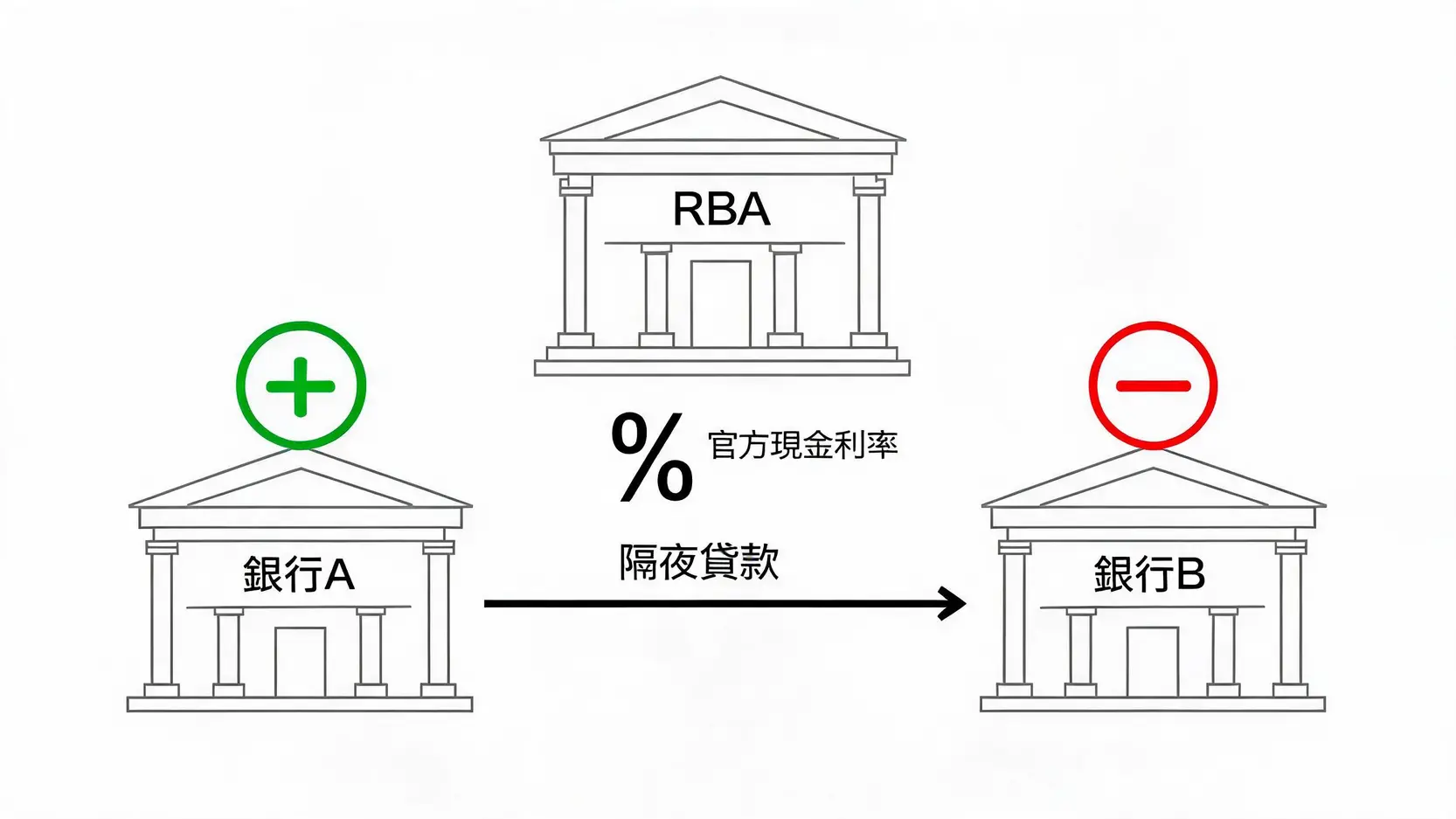

Changes to the RBA’s Cash Rate ripple through the economy, affecting both personal finances and overall economic activity.

Impact on Home Loans: How Interest Rate Changes Affect Your Monthly Repayments

This is the most direct and noticeable impact of the Cash Rate on individuals. Most home loans, particularly variable-rate home loans, are closely linked to the Cash Rate.

- When the RBA raises interest rates: Commercial banks typically increase their lending rates, meaning your monthly mortgage repayments rise and your disposable income decreases.

- When the RBA cuts interest rates: Banks generally lower their lending rates, reducing your monthly mortgage repayments and leaving you with more money for spending or saving.

For households with home loans worth hundreds of thousands of Australian dollars, even a small 0.25% change can result in annual repayment differences of several thousand Australian dollars.

Further Reading (Highly Recommended)

What Are Investment Risks? A Complete Guide to the Five Most Common Types of Investment Risk for Beginners…

How Do Stocks Make Money? An Investment Guide From Market Trend Analysis to Identifying Bull and Bear Markets…

Impact on Savings Interest: How Your Savings Account Returns Change

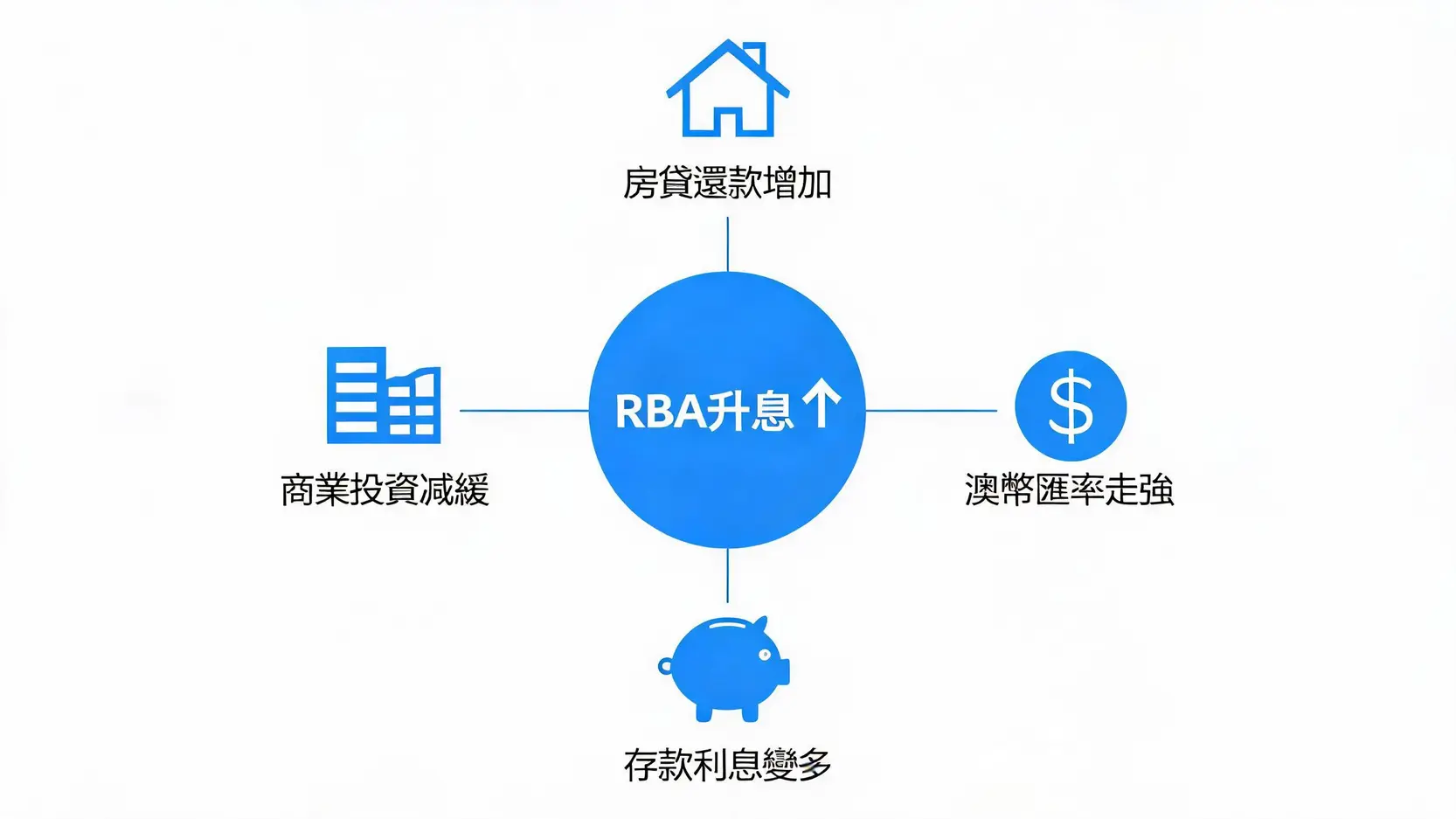

The same principle applies to savings. When the Cash Rate rises, banks generally increase interest rates on savings accounts and term deposits to attract more deposits, which benefits savers. Conversely, when the Cash Rate falls, the interest earned on your savings also declines. This explains why many people seek higher-return investment options during periods of low interest rates instead of simply leaving their money in the bank.

Impact on the Australian Dollar Exchange Rate: Why Interest Rate Decisions Affect the Foreign Exchange Market

The Cash Rate is one of the key factors influencing the Australian dollar (AUD) exchange rate. International investors (particularly large institutional funds) seek countries with higher interest rates to earn better returns on their capital, a strategy known as the “carry trade”.

- Rate hikes: Higher interest rates attract more overseas capital into Australia, increasing demand for the Australian dollar and causing it to appreciate.

- Rate cuts: Lower interest rates reduce Australia’s appeal to overseas investors, potentially leading to capital outflows and depreciation of the Australian dollar.

The strength of the Australian dollar affects the prices of imported and exported goods, which in turn influences the cost of living. If you would like to learn more about how the foreign exchange market works, refer to this article: Forex Trading Guide for Beginners: Learn the Basics of Forex Trading From 0 to 1!

Impact on the Labor Market and Business Investment

Changes in the Cash Rate also have a profound impact on business decisions and the labor market. A low-interest-rate environment reduces borrowing costs for businesses, making them more willing to borrow to expand operations, develop new projects, or hire additional employees, thereby supporting employment growth. Conversely, a high-interest-rate environment increases financing costs, which may lead businesses to scale back investment plans or even reduce their workforce, putting pressure on employment. As a result, when making interest rate decisions, the RBA always seeks a delicate balance between controlling inflation and supporting employment.

How Can You Check Australia’s Current Cash Rate and Historical Data?

Accessing official information is the foundation of making informed financial decisions. Checking Australia’s interest rate trends and current data is straightforward, and the following are several authoritative sources.

How to Check the RBA’s Official Website

The most authoritative and up-to-date source of information is always the official website of the Reserve Bank of Australia (RBA). You can visit its Cash Rate Target statistics page directly.

This page provides:

- Current Cash Rate Target: The latest official interest rate. As of June 2026, Australia’s Cash Rate is 4.35%.

- Interactive charts: You can customize the time period to view interest rate movements over several decades.

- Historical data tables: Detailed historical data is available for download and analysis.

How to Read the Historical Cash Rate Chart: Understanding the Highs and Lows Over the Past Decades

When viewing the historical chart, you will notice several interesting patterns:

- Periods of high interest rates: In the early 1990s, to combat inflation of up to 8%, the Cash Rate climbed to more than 17%. This reflected the central bank’s aggressive tightening policy during a period of economic overheating.

- Periods of low interest rates: During the 2008 Global Financial Crisis (GFC) and the 2020 COVID-19 pandemic, the RBA rapidly lowered interest rates to record lows (reaching as low as 0.1% during the pandemic), to cushion the economic downturn.

By studying these historical peaks and troughs, you can gain a deeper understanding of how interest rate policy serves as a tool for responding to major economic events and where today’s interest rate environment sits in historical context.

Recommended Tools: Financial Data Websites and Apps

In addition to the RBA’s official website, many leading financial news websites and apps provide real-time interest rate information and professional analysis, including:

- Bloomberg, Reuters: Professional global financial data and news.

- Major banking apps: Your bank’s app will typically send interest rate decision updates and analysis on policy announcement days.

- Financial news outlets: Such as the Australian Financial Review (AFR), which provides in-depth analysis and market forecasts.

Practical Calculation! How Much Will an Interest Rate Change Affect My Mortgage?

Theory is one thing, but calculating it yourself is the best way to understand how an interest rate change affects your monthly mortgage repayments. This can help you better plan your household budget and prepare for future market changes.

A Simple Formula or Online Calculator

You can use a very simple formula to estimate the change in your monthly repayments:

Monthly Repayment Change ≈ (Total Loan Amount × Interest Rate Change) ÷ 12

For example, a “one-step” rate hike, or “25 basis points”, equals 0.25% (or 0.0025). Many banks and third-party financial comparison websites also provide free online mortgage calculators that can more accurately calculate repayments, including both principal and interest.

Example: Monthly Repayment Difference on a AUD 500,000 Mortgage After a 25 Basis Point Rate Hike or Rate Cut

Assume you have a home loan of AUD 500,000. Let’s see how a one-step rate hike or rate cut (0.25%) would affect your monthly mortgage repayments:

| Interest Rate Change |

Calculation |

Monthly Repayment Change

|

Annual Change |

| Rate Hike 0.25% |

(500,000 × 0.0025) ÷ 12 |

Approximately +$104 |

Approximately +$1,250 |

| Rate Cut 0.25% |

(500,000 × 0.0025) ÷ 12 |

Approximately -$104 |

Approximately -$1,250 |

As shown in the table above, even a seemingly small 0.25% change can represent a significant additional expense or saving for the average household. This also highlights the importance of conducting a stress test before applying for a loan.

Further Reading (Highly Recommended)

What Are Investment Risks? A Complete Guide to the Five Most Common Types of Investment Risk for Beginners…

Forex Trading Guide for Beginners: Learn the Basics of Forex Trading From 0 to 1!

Strategies for Variable-Rate and Fixed-Rate Home Loans

When interest rates fluctuate, different types of home loans require different strategies:

- Variable Rate: Your interest rate moves with market conditions. This type of loan is generally more advantageous when interest rates are expected to fall. Strategically, you can use Extra Repayments and an Offset Account to pay down your principal more quickly, reduce your total interest costs, and build a buffer against potential future rate hikes.

- Fixed Rate: Your interest rate remains unchanged for the fixed term (typically one to five years), regardless of market fluctuations, making budgeting easier. Locking in a lower fixed rate before interest rates are expected to rise can be a wise decision. However, the downside is reduced flexibility, as additional repayments are usually subject to restrictions.

FAQ

Q: What is the RBA’s inflation target?

A: The Reserve Bank of Australia’s (RBA) long-term inflation target is to keep the annual growth rate of the Consumer Price Index (CPI) within a range of 2% to 3%. This target aims to maintain price stability while avoiding deflation and supporting sustainable economic growth.

Q: What is the difference between the Cash Rate and the interest rates offered by banks?

A: The Cash Rate is the RBA’s “policy rate” or “benchmark interest rate”, representing the cost of borrowing between banks. The deposit and lending rates offered by commercial banks are based on the Cash Rate, with a margin added or subtracted. This margin reflects the bank’s operating costs, risk assessment, and profit. As a result, the Cash Rate serves as the “anchor” for all interest rates, but the rate you ultimately receive will differ from it.

Q: Could Australia’s Cash Rate ever become negative?

A: In theory, yes. Some countries (including Japan and the eurozone), have implemented negative interest rate policies. However, senior officials at the Reserve Bank of Australia (RBA) have repeatedly stated that negative interest rates are an “extremely unlikely” option and that they would instead prioritize other unconventional monetary policy tools (such as quantitative easing (QE)). Therefore, the likelihood of negative interest rates in Australia in the foreseeable future is extremely low.

Q: What does a “25 basis point rate hike” mean? What is a basis point?

A: In finance, one “step” generally refers to 25 “basis points” (bps). One basis point equals 0.01%. Therefore, a one-step rate hike means interest rates increase by 0.25%. For example, if the Cash Rate rises by one step from 4.35%, the new rate would be 4.60%. Using “basis points” provides a more precise way to describe small changes in interest rates and helps avoid confusion.

Conclusion

Understanding Australia’s Cash Rate is an essential part of personal financial literacy for every Australian resident. It is more than just an economic statistic. It is a key indicator that directly affects your mortgage, savings, spending power, and even job security. From understanding how the RBA makes its decisions to seeing how those decisions are transmitted through the economy to affect your personal finances, this knowledge will help you better understand financial news and navigate market fluctuations with confidence. We hope this article has given you a clearer understanding of how the Cash Rate works and helped you make more informed financial decisions when interest rates change in the future. By regularly following RBA announcements and considering your own financial situation, you can better navigate an ever-changing economic environment.