Not the Same as Before: A Comparison of Japan’s Economic Fundamentals in the 1990s vs. Today

Balance Sheets: Companies and Banks Today Are Much Stronger Than Before

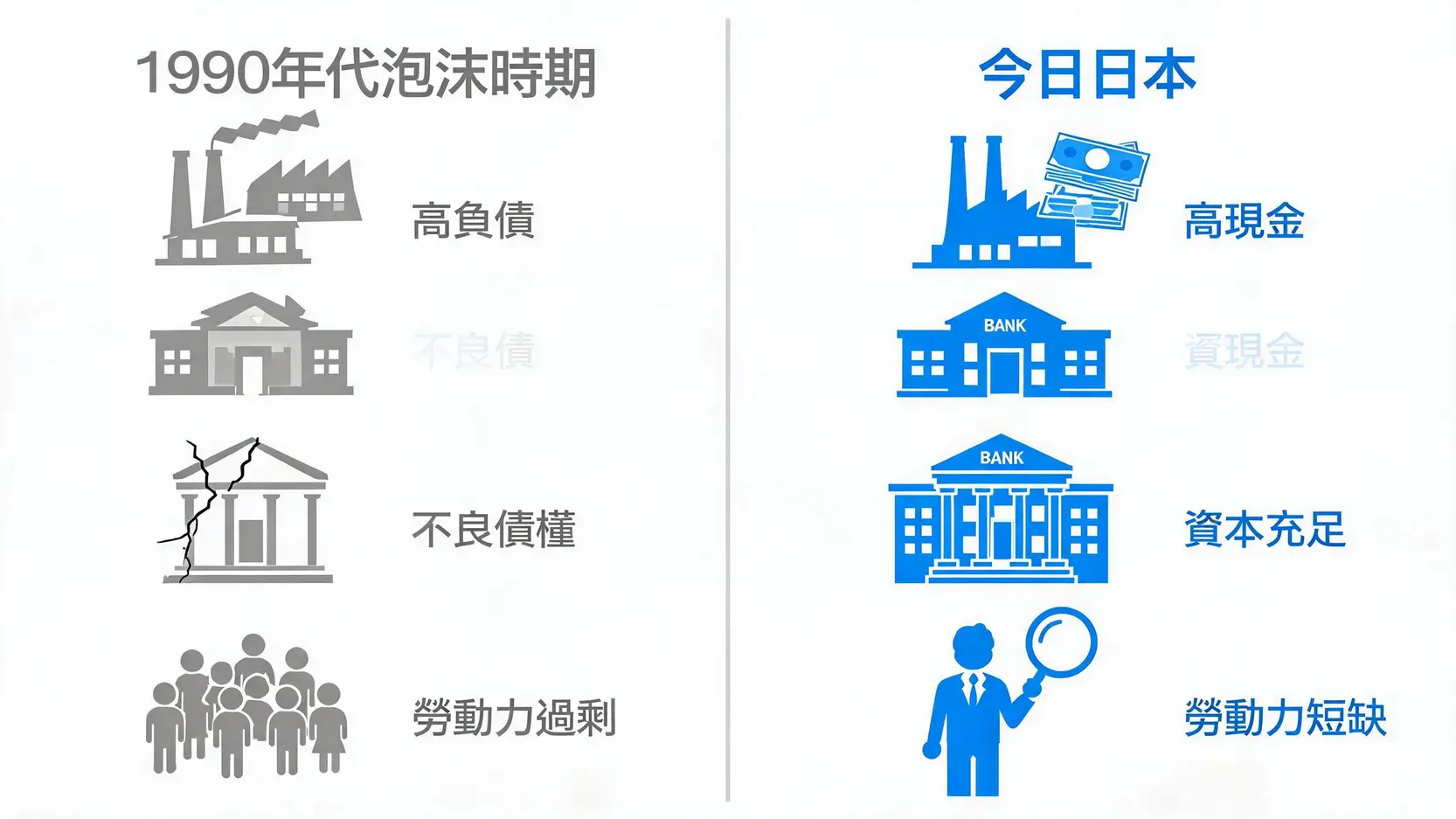

The core problem behind the bursting of the bubble in the 1990s was the extreme fragility of corporate and bank balance sheets. At the time, companies had borrowed excessively to invest in real estate and the stock market. Once asset prices plunged, they fell into massive losses and debt trouble. Banks were also on the brink of bankruptcy because they held large amounts of non-performing loans.

Today, after thirty years of “deleveraging”, Japanese companies generally hold large amounts of cash and are in extremely healthy financial condition. The banking system has also moved beyond the burden of non-performing loans, with capital adequacy ratios far above international standards. Healthy balance sheets mean Japan’s economy is better able to withstand external shocks, while also providing a solid foundation for companies to raise wages and invest.

Demographic Structure: How Labor Shortages Change Deflation Expectations

In the past, population aging was seen as a burden on Japan’s economy. In the current environment, however, it has unexpectedly become a catalyst for breaking the deflationary cycle. Severe labor shortages force companies to raise wages in order to recruit enough employees, fundamentally changing the decades-long situation of wage stagnation. A tight labor market has become an important structural factor driving service price increases and forming positive inflation expectations.

Global Environment: The Shift From Globalization to Regional Alliances

The 1990s were an era when globalization advanced rapidly, and companies could easily move production to low-cost countries. Today, however, the world is undergoing a shift from globalization to supply chain restructuring. Rising geopolitical risks have prompted companies to place greater emphasis on supply chain resilience and security. Many Japanese companies have begun moving production lines back home (reshoring), which not only increases domestic employment and investment, but also makes production costs harder to reduce, helping to support price levels.

Further Reading (Highly Recommended)

Beginner’s Guide to Hong Kong Stock Investment: Learn From Scratch How Stocks Make Money (With Popular Hong Kong Stock Accounts in 2026)

How to Buy Apple Stock? A Five-Step Beginner’s Guide: From Converting to US Dollars to Placing an AAPL Order

Conclusion

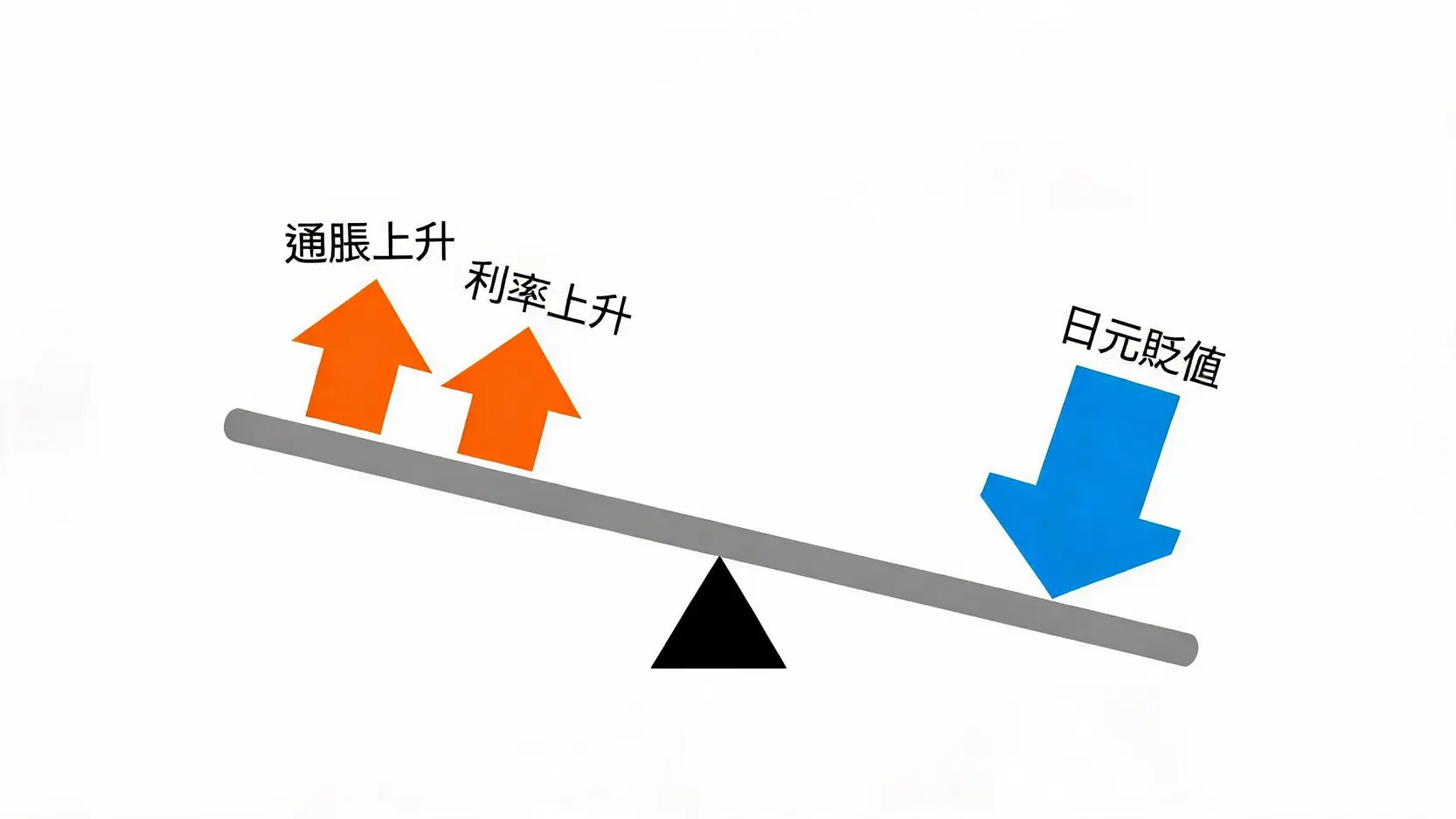

In summary, the current coexistence of Japan inflation and yen depreciation pressure is a complex phenomenon shaped by multiple intertwined factors. The spark of inflation was ignited by external imported pressures, but whether it can continue burning depends on structural shifts in wage growth and domestic demand recovery. Although the Bank of Japan has been raising rates slowly, with interest rates reaching their highest level since 1995, the huge interest rate differential with the US and the market’s dovish expectations have greatly weakened the policy effect, making it difficult to reverse the yen’s weakness in the short term.

However, compared with the bubble economy era, Japanese companies and banks today are in healthier condition, while structural changes in the labor market and the restructuring of global supply chains have provided favorable conditions for Japan’s long-term economic recovery. For investors, understanding this macro background is the first step to grasping future global asset repricing and Japan investment opportunities (such as the stock market and real estate). This global economic experiment has only just begun.

Frequently Asked Questions About Japan Inflation and Yen Depreciation

Q: How is this round of Japan inflation different from the past?

A: The biggest difference lies in structural factors. In the past few decades, brief periods of inflation were mostly triggered by a single factor, such as consumption tax hikes, and could not be sustained. This round of Japan inflation, however, is not only driven by global increases in energy and raw material prices, but more importantly, is accompanied by significant wage growth not seen in decades (as reflected in the “Shunto” results), as well as broad-based price increases in the service sector driven by labor shortages and demand recovery. This means the foundation of inflation is broader and more solid, and it is more likely to form a positive “price-wage” upward spiral rather than being short-lived.

Q: What direct impact does yen depreciation have on ordinary people?

A: The impact is two-sided. For people living in Japan, the most direct negative impact is that imported goods become more expensive. From energy and food to electronics, the cost of living rises significantly. But for overseas tourists and investors, yen depreciation means traveling to Japan, shopping, or buying Japanese assets (such as real estate and stocks), becomes cheaper. For people in Taiwan and Malaysia, the appeal of traveling to Japan increases significantly, but they should also note that prices of imported Japanese goods may rise.

Q: Will the Bank of Japan continue raising rates in the future?

A: The market generally expects the Bank of Japan to continue raising rates, but the process will be very slow and gradual. According to analyses by multiple authoritative institutions, the next possible rate hike may take place in the second half of 2026 or early 2027. The central bank’s decision will depend heavily on future economic data, especially whether inflation can remain stable above the 2% target and whether wage growth can continue. Before confirming that the economy has entered a steady recovery path, the central bank will make every effort to avoid hurting the economy through overly rapid tightening.

Q: How long will yen depreciation last? Is a reversal in the exchange rate possible?

A: When the yen exchange rate reverses depends on two key factors: changes in the US-Japan interest rate differential and a shift in market expectations. When the US Federal Reserve (Fed) clearly starts a rate-cutting cycle and the Bank of Japan (BOJ) continues raising rates gradually, the interest rate differential between the two will narrow, easing depreciation pressure on the yen. In addition, if Japan’s inflation and wage growth data remain strong, convincing the market that the Japanese economy has fully escaped deflation and restoring investor confidence, only then may a trend reversal in the yen become visible.