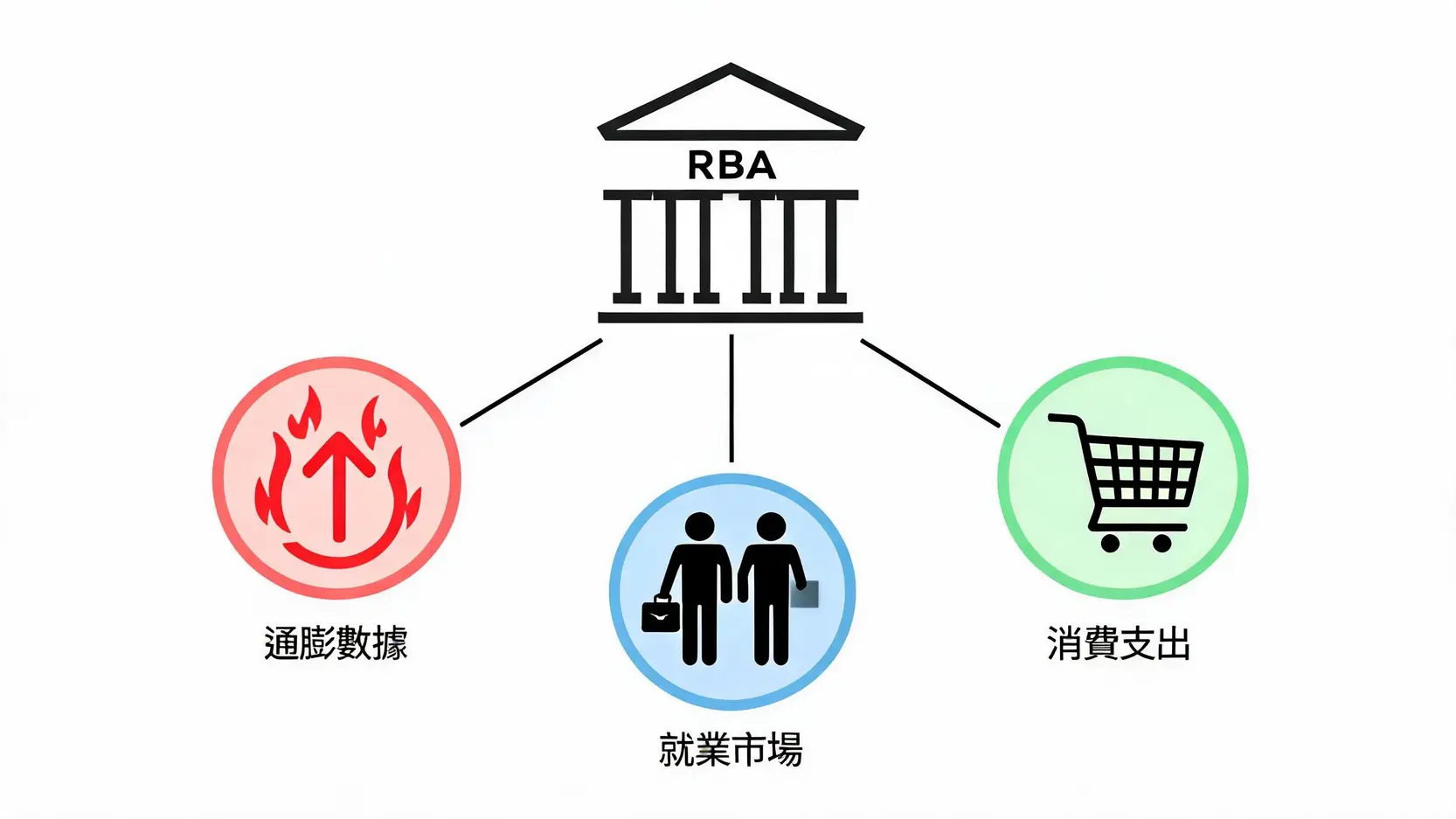

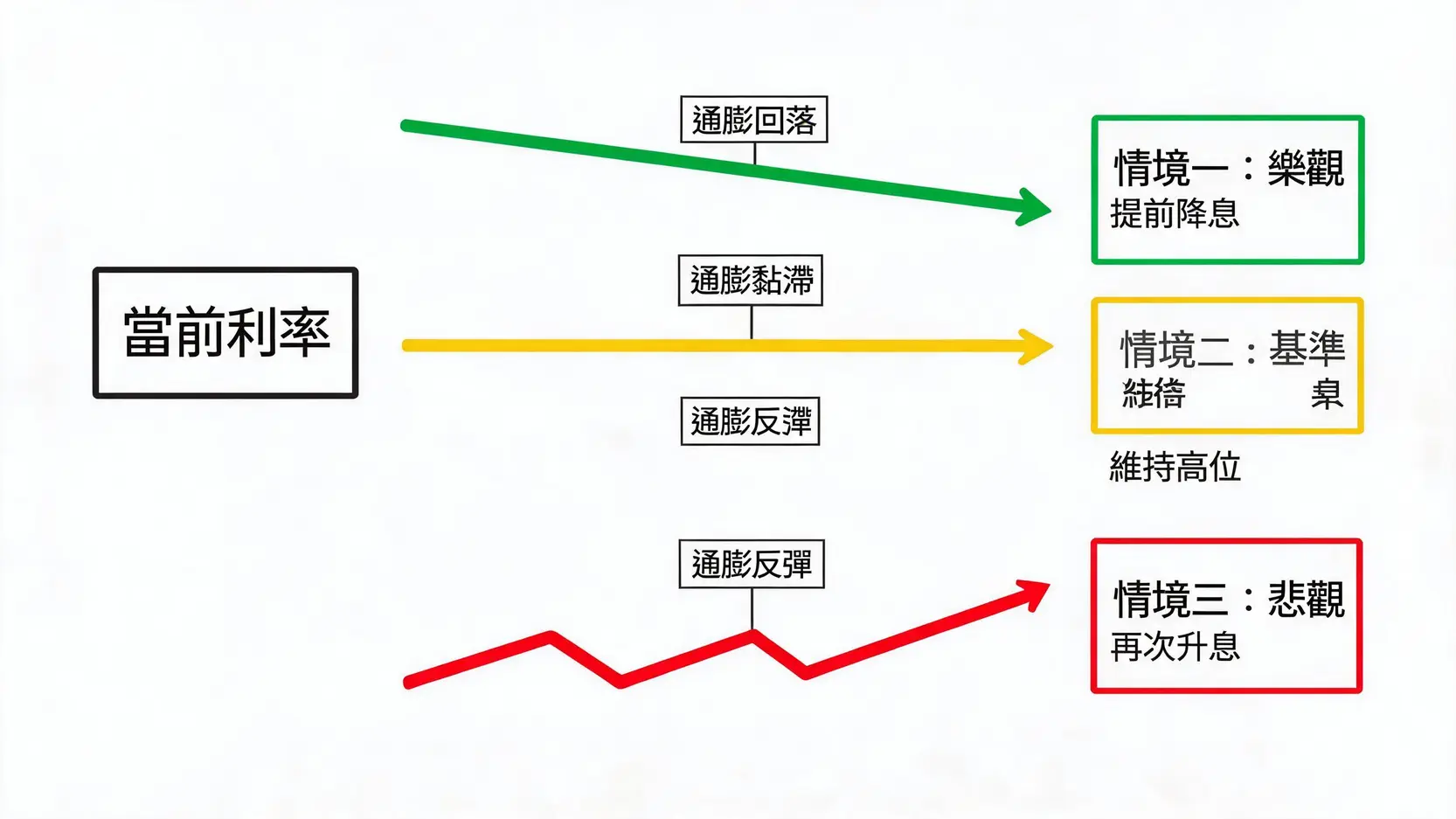

Three Possible Scenarios for the Future Interest Rate Path

Scenario One (Optimistic): Inflation Falls Rapidly and Rate Cuts Are Brought Forward

Trigger conditions:

- Global supply chain issues ease and import prices fall.

- Australian domestic consumer spending slows significantly and the labor market cools.

- CPI data comes in below expectations for several consecutive quarters.

Interest rate path: Under this scenario, the RBA could begin its first rate cut as early as the fourth quarter of 2026, similar to CBA’s forecast.

Scenario Two (Base Case): Inflation Declines Slowly and Interest Rates Stay Higher for Longer

Trigger conditions:

- Inflation remains sticky, especially in the services sector.

- The labor market remains resilient, with wage growth slowing gradually.

- The global economic outlook remains uncertain, prompting the RBA to take a cautious wait-and-see approach.

Interest rate path: This is currently the mainstream view among the market and many experts (such as ANZ and NAB). Interest rates are expected to remain at 4.35% or slightly higher until the end of 2026, with room for rate cuts only emerging in the first half of 2027.

Scenario Three (Pessimistic): Inflation Remains Stubborn and the RBA Is Forced to Raise Rates Again

Trigger conditions:

- Global geopolitical risks escalate, triggering a new shock to energy or food prices.

- Australian domestic fiscal stimulus policies, such as tax cuts, unexpectedly boost consumer demand.

- CPI data unexpectedly rebounds, breaking the downward trend.

Interest rate path: Under this least favorable scenario, the RBA would have no choice but to restart rate hikes, with the cash rate potentially reaching Westpac’s forecast of 4.85% or even higher. This would create significant pressure on mortgage holders and the broader economy.

Frequently Asked Questions (FAQ) About Australian Interest Rate Forecasts

Q: If the RBA Raises Rates Again, How High Could the Cash Rate Go?

A: Based on the most hawkish current forecasts (such as Westpac’s), if inflationary pressure remains persistent, the RBA may need to raise the cash rate to 4.85%. In a more extreme scenario, a move to 5.0% cannot be ruled out, but this would have a severe tightening effect on the economy, so the probability is relatively low.

Q: When Does the Market Expect the First Rate Cut?

A: Market expectations remain divided. Pricing in the interest rate futures market suggests that traders see a low probability of a rate cut before the end of 2026, with expectations generally pointing to the second quarter of 2027 or later. However, some economists (such as those at CBA), believe that if economic data aligns, the first rate cut could come as early as the fourth quarter of 2026.

Q: How Will Changes in Australian Interest Rates Affect the Australian Dollar?

A: Generally speaking, higher interest rates attract international capital seeking higher returns, supporting the Australian dollar. Therefore, if the RBA raises rates or keeps interest rates higher for longer than other countries (especially the US), it would support the Australian dollar. Conversely, if the RBA cuts rates first, the Australian dollar may weaken. For more analysis on the Australian dollar outlook, please refer to our in-depth article.

Q: As an Ordinary Investor, How Can I Use These Forecasts to Adjust My Strategy?

A: First, mortgage holders should assess their repayment capacity under a high interest rate environment and consider whether to lock in a fixed rate. For investors, a rate hike environment is generally favorable for financial stocks such as banks, but unfavorable for interest rate-sensitive sectors such as technology and real estate. When rate cuts are expected, bond prices typically rise, making them a potentially attractive allocation option. The key is to keep your portfolio diversified and adjust flexibly based on the latest economic data and market expectations.

Conclusion

Overall, there is no clear consensus among markets and experts regarding the Australian interest rate outlook for the second half of 2026 and beyond. Forecasts range from “rate cuts before the end of the year” to “further rate hikes”, highlighting the high level of uncertainty surrounding the outlook. However, investors need not feel overwhelmed. By closely monitoring the three key indicators of inflation (CPI), employment, and consumer spending, while also considering analyses from professional institutions such as Australia’s Big Four banks, it is possible to make more informed judgments about the RBA’s likely policy direction. The central question remains whether inflation can return to target before high interest rates begin to weigh too heavily on economic growth. Until that answer becomes clear, maintaining a flexible investment portfolio and a strong awareness of risk will remain the most effective approach to navigating future market developments.