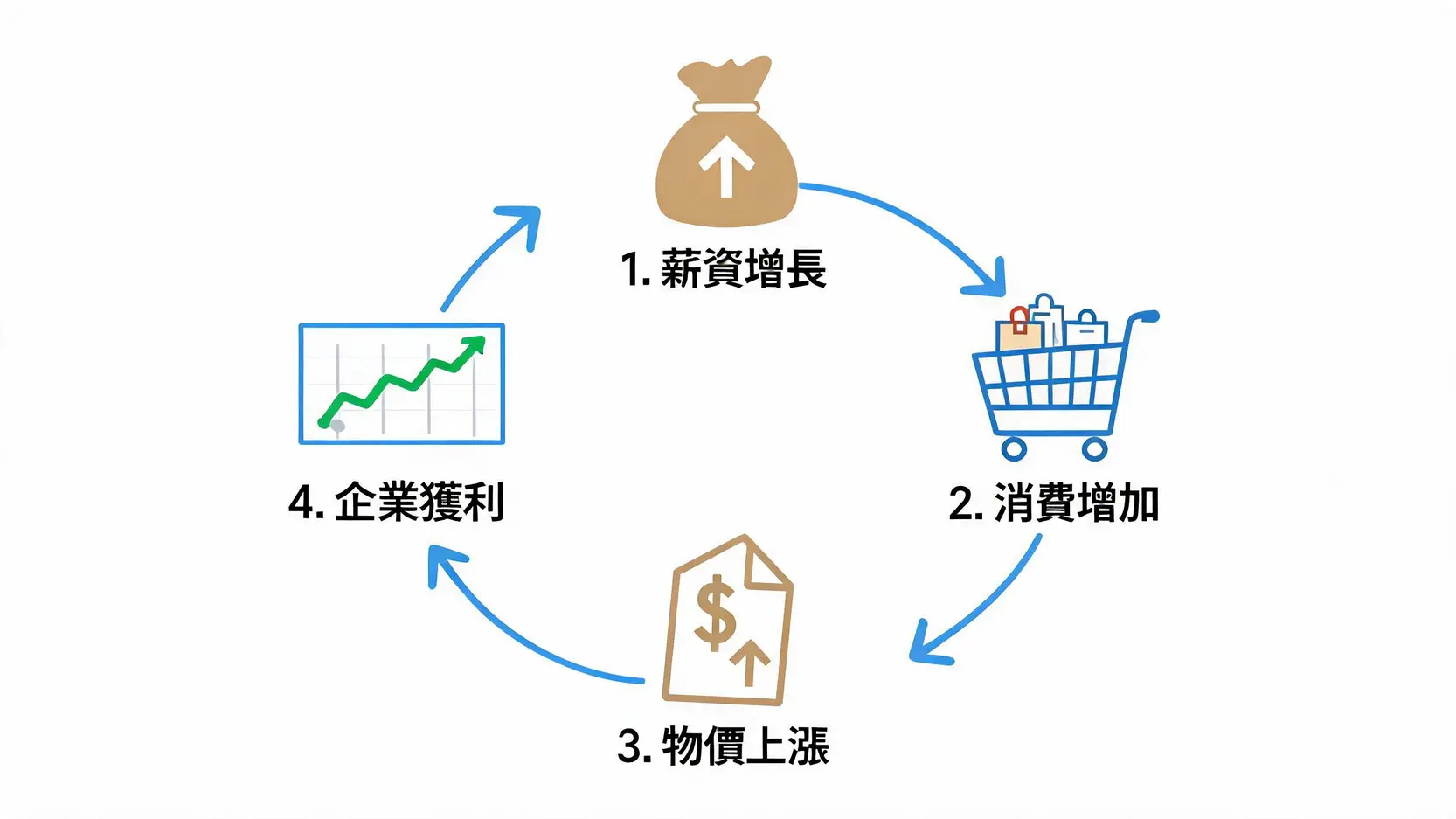

Figure One: A Virtuous Cycle Between Wages and Prices Is the Foundation for Bank of Japan Rate Hikes

Global Economic Conditions and Geopolitical Risks

As an open economy, Japan’s monetary policy cannot be completely independent of the rest of the world. The interest rate decisions of the US Federal Reserve (Fed), the economic performance of the eurozone, and any developments in global geopolitics will all affect the yen exchange rate and Japan’s economy. For example, if major overseas economies turn toward rate cuts, the interest rate gap with Japan will narrow, which may ease depreciation pressure on the yen and give the BOJ more policy room. Conversely, if global risk aversion rises, the yen may passively appreciate as a traditional safe-haven currency, which would then affect Japan’s exports and disrupt the central bank’s rate hike pace.

Potential Adjustments to Yield Curve Control (YCC) Policy

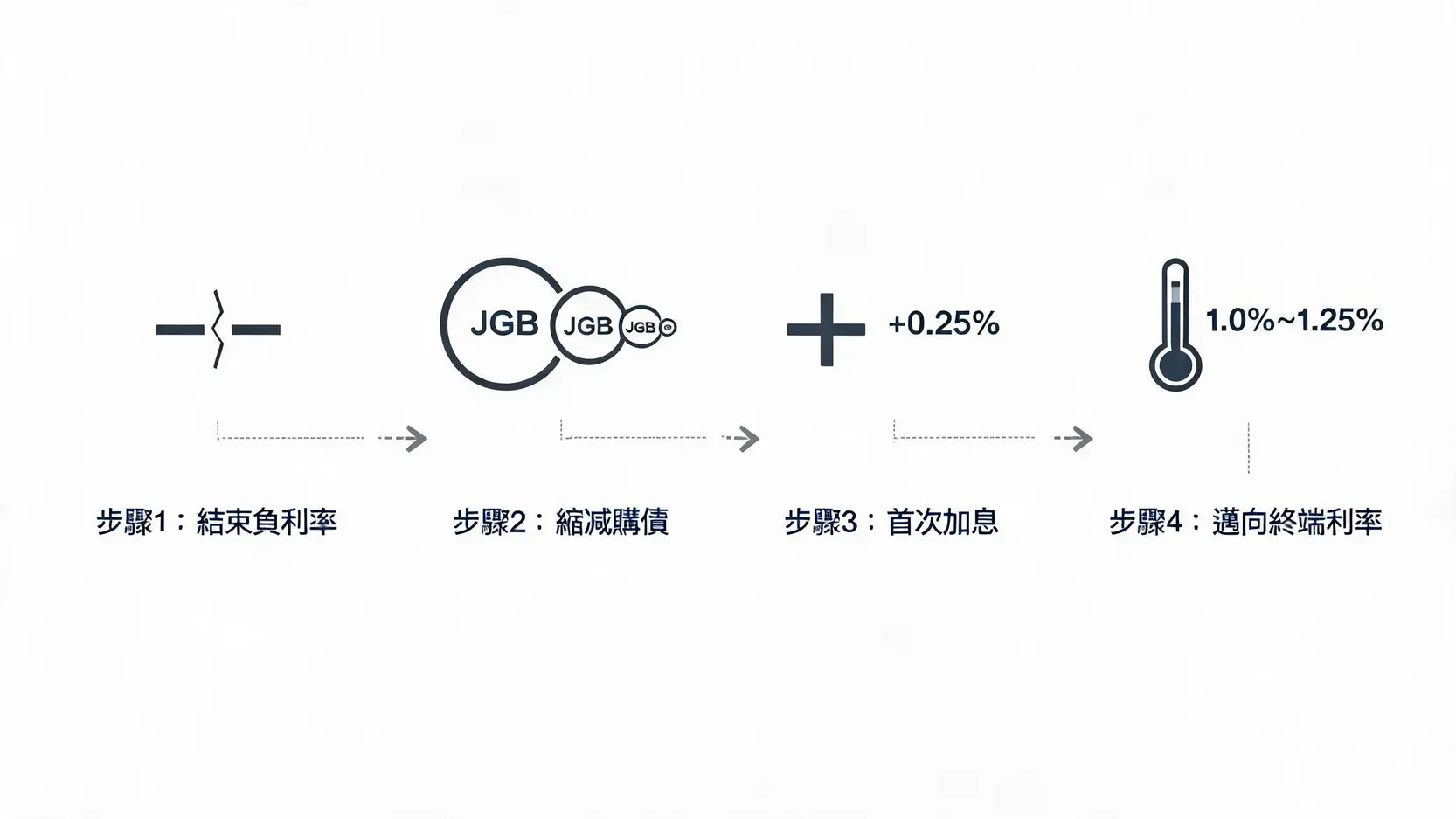

Although the Bank of Japan has officially abandoned the YCC policy, it has not completely stopped purchasing Japanese government bonds (JGBs). The central bank is currently still carrying out a bond purchase plan of about 6 trillion yen per month to maintain market stability. The market generally believes that before or alongside the next rate hike, the BOJ may gradually reduce the scale of bond purchases, that is, so-called “bond purchase tapering” (Tapering). Bond purchase tapering itself is a signal of monetary tightening, and its scale and pace will directly affect the direction of long-term interest rates. It is another important window for observing the central bank’s policy stance.

Market Expectations for the Bank of Japan’s Rate Hike Path

Based on the current views of major investment banks and economists, the market has formed an initial consensus on the BOJ’s rate hike path, but there are still differences over the specific timing.

Forecast for the Timing and Magnitude of Rate Hikes in 2026

The current mainstream market view is that the next rate hike is most likely to occur in Q3 or Q4 2026. The main reason is that the central bank needs more time to confirm the sustainability of wage growth and whether inflation can remain stable above the 2% target. As for the rate hike magnitude, it is expected to maintain a “gradual” pace, with a single rate hike potentially at 0.25 percentage points, raising the policy rate from the current 0%-0.1% range to around 0.25%.

Possible Range of the Terminal Rate

The “terminal rate” refers to the peak interest rate in the current rate hike cycle. Considering Japan’s structural economic issues (such as an aging population and high government debt), the market generally does not believe that the Bank of Japan will raise rates aggressively like the US Federal Reserve. Most forecasts suggest that the terminal rate in this rate hike cycle may fall within the range of 1.0% to 1.25%. This is a relatively neutral level that can curb overheated inflation without stifling economic growth.

The “Gradual” Nature of Monetary Policy Normalization

Kazuo Ueda is known for his cautious approach and emphasis on communication. He is well aware that after ending decades of ultra-loose policy, any overly aggressive move could cause a major shock to the economy and financial markets. Therefore, a “gradual” normalization path is an inevitable choice. Before each decision, the central bank will release signals to the market through official remarks, meeting minutes, and other channels to guide expectations and avoid “policy surprises”. To understand the meaning of policy normalization in greater depth, please refer to the Complete Analysis of the Bank of Japan’s Rate Hike: Bidding Farewell to the Negative Interest Rate Era, Full Forecast for the Yen and Japanese Stocks