Macroeconomic Transmission Chain: From the Nonfarm Payrolls Report to Stock Market Volatility

The Starting Point: A “Too Strong” Nonfarm Payrolls Report

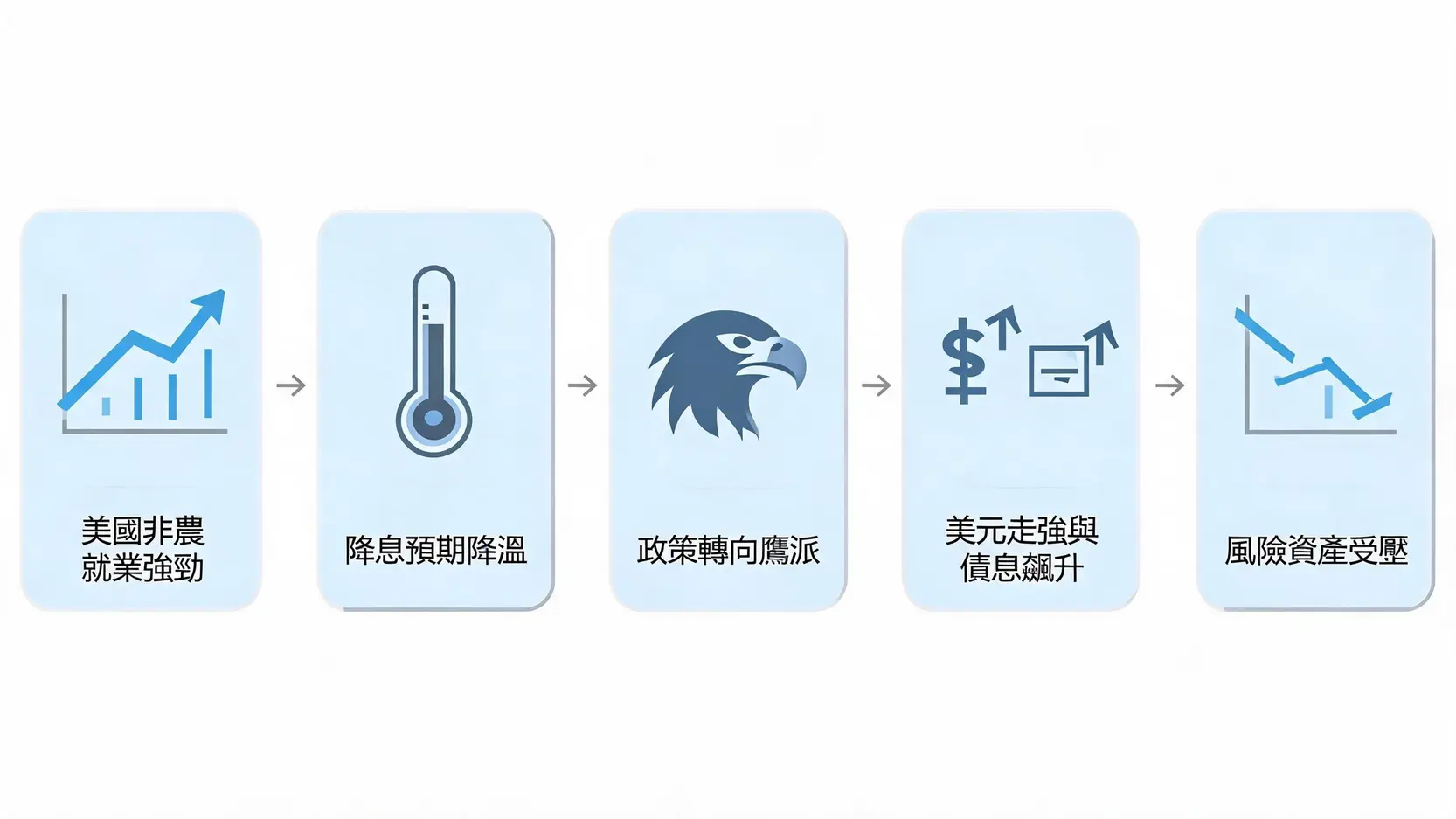

Major market moves often begin with economic data that significantly exceeds expectations. This time, the catalyst came from the latest nonfarm payrolls report released by the US Bureau of Labor Statistics.

Data Review: Employment Growth and Wage Growth Both Exceeded Expectations

According to the official data released by the US Bureau of Labor Statistics, the latest nonfarm payrolls report showed job creation well above market expectations, while annual average hourly earnings growth also remained at a relatively elevated level. Specifically:

- Job Growth: Employment increased by significantly more than forecast, indicating that labor demand remains exceptionally strong.

- Unemployment Rate: The unemployment rate remained near historic lows and even declined further.

- Wage Growth: Both annual and monthly growth in average hourly earnings exceeded expectations, making wage growth an important leading indicator of inflationary pressure.

Taken together, these figures painted a picture of an “overheated” US economy, sharply contrasting with the market’s earlier expectation of a “gradual cooling”.

Market Interpretation: An Overheated Economy Means Inflation Remains Difficult to Control

For financial markets, the data itself is only part of the story. The real focus is how the data is “interpreted”. This “too strong” nonfarm payrolls report sent several key messages:

- Economic Resilience Exceeds Expectations: Strong employment supports consumer spending, reducing the risk of a near-term recession.

- Inflation May Be More Persistent: Rapid wage growth remains the primary driver of service-sector inflation. Continued strong wage gains suggest that the Federal Reserve’s “last mile” in fighting inflation will be especially challenging. Concerns about a potential wage-price spiral” have once again returned to the forefront.

- Limited Room for Federal Reserve Policy Easing: With inflationary pressure remaining elevated, the Federal Reserve’s ability to ease monetary policy (through rate cuts) has become significantly more constrained.

The First Link: A Dramatic Reversal in Federal Reserve Interest Rate Expectations

Following the release of the nonfarm payrolls report, the most immediate impact appeared in the interest rate futures market, where expectations for the Federal Reserve’s policy path shifted dramatically.

Rate Cut Expectations Collapse While Rate Hike Expectations Re-Emerge

Before the data release, markets generally expected the Federal Reserve to begin cutting interest rates during the year to prevent a hard economic landing. However, the strength of the data effectively eliminated the case for “preventive rate cuts”. Interest rate futures quickly repriced:

- Timing of the First Rate Cut: Expectations shifted substantially, from the second half of the year to the end of the year or even later.

- Total Rate Cuts Expected During the Year: Both the expected number and cumulative size of rate cuts were significantly reduced.

- Possibility of Another Rate Hike: Although still considered unlikely, markets even began assigning a small probability to “another interest rate” increase as a response to stubborn inflation.

Hawkish Comments From Federal Reserve Officials Reinforce Market Expectations

After the data release, several Federal Reserve officials also delivered “hawkish” remarks. They consistently emphasized “their commitment to fighting inflation”, “the need to see more evidence that inflation is moving sustainably lower”, and the fact that there is “no urgency to cut interest rates”. These comments reinforced the market’s changing expectations, further solidifying the consensus that interest rates will remain “Higher for Longer”.

Further Reading (Highly Recommended)

2026 US Rate Cut Guide: The Federal Reserve’s Rate Cut Timeline and the Three Key Conditions Explained

The Complete Guide to the Impact of US Interest Rate Hikes: Five Major Effects on Hong Kong’s Stock Market and Property Market, Plus Response Strategies

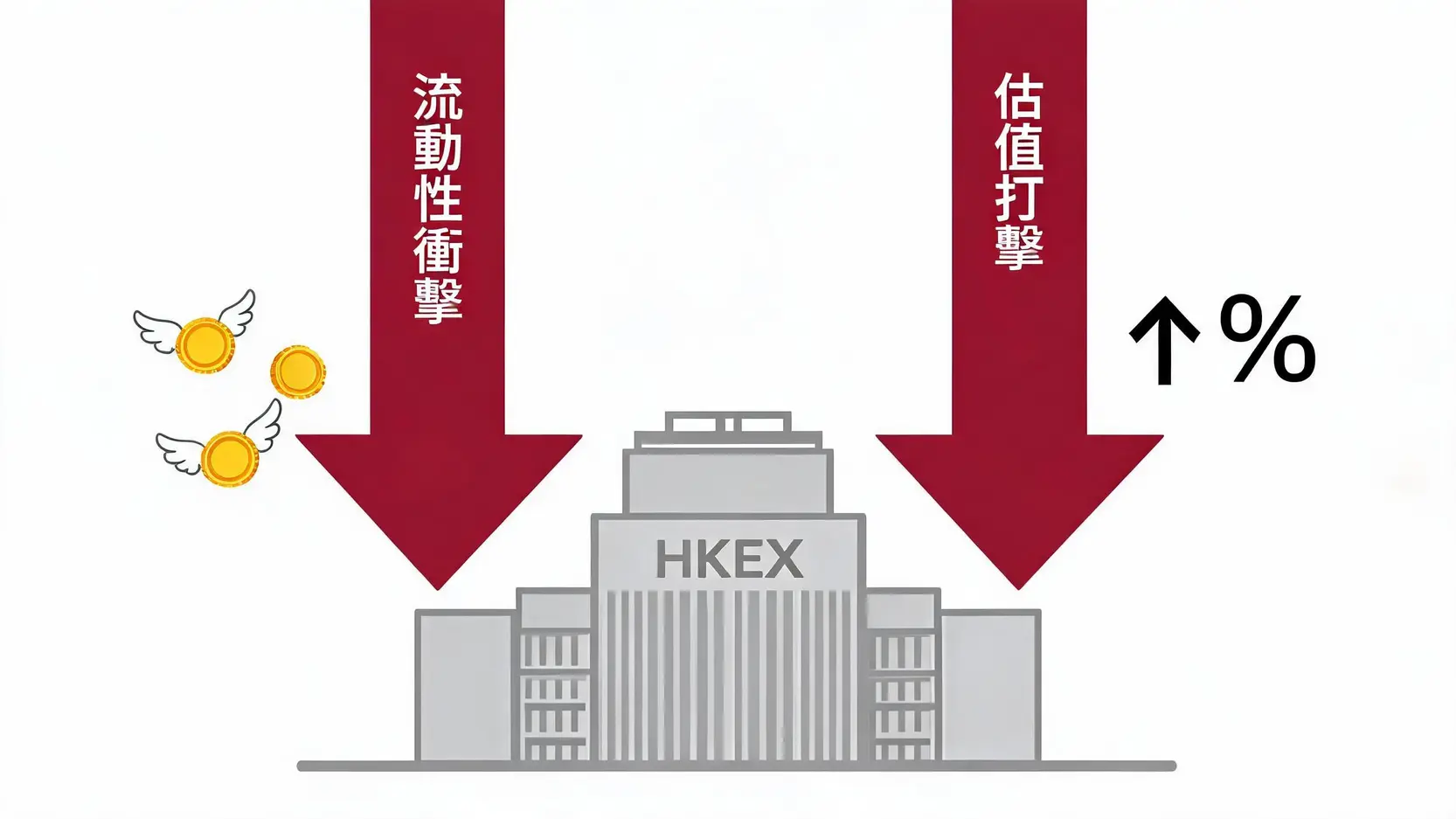

The Second Link: The Dual Reaction of the US Dollar and US Treasuries

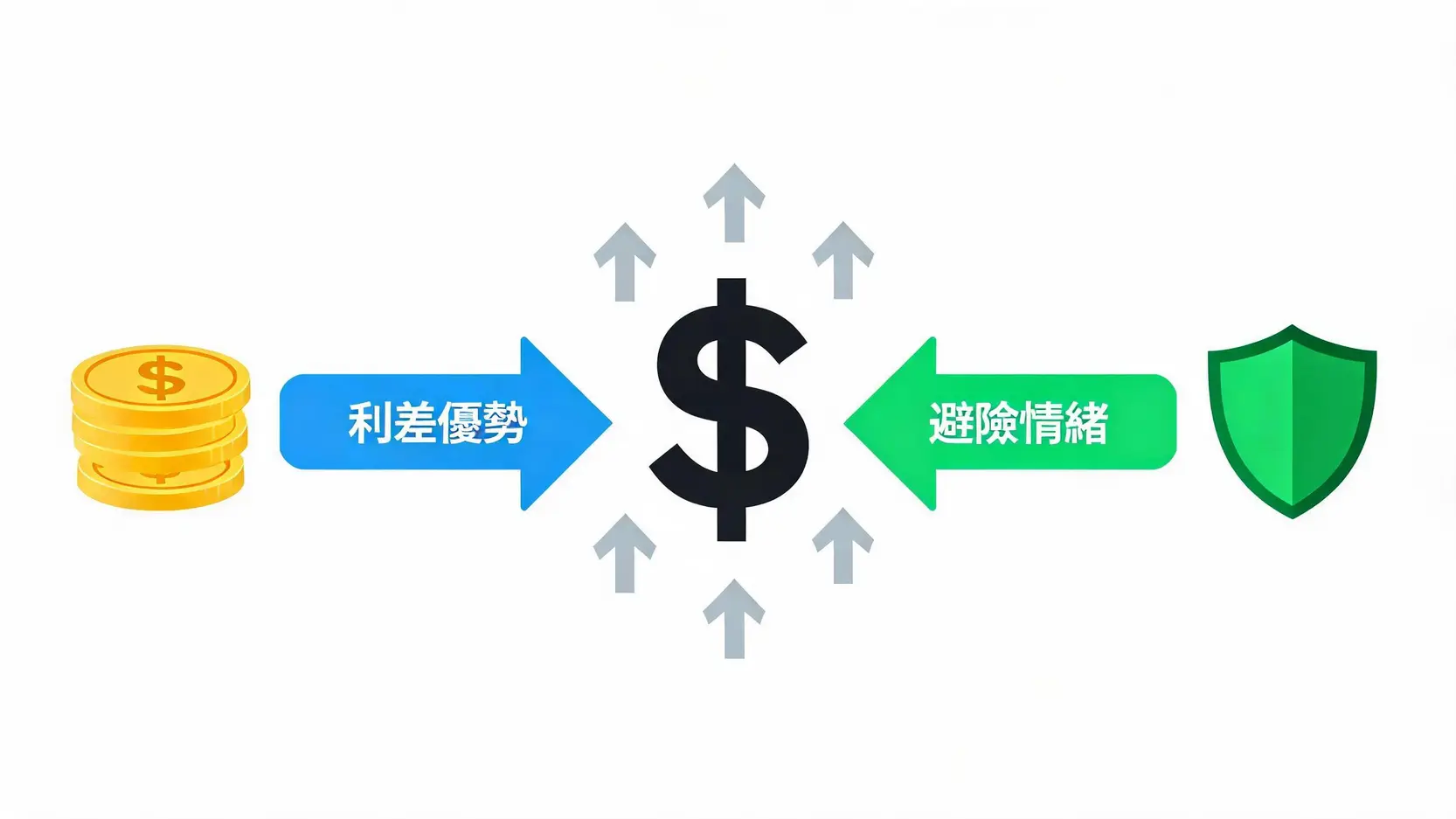

Federal Reserve policy expectations act as the “master valve” controlling global capital flows. As expectations turned more hawkish, both the US dollar and the US Treasury market reacted immediately, amplifying market volatility.

US Dollar Index Strengthens: Interest Rate Differentials Combined With Safe-Haven Demand

The strengthening of the US dollar became almost inevitable, driven by two major forces:

- Interest Rate Differentials: As expectations for US interest rates moved higher while other major economies (such as Europe and Japan) maintained unchanged or potentially lower interest rates, US dollar-denominated assets offered relatively more attractive returns. This attracted global capital into the US, driving the US dollar higher.

- Safe-Haven Demand: Market volatility triggered by economic data encourages investors to seek relatively safe assets. As the world’s leading reserve and safe-haven currency, the US dollar typically benefits whenever market uncertainty increases.