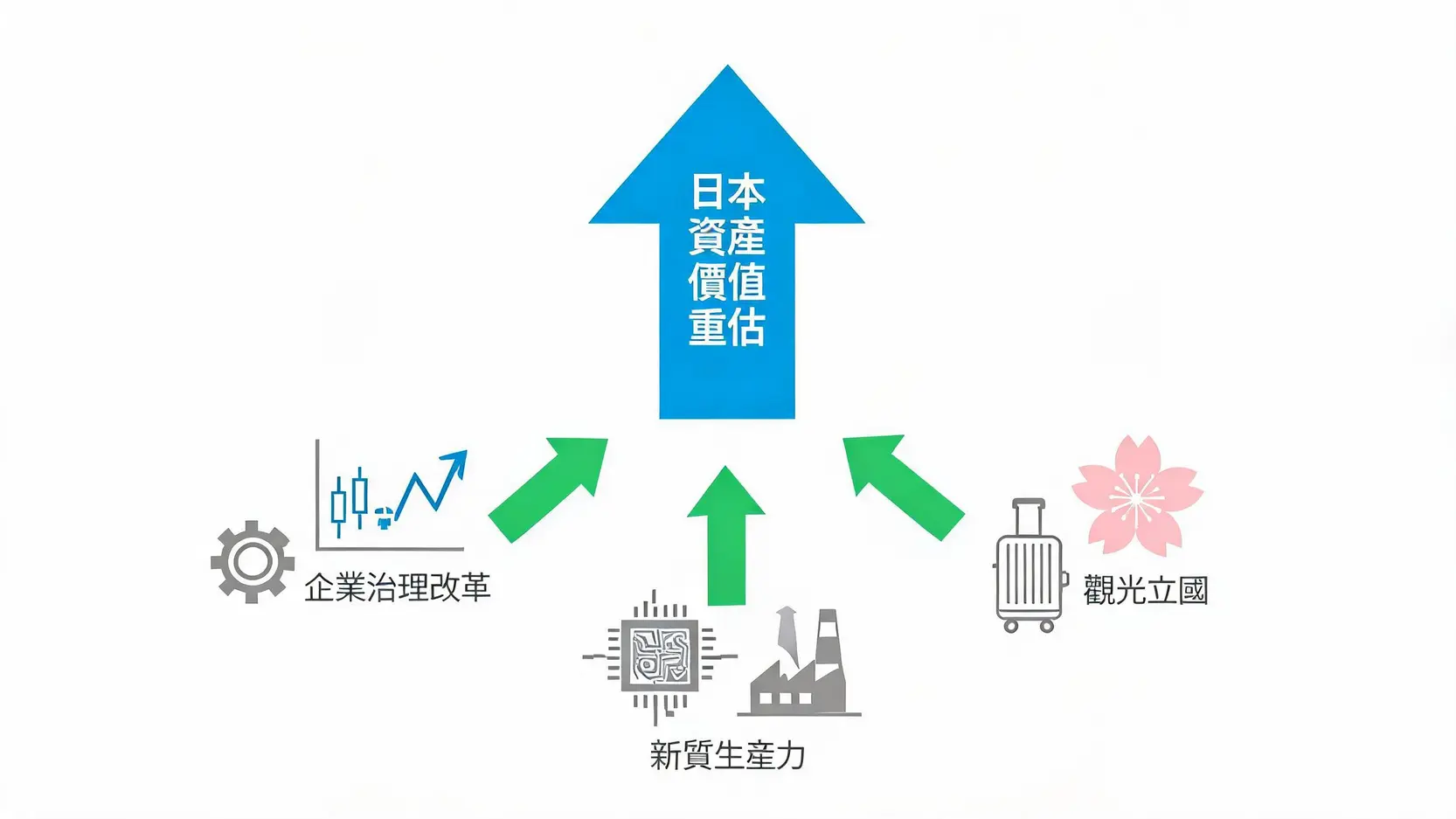

Three Core Engines Driving Japan’s Value Repricing

Corporate Governance Reform: What Warren Buffett Values Is Not Just Cheapness

Warren Buffett’s major investments in Japan’s five major trading houses in recent years have attracted global attention. What he values is far more than low stock prices. It is also the fundamental improvement in Japanese corporate governance. Under the requirements of the Tokyo Stock Exchange (TSE), many companies with low price-to-book ratios (P/B Ratio) have been urged to take measures to improve shareholder returns and corporate value. This reform is improving the profitability and investment appeal of Japanese companies from within, injecting new vitality into the overall economy.

The Rise of New Quality Productive Forces: The Revival of Semiconductors and High-End Manufacturing

Japan is regaining its key position in the global technology supply chain. With TSMC’s plant in Kumamoto as a landmark event, Japan’s semiconductor supply chain is rapidly reviving. This has not only driven the economy and real estate market in areas such as Kumamoto, but also symbolizes Japan’s full return in fields of “new quality productive forces”, such as high-end manufacturing and precision instruments. A strong real economy foundation is the stabilizing anchor that supports long-term asset value growth.

Tourism-Oriented Nation: How the Tourism Recovery Drives Commercial Real Estate Value

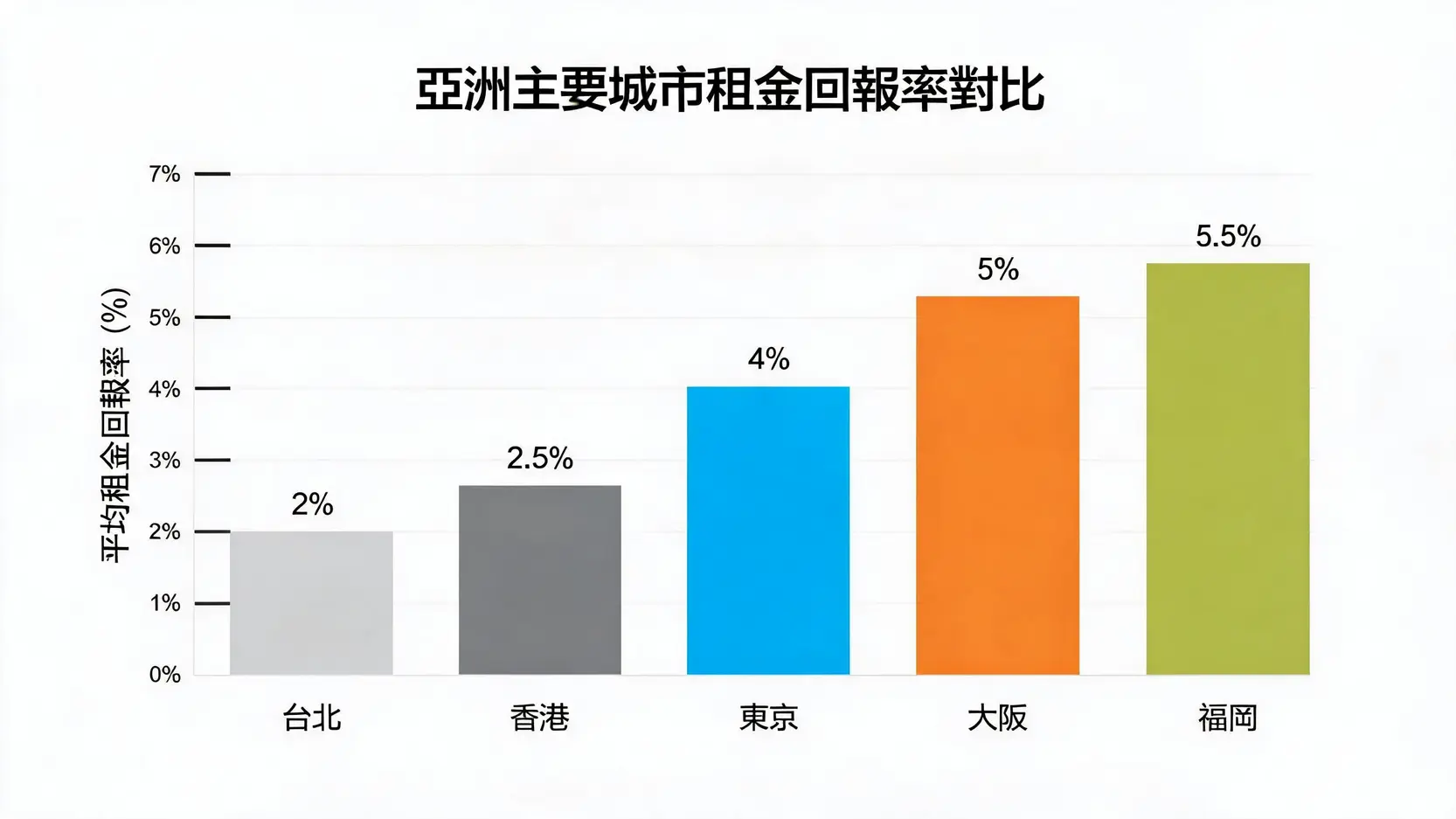

Yen depreciation has also greatly stimulated Japan’s tourism industry. Tourists from Taiwan, Malaysia, Europe, the US, and other places have poured in, not only bringing strong profits to the hotel industry, but also greatly boosting retail, dining, and other commercial activities. The strong recovery in tourism has directly driven the value of commercial real estate in tourist cities (such as Tokyo, Osaka, Kyoto, and Hokkaido), including hotels, shops, and guesthouses, making it one of the most explosive segments of Japan’s property market.

Frequently Asked Questions (FAQ)

Q: Is It Still Not Too Late to Invest in Japan’s Property Market Now?

A: It is definitely not too late. The current market rise is still more in the early stage driven by exchange rate advantages and value discovery. Japan’s structural economic shifts, such as corporate reform and the return of inflation, are long-term positive factors. Rather than chasing hotspots that have already risen sharply, investors should pay more attention to areas with solid fundamentals and strong rental demand, but where prices have not yet fully reflected their value, and carry out “value investing”.

Q: Besides Tokyo, Which Other Japanese Cities Are Worth Investing In?

A: Of course! Although Tokyo, as the capital region, has an irreplaceable position, other cities are also showing huge potential. For example, Osaka is viewed favorably for its infrastructure and development prospects due to the 2025 World Expo and the upcoming integrated resort (IR); Fukuoka, as the gateway to Kyushu, continues to see population growth and is Japan’s “startup capital”; while Sapporo in Hokkaido has also attracted significant attention thanks to its unique tourism resources and urban redevelopment plans.

Q: If the Yen Rebounds, Will My Overseas Assets Shrink?

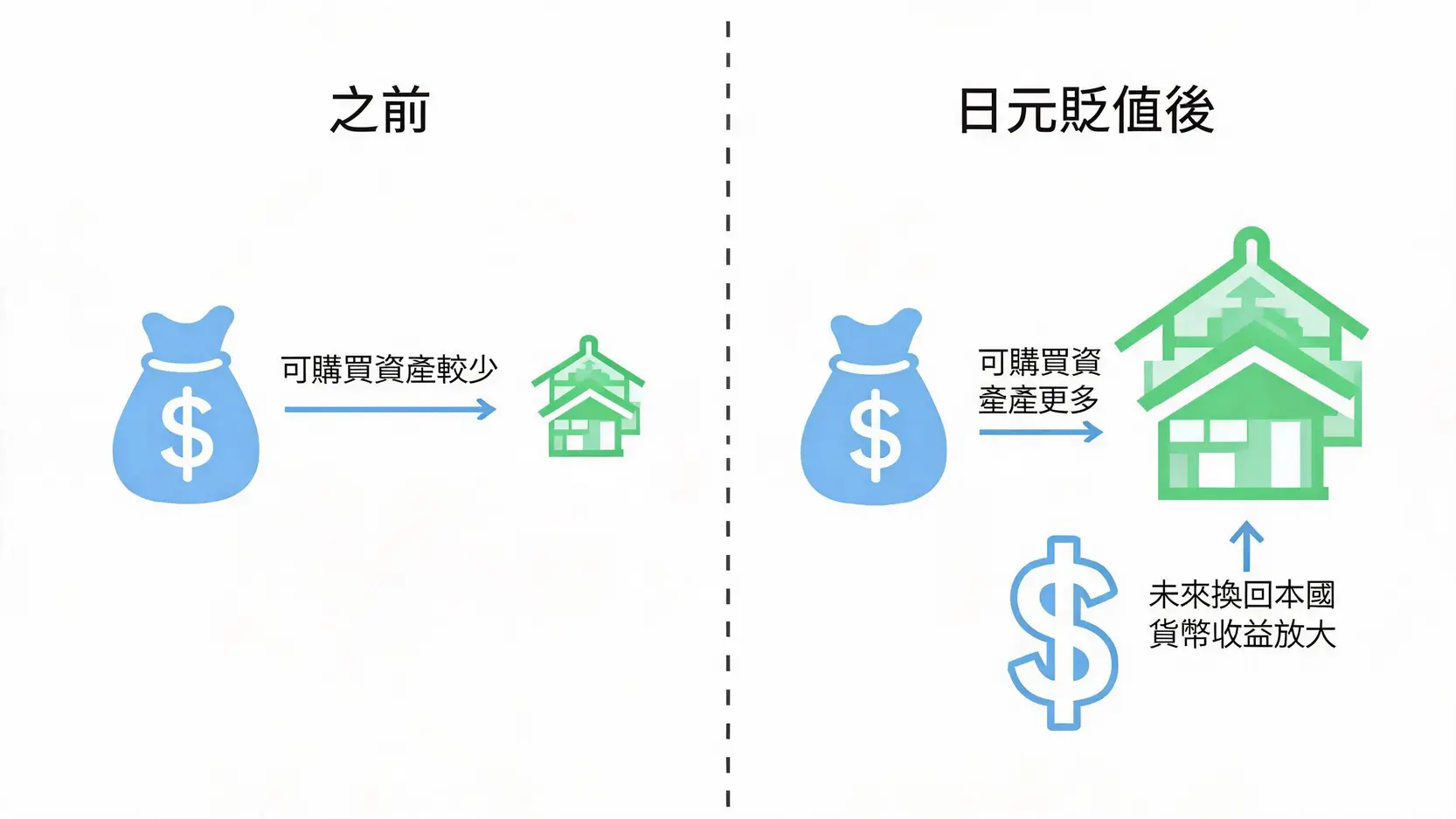

A: This is an exchange rate risk that all overseas investors will consider. Indeed, if the yen appreciates significantly, the asset value calculated in your home currency may decline. But this is a double-edged sword: a stronger yen usually also means Japan’s economic fundamentals are stronger, which may further push up the price of your real estate itself and form a hedge. For large-scale investments, you may consider using tools such as forward foreign exchange contracts to partially lock in exchange rates. But for most long-term investors, the core should be the appreciation potential of the asset itself, rather than excessive speculation on short-term exchange rate fluctuations.

Conclusion

In summary, yen depreciation pressure is not a crisis, but a catalyst that has opened the curtain on global asset repricing. In this wave, Japan’s property market has become an ideal “safe haven” and valuation depression for global capital, thanks to its superior rental yields, asset stability, and the long-term dividends of economic structural reforms. For investors seeking diversified asset allocation and protection against single-market risks, deeply understanding this value repricing, triggered by exchange rates and supported by fundamentals, is the key to seizing the golden opportunity in the Japanese market over the next decade.