Interpreting Central Bank Rhetoric Through Macquarie’s Forecast: How Should Traders Read Policy Signals?

Interpreting central bank rhetoric through Macquarie’s forecast has never been just about “what the investment bank said”, but about how to connect central bank rhetoric analysis, hawkish and dovish signals, and market expectation-gap trading into an executable framework. For market participants in Taiwan and Malaysia, which are highly affected by the US dollar, interest rates, and capital flows, a seemingly conservative phrase from a central bank often moves exchange rates, bond markets, and stock market volatility earlier than whether interest rates are actually adjusted. What is truly useful is not memorizing a few keywords, but understanding how investment banks build forecasts, why central banks deliberately leave room for ambiguity, and why the market often “announces as expected, yet moves in the opposite direction”.

If you usually find policy statements too wordy and scattered, this article will break down the interpretation process: first, how investment bank forecasts are formed, then how central banks manage expectations through tone, and finally, the one thing traders care about most: how to turn rhetoric into risk-controlled decisions.

Why Investment Bank Forecasts Can Become an Important Reference for Interpreting Central Bank Rhetoric

The reason the market pays attention to forecasts from large investment banks such as Macquarie is not because they are always right, but because they often provide a more complete interpretation framework than retail investors. Before a meeting, investment banks integrate inflation, wages, employment, retail sales, PMI, financial conditions, bond yield curves, and even details from recent official speeches to estimate the central bank’s next step. These data points themselves are not mysterious. The difference lies in integration ability and narrative ability.

In other words, the value of an investment bank report is not only in predicting a rate hike or rate cut, but in telling the market which variable the central bank cares about most, which sentence may change the policy bias, and which risk is currently being underestimated. When several large institutions hold similar views, a market consensus gradually forms, which then affects interest rate futures, forex options, and stock and bond allocation.

How Investment Banks Build Forecasts From Data, Pre-Meeting Signals, and Official Speeches

A mature central bank forecast usually does not rely on a single number, but on three layers of cross-checking:

Soft signals: Official speeches, meeting minutes, media signaling, policy research articles.

Market pricing: Interest rate futures, short-term government bond yields, the US Dollar Index, and risk asset reactions.

Taking the Federal Reserve as an example, if inflation is slowing at a weaker pace, the labor market remains resilient, and the chair’s press conference emphasizes that “more evidence is still needed”, then even if the Fed holds steady this time, the market may still interpret it as hawkish. At this point, investment banks will focus on tone rather than the result itself. To view the official original context, you can directly compare the Federal Reserve’s monetary policy meetings and statements, then go back and see whether the market has overextended its interpretation.

Why the Market Uses Major Institutional Views to Calibrate Policy Expectations

Because the market trades “expectation gaps”, not textbook answers. If an investment bank is the first to propose a framework that says “the central bank is neutral on the surface, but actually hawkish”, and the subsequently released statement happens to echo this, capital will quickly crowd in that direction. This is also why many times, even when the news headline says “interest rates remain unchanged”, bonds, exchange rates, and technology stocks still fluctuate sharply.

For investors, the core takeaway from interpreting central bank rhetoric through Macquarie’s forecast is learning to understand which side the market is currently standing on: fully priced in, not yet priced in, or completely misread. These three situations have completely different meanings for subsequent market movements.

How to Read Central Bank Rhetoric Without Only Looking at Surface-Level Words

When most people read a central bank statement for the first time, the easiest mistake is treating every sentence as a straightforward statement. In fact, central bank wording is usually carefully designed balancing language: it must preserve policy flexibility, manage market sentiment, and avoid committing too early. What you truly need to look at is the change in wording, not a single sentence itself.

For example, “inflation remains above target” and “inflation is moving back toward target” may look similar, but their implications for the interest rate path are completely different. Another example is that “the committee will continue to assess the data” is a neutral reservation, while “further tightening is not ruled out if necessary” carries a clear anti-inflation stance. These details are where central bank rhetoric analysis most easily creates a gap in interpretation.

Hawkish Keywords, Dovish Keywords, and Option-Preserving Statements

You can start interpretation from three types of terms:

Hawkish terms: Inflation pressure, persistence, restrictive policy, upside risks, more confidence needed, not yet sufficient.

Option-preserving terms: Data-dependent, meeting-by-meeting decisions, no preset path, closely monitoring.

Among these, the third category is often the most worth watching. This is because what makes central banks truly skillful is not saying things clearly, but preserving ambiguity. Such wording prevents the market from locking in the future path all at once, and also causes prices to be repriced whenever new data appears.

How the Same Sentence Can Have Different Market Meanings in Different Economic Cycles

This is a key point that many people overlook: the same sentence can be interpreted completely differently by the market when placed in different periods.

For example, if “policy remains restrictive” appears when high inflation has just started to fall, the market may interpret it as interest rates staying high for longer. But if it appears after growth has clearly slowed and unemployment has risen, the market may instead feel that the central bank is already close to pivoting and is simply unwilling to soften its stance too early verbally.

So when interpreting central bank rhetoric through Macquarie’s forecast, you cannot just focus on the literal wording. You also need to ask three questions:

What did the market originally expect?

Where is the current economic cycle?

Is the central bank more concerned about inflation this time than last time, or more concerned about growth?

If these three questions are not answered first, simply reading a news summary can easily cause you to see neutrality as dovishness, or reservation as hawkishness.

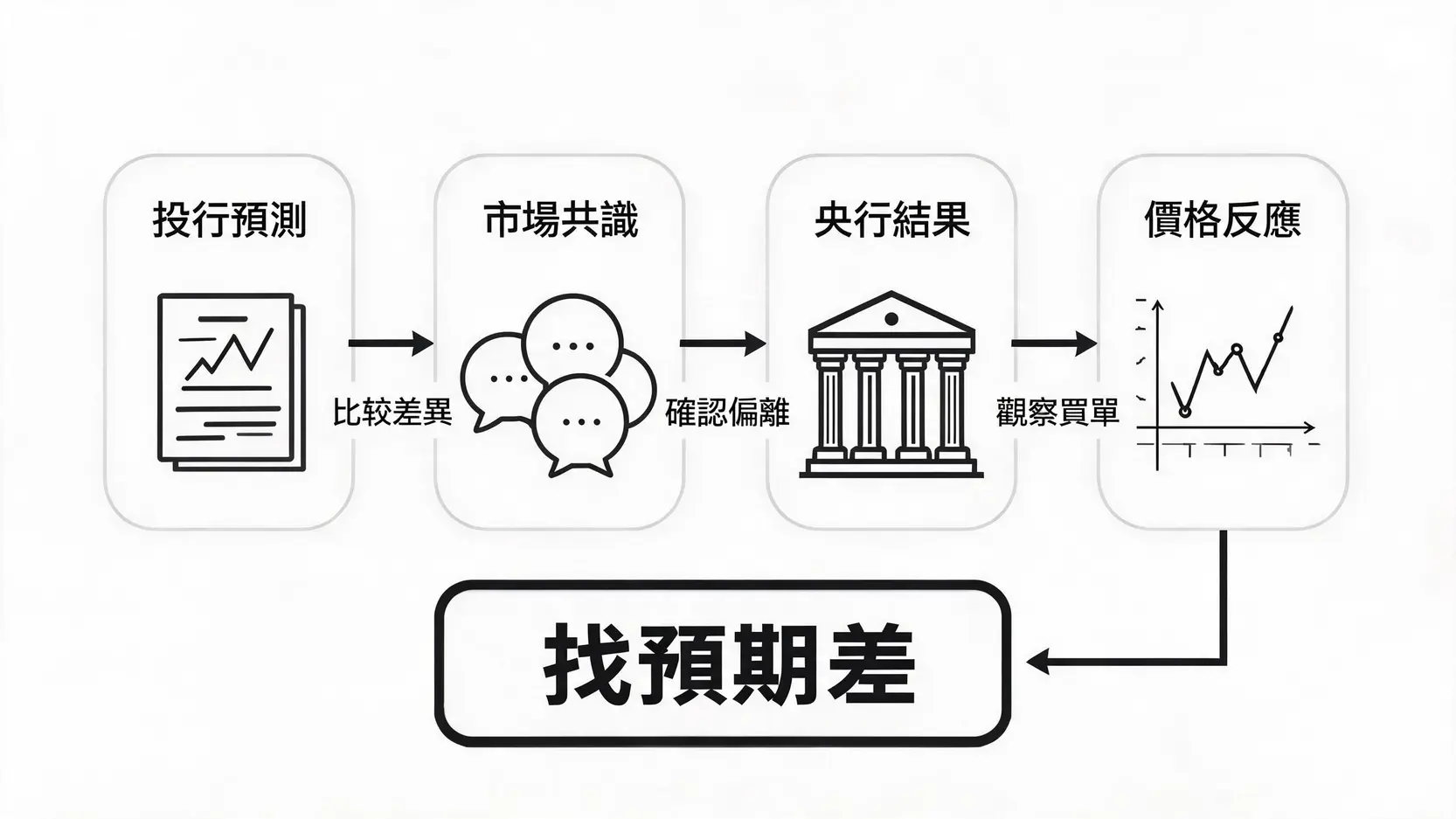

From Forecast to Trading: How to Use Market Expectation-Gap Trading to Transform Central Bank Rhetoric Analysis

Truly mature traders will not chase prices directly just because they see an investment bank report. Instead, they first compare three levels: investment bank forecasts, mainstream consensus, and the extent to which asset prices have already reflected them. Only when a gap appears among these three is there an opportunity worth watching.

The reason central bank-driven markets are difficult to trade is that the market often does not react to the event itself, but to “the gap between the event and expectations”. Interest rates may stay unchanged as expected, yet the US dollar rises sharply; or the dot plot may show no obvious change, yet the stock market gaps higher. Behind these moves, expectation gaps are actually at work.

First Compare Investment Bank Forecasts With Market Consensus, Then See Whether the Central Bank Deviates

The process can be simplified into the table below:

Step

What to Watch

Practical Use

Investment Bank Forecasts

Scenario analysis from institutions such as Macquarie

Understand the professional market framework

Market Consensus

Interest rate futures and mainstream media narratives

Understand the direction that has already been priced in

Observe which signal the market is truly buying into

For example, if the market broadly bets on a dovish stance, but the central bank merely removes one easing-leaning phrase without actually raising interest rates, asset prices may still be repriced sharply. This is the most common “small wording change, big volatility” in central bank rhetoric analysis.

What traders truly focus on is not the event itself, but the gap between investment bank forecasts, market consensus, and the central bank outcome.

Break Rhetoric Down Into Four Major Signals: Growth, Inflation, Employment, and Risk

To read a statement more systematically, you can directly divide it into four parts:

Growth: Whether economic activity is solid, slowing, or losing momentum.

Inflation: Whether the pace of decline is sufficient, and whether core pressure remains sticky.

Employment: Whether the labor market is tight, balanced, or deteriorating.

Risk: Financial conditions, geopolitical risks, tariffs, and commodity price volatility.

If a statement mentions both “slowing growth” and “still-sticky inflation”, it means the central bank has entered a more difficult operating zone, and market volatility will usually rise as well. For investors in Taiwan and Malaysia, this kind of environment especially requires close attention to the US dollar, export cycles, and foreign capital flows, because local markets often reflect global funding costs first before reflecting local fundamentals.

Taiwanese readers who want to compare local official wording can also refer to the Central Bank Board of Directors and Supervisors Joint Meeting Resolution Press Release. Looking at the wording of the local central bank and the Federal Reserve side by side makes it easier to understand how different central banks choose different communication methods in similar environments.

Avoid Overreliance on a Single Investment Bank View: Build Your Own Interpretation Checklist

Macquarie’s forecast can be read, but it should not be accepted wholesale. The reason is simple: investment banks can also be wrong, and sometimes the issue is not the direction, but the timing. If the market trades its logic two months in advance, by the time the meeting day arrives, it may instead result in “positive catalysts exhausted” or “negative catalysts losing impact”.

A more prudent approach is to build your own interpretation checklist:

Is market pricing for this meeting too one-sided?

Compared with the previous statement, which words were removed and which words were added?

Did the chair’s press conference revise the assumption the market cares about most?

Are bond yields and the US dollar reacting consistently?

Is the stock market rising because risk appetite has improved, or is it merely a short squeeze?

As long as these five questions are standardized, interpreting central bank rhetoric through Macquarie’s forecast will no longer stay at the level of news reading, but will become a decision-making process that can be repeatedly verified.

When Investment Bank Forecasts Miss the Mark, Does Central Bank Rhetoric Analysis Still Have Reference Value?

Yes, and it is often even more valuable. Because when a forecast misses the mark, the most worth studying is not “who guessed wrong”, but why the market originally made that guess, and at which point the central bank deliberately chose not to follow the market’s script.

For example, if investment banks forecast a dovish stance, but the central bank ultimately stays neutral to hawkish, it means the central bank may still be worried about a rebound in inflation, overheated asset prices, or may be unwilling to let the market loosen financial conditions too early. This gap itself is the starting point of the next market move. Many times, large volatility does not come from the meeting result, but from “the market being forced to revise its originally too-comfortable consensus”.

Therefore, central bank rhetoric analysis should not only be used when the forecast is correct. It should also be used in reverse when the forecast is wrong to recalibrate your own model. This is the key to turning information into experience.

FAQ

Which has a greater impact on the market, central bank rhetoric or the interest rate number?

Many times, rhetoric has a greater impact. If the interest rate decision has already been fully expected by the market, what truly drives prices is the statement content, press conference tone, dot plot changes, and hints about the future policy path. In other words, the market trades the future, not just this one number.

Do investment bank forecasts still have reference value when they miss the mark?

Yes. Even if the direction is inaccurate, investment bank reports can still help you understand the market’s mainstream assumptions and focus at the time. As long as you further compare the central bank’s final wording with the differences in market pricing, you can find the next area for adjustment. Missing the mark does not mean it is useless. Instead, it often provides more valuable material for reflection.

How should beginners quickly identify hawkish and dovish wording?

Start with keywords, then look at the context. Phrases such as “inflation remains high” and “policy needs to remain restrictive” are usually hawkish; phrases such as “inflation continues to slow” and “growth downside risks are rising” are usually dovish. But what matters more is comparing differences between the previous and current versions, rather than looking at one sentence in isolation.

Why does the market surge or plunge when the central bank clearly has not done much?

Because the market reacts to expectation gaps. When investors originally bet on a more hawkish or more dovish stance, even if the central bank only says one sentence less or preserves one degree of flexibility, it may cause capital to reprice. So “no action” does not mean “no signal”.

Why should investors in Taiwan and Malaysia also pay attention to rhetoric from major central banks?

Because global funding costs, the direction of the US dollar, export demand, and foreign capital allocation all affect local stock, currency, and bond markets. Changes in rhetoric from the Federal Reserve, European Central Bank, or Reserve Bank of Australia often indirectly affect Taiwanese stocks, Malaysian stocks, technology stock valuations, and bond returns through exchange rates and risk appetite.

Conclusion

The real value of interpreting central bank rhetoric through Macquarie’s forecast is not finding the “most accurate” report, but learning to break down three layers of information: what the market originally expected, what the central bank actually said, and how prices ultimately reacted. As long as these three things are connected, many market moves that originally seemed contradictory can actually be traced back to a clear context.

For traders and medium- to long-term investors, the most important thing is not guessing correctly in advance every time, but gradually building their own interpretation framework. When you can place hawkishness, dovishness, option preservation, expectation gaps, and risk pricing on the same map, central bank statements will no longer be difficult text, but a market language that can be interpreted, verified, and used for risk management.

A Complete Analysis of Central Bank Policy Shifts: From YCC to QT, Decoding the BOJ and the Fed’s Next Move The Bank of Japan (BOJ) and the US Federal Reserve (Fed), two giants of the global financial markets, are seeing their diverging monetary policy directions become the core force driving...

Have Yen Appreciation Expectations Been Established? A Complete Analysis of 2026 Investment Bank Forecasts, Revealing the Key Turning Point Mainstream View: Why Does the Market Generally Expect the Yen to Appreciate in 2026? After a long period of historic depreciation, the market has seen a significant shift in expectations for...

When Will the Bank of Japan’s Next Rate Hike Arrive? 2026 Expert Forecasts and Investor Response Strategies Decision-Making Basis for the Bank of Japan’s Future Interest Rate Policy The Bank of Japan ended its eight-year negative interest rate policy in early 2026, sending a shockwave through global financial markets. The...