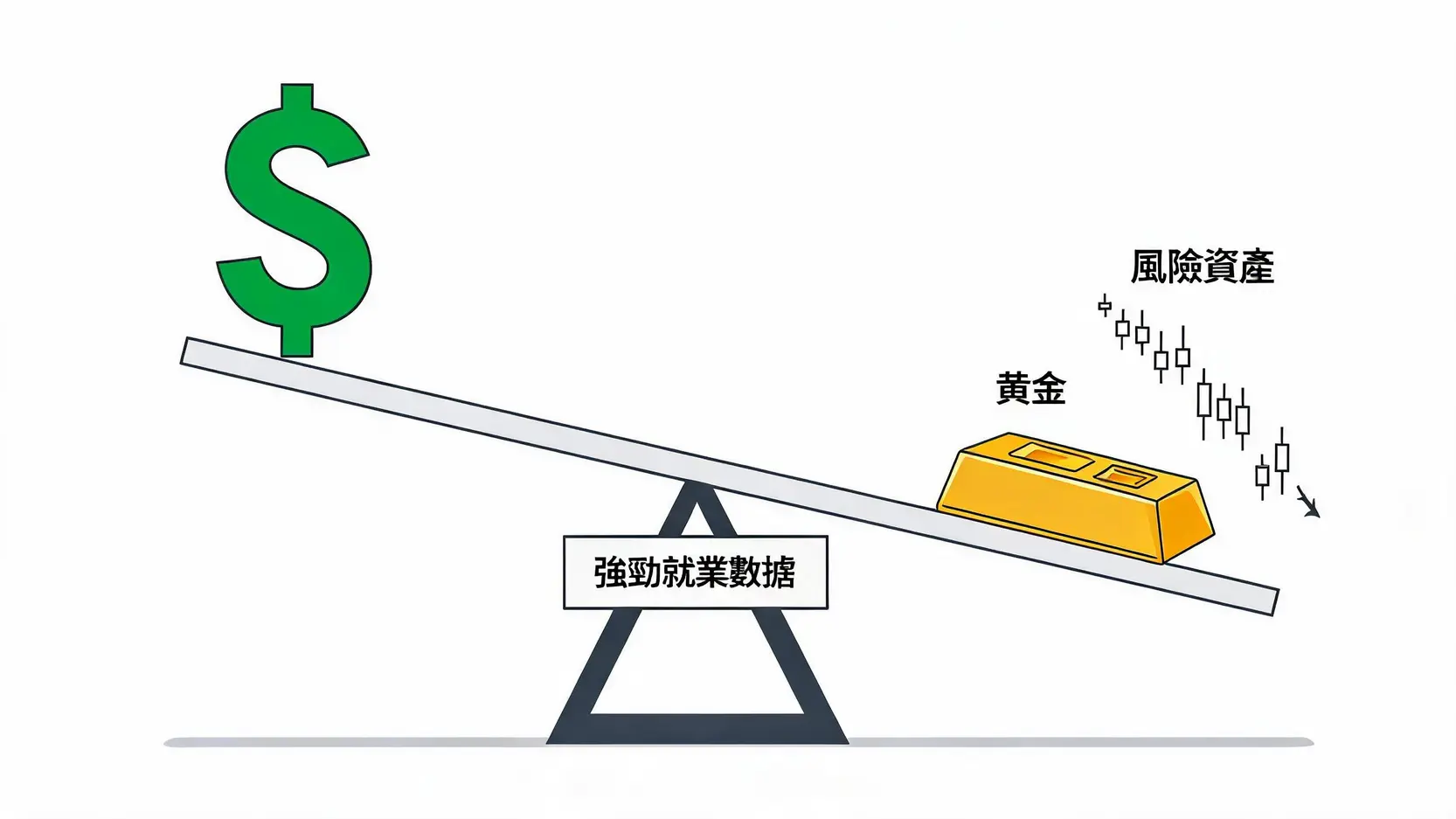

After the Release of the Nonfarm Payrolls Report, Global Assets Moved in Opposite Directions

Why Did the US Dollar Index Surge? Interest Rate Differentials and Safe-Haven Demand

The US dollar’s strength was driven by two key factors:

- Interest Rate Differential: As markets expect the US to maintain relatively high interest rates while other major economies (such as Europe and Japan) may begin cutting rates sooner, US dollar-denominated assets (including US dollar deposits and US Treasury securities) become relatively more attractive. International capital flows into the US dollar in pursuit of higher returns, pushing the US Dollar Index (DXY) higher.

- Risk-Off Sentiment: The market volatility triggered by the nonfarm payrolls report increased investor uncertainty. During periods of market turbulence, the US dollar, as the world’s primary reserve and settlement currency, naturally becomes the preferred safe-haven asset. After selling equities and other risk assets, investors often move into US dollar cash positions, providing additional support for the dollar.

Why Was Gold Hit Hard? The Opportunity Cost of Non-Yielding Assets

As a non-interest-bearing asset, gold is highly sensitive to changes in interest rates. When interest rates rise, the “opportunity cost” of holding gold also increases. Opportunity cost refers to the interest income investors forgo by allocating capital to gold instead of placing it in bank deposits or interest-bearing bonds. The higher interest rates rise, the greater the forgone return, reducing gold’s relative attractiveness. In addition, a stronger US dollar also puts pressure on gold prices, as gold becomes more expensive for buyers using other currencies.

Why Are US and Hong Kong Stocks Under Pressure? The Impact of Higher Interest Rates on Businesses

Equity markets, particularly growth stocks such as technology companies, are especially sensitive to higher interest rates.

- Higher Corporate Borrowing Costs: Rising interest rates increase financing costs for businesses, whether for expansion or day-to-day operations, directly reducing corporate profitability.

- Higher Discount Rates for Future Cash Flows: When valuing a company, analysts discount its expected future cash flows back to their present value. The discount rate is typically positively correlated with the risk-free interest rate (such as US Treasury yields). As interest rates rise, discount rates also increase, resulting in lower company valuations.

- Concerns Over the Economic Outlook: Although employment data remains strong, the market is concerned that if the Federal Reserve keeps interest rates elevated for too long to combat inflation, it could ultimately over-tighten monetary policy and trigger a hard landing, threatening future corporate earnings.

Emerging markets, including Hong Kong, face even greater pressure because a stronger US dollar often encourages capital to flow out of emerging markets and back into the US, tightening liquidity in local markets.

Looking Beyond the Headlines: Wall Street Analysts Identify “Hidden Weaknesses” in the Nonfarm Payrolls Report

Although the latest nonfarm payrolls report appeared exceptionally strong on the surface, several Wall Street analysts who examined the data more closely identified underlying structural weaknesses, or “hidden risks”. These details suggest that the labor market may not be as healthy as the headline figures imply and could introduce additional uncertainty into the path toward a “soft landing”.

Employment Structure Analysis: Changes in Part-Time and Full-Time Employment

The nonfarm payrolls report consists of two separate surveys. The “Establishment Survey”, conducted among businesses, produced an impressive gain of 355,000 new jobs. The “Household Survey”, meanwhile, is used to calculate the unemployment rate.

The devil is often in the details. Analysts have found that, according to the “Household Survey”, the number of full-time jobs may have actually declined, while most of the employment gains were driven by part-time positions and self-employed workers (the gig economy). This could reflect several underlying issues:

- Economic Uncertainty: Businesses may be uncertain about the economic outlook and therefore prefer hiring more flexible part-time workers instead of committing to permanent full-time positions.

- Household Financial Pressure: More individuals may be taking on multiple part-time jobs because income from a single full-time job is no longer sufficient to keep up with inflation.

If this trend continues, it would suggest that the “quality” of employment is deteriorating, which is not an entirely healthy signal.

The Truth Behind the Labor Force Participation Rate: Hidden Economic Warning Signs

The Labor Force Participation Rate measures the percentage of the working-age population that is either employed or actively seeking work. In this report, the participation rate remained unchanged or edged slightly lower.

A stagnant participation rate, particularly when participation among certain demographic groups, (such as prime-age men) has yet to return to pre-pandemic levels, raises concerns. It may indicate that:

- Some workers have permanently left the labor force because of skill mismatches, health issues, early retirement, or other reasons.

- This further intensifies labor shortages, putting additional upward pressure on wages and making inflation more difficult to control.

Therefore, an exceptionally low unemployment rate deserves closer scrutiny if it is not accompanied by a meaningful improvement in labor force participation.

Assessing the Real Impact on the Prospect of a Soft Landing

Taking these “hidden risks” into account, the outlook for a “soft landing” where inflation is brought under control without triggering a severe recession, deserves a more cautious assessment.

On one hand, the strong headline employment figures give the Federal Reserve confidence to maintain higher interest rates in its fight against inflation. On the other hand, structural issues such as declining job quality and stagnant labor force participation resemble warning signals from within the economy. If the Federal Reserve relies too heavily on the headline data and maintains an excessively restrictive policy stance, it could overlook these underlying vulnerabilities and increase the risk of a future “hard landing”. This is precisely where the market remains deeply divided and why leading investors continue to hold sharply different views.

Frequently Asked Questions (FAQ)

Q: What Specific Impact Does Stronger-Than-Expected Nonfarm Payrolls Data Have on My US Stock Investments?

A: In the short term, strong nonfarm payrolls data is usually unfavorable for the stock market. This is because it reduces expectations for Fed rate cuts and pushes interest rates higher, which increases corporate borrowing costs and lowers stock valuations. The pressure is especially greater on interest rate-sensitive technology and growth stocks (such as NASDAQ constituents). However, the impact may differ for certain sectors. For example, banks may benefit from higher interest rates as net interest margins expand. Therefore, investors should review their portfolios, assess their exposure to interest rate risk, and consider whether to increase allocations to value stocks or defensive sectors.

Q: With Rate Cut Expectations Cooling, Is Now a Good Time to Buy Gold?

A: Against the backdrop of cooling rate cut expectations and a stronger US dollar, gold usually comes under greater short-term pressure. This is because higher interest rates increase the opportunity cost of holding a non-yielding asset like gold. However, from a long-term perspective, gold remains an important safe-haven asset. If the market worries that excessive tightening by the Fed could lead to a future economic recession, or if geopolitical risks intensify, safe-haven demand for gold may recover. For investors seeking diversified allocation, it may be reasonable to consider building positions gradually during gold price pullbacks, but it is not advisable to commit a large amount of capital to chase prices higher at this stage.

Q: Will the US Dollar Stay Strong Forever?

A: How long the US dollar can remain strong depends on multiple factors. The first is the divergence in economic performance and monetary policy between the US and other major economies (such as Europe, China, and Japan). If the US economy remains strong while other regions remain weak, interest rate differentials will continue to support the US dollar. The second is global risk sentiment. The more turbulent the market becomes, the stronger the US dollar’s safe-haven status becomes. However, future US inflation data (CPI) should also be closely monitored. If inflation cools faster than expected, the Fed’s stance may shift again, and the US dollar’s strength could then be disrupted. Therefore, tracking upcoming key economic data is essential.

Conclusion

In summary, a strong, stronger-than-expected nonfarm payrolls report has landed like a shockwave across global financial markets. It directly challenged the market’s optimistic expectations for near-term Fed rate cuts, triggered a chain reaction of cooling rate cut expectations, and reinforced the” US dollar’s dominant” position as the only asset holding firm among global assets. For investors, this means they must reassess the possibility that the high interest rate environment may last longer and adjust their asset allocation accordingly.

More importantly, we cannot focus only on the surface of the data. A deeper look into the potential “hidden risks” in the report, such as employment structure and labor force participation, can help us better understand the real health of the US economy. In a market where data and expectations are constantly competing, staying cautious and paying attention to details will be key to finding certainty amid uncertainty.