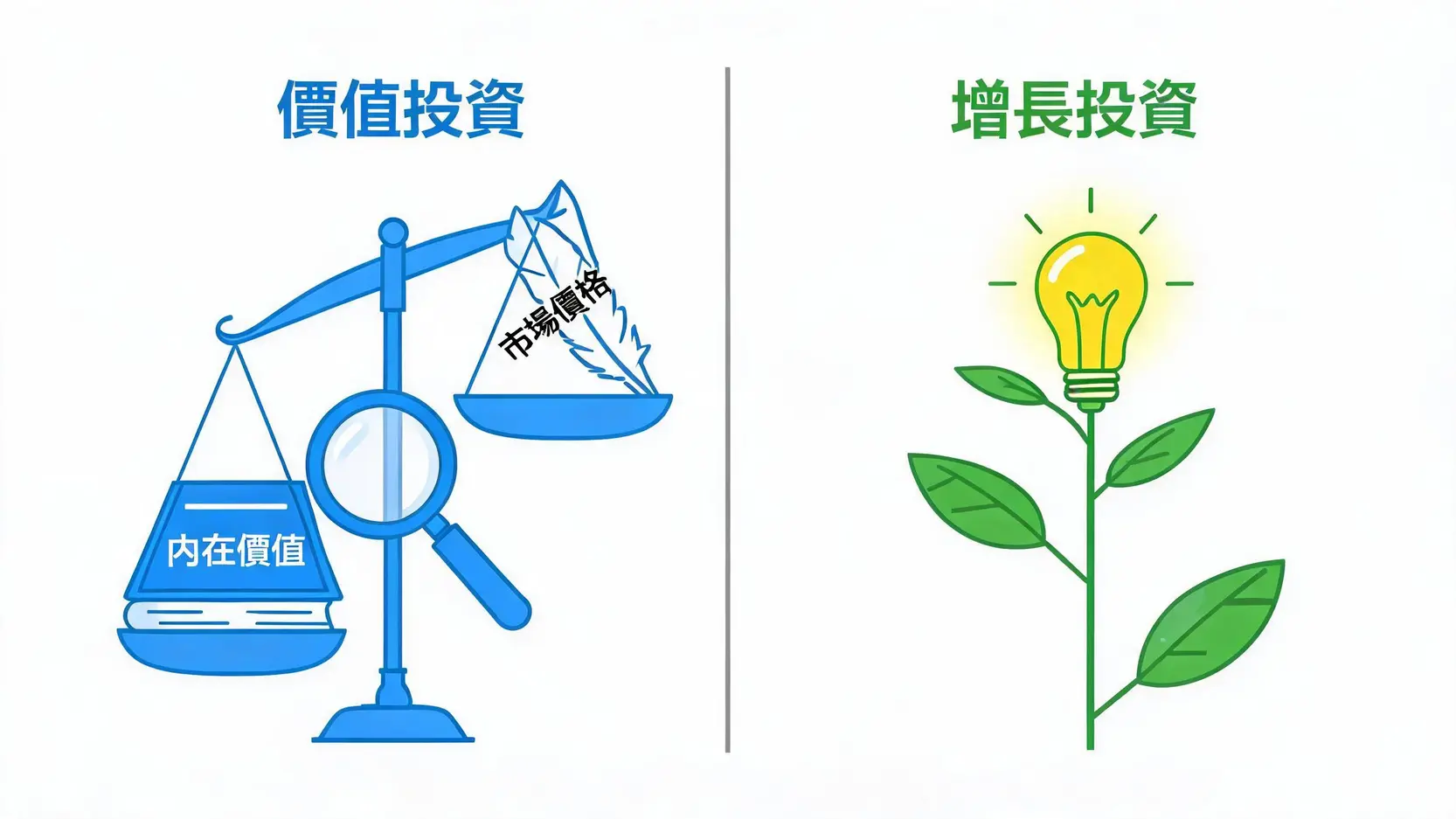

Value investing vs. growth investing: one looks for today’s “quality bargains”, while the other positions for tomorrow’s “future stars”.

Strategy Four: Growth Investing, Positioning for Future Trend Industries

Unlike value investing, growth investing focuses more on a company’s “future growth potential”, rather than whether the current stock price is cheap. Growth investors are willing to pay higher valuations for companies that are in a high-growth stage and whose revenue and profit growth rates far exceed the market average. They look for the next industry or technology that can change the world, such as early-stage technology stocks, electric vehicles, or the artificial intelligence industry. This strategy carries relatively higher risk, but the potential returns can also be very substantial.

Strategy Five: Dividend Growth Investing

This strategy focuses on investing in companies that not only pay dividends steadily, but also continuously increase the amount of dividends paid. These companies are usually mature enterprises with abundant cash flow. Dividend growth not only provides stable passive cash flow income, but the continuous increase in dividends itself is often proof of the company’s healthy fundamentals, which further drives the stock price upward. This is a stable long-term investment strategy that balances cash flow and capital gains.

Further Reading (Highly Recommended)

Bear Market Investment Strategy: What Should You Buy in a Bear Market? A Complete Guide to 5 Bottom-Fishing Techniques and Monthly Stock Investment

What Does a Bull Market Mean? Understand the Definition, Characteristics, and 3 Major Investment Strategies of a Bull Market

How to Screen for Excellent Long-Term Investment Targets?

No matter which strategy you choose, learning how to screen targets suitable for long-term investing is an essential skill. This is not just about looking at whether the stock price is high or low, but about examining the company’s “quality” like a business owner.

Indicator Screening: The Importance of ROE, Gross Margin, and Free Cash Flow

There are many indicators in financial reports, but for long-term investors, the following three are crucial:

- Return on Equity (ROE): Measures how efficiently a company earns money for shareholders. If it remains stable above 15% over the long term, it usually means the company has good profitability and operating efficiency.

- Gross Margin: Represents the pricing power and cost control ability of the company’s products or services. A high and stable gross margin means the company has strong competitiveness in the industry.

- Free Cash Flow: The real cash earned from the company’s operations after paying all operating expenses and capital expenditures. Abundant free cash flow is the foundation for a company to pay dividends, reinvest, or repay debt, and is a key indicator of healthy fundamentals.

Moat Analysis: Identifying Whether a Company Has Long-Term Competitive Advantages

“Moat” is a concept proposed by Buffett, referring to a company’s structural advantage that allows it to resist competitors and maintain high profitability over the long term. Only companies with wide moats can continue creating value for shareholders over long periods. Common types of moats include:

- Intangible assets: Such as strong brands (Coca-Cola) and patents (Pfizer).

- Cost advantages: Having lower production or operating costs than competitors (Costco).

- Network effects: The value of a product or service increases as the number of users grows (Facebook, LINE).

- High switching costs: Users need to pay a high cost to switch to a competitor’s product (banking systems, Apple ecosystem).

Avoiding Value Traps: How to Distinguish Cheap Good Companies From Cheap Bad Companies

When executing a value investing strategy, the greatest fear is falling into a “value trap”. Some stocks appear cheap (such as having a very low price-to-earnings ratio), but in reality, it is because the company’s fundamentals are deteriorating and its future prospects are bleak, causing the stock price to keep falling. The key to distinguishing the two is to ask yourself: “Is this company cheap because of a short-term market misjudgment, or because the company itself has a long-term problem?” A cheap company worth investing in usually has healthy financial fundamentals and a solid moat, but is only temporarily facing industry headwinds or non-operational negative news.

Long-Term Investment Frequently Asked Questions (FAQ)

Q: How long does it take to see results from long-term investing?

A: Long-term investing does not have a fixed timetable, but it is generally believed to require at least 3 to 5 years or more. A complete economic cycle (including both bull and bear markets, is approximately 7 to 10 years). The key is not the length of time, but giving the compounding effect enough time to develop and allowing the intrinsic value of companies to be reflected. Patience is the most important virtue for long-term investors.

Q: If the long-term target I choose keeps falling, when should I sell?

A: This depends on the reason for the stock price decline. You should ask yourself: “Have the reasons I originally bought this company disappeared?” If it is only because of external factors such as market panic or a temporary industry downturn, while the company’s fundamentals (such as its moat and profitability) remain solid, then the continued decline may instead be a good time to add positions. However, if the decline is due to the company losing competitiveness, major management mistakes, or the industry being disrupted, then you should sell decisively. This is called “stop-loss”.

Q: What proportion of my funds should I use for long-term investing?

A: This depends on your age, risk tolerance, and financial goals. Generally speaking, the younger you are, the higher the risk you can tolerate, and the higher the proportion you can allocate to long-term investments (especially stocks), such as 80-90%. As you age and approach retirement, you should gradually reduce the proportion of high-risk assets and shift to more stable assets such as bonds and cash. A simple reference rule is “100 – your age”. The resulting number is the recommended percentage of funds to invest in the stock market.

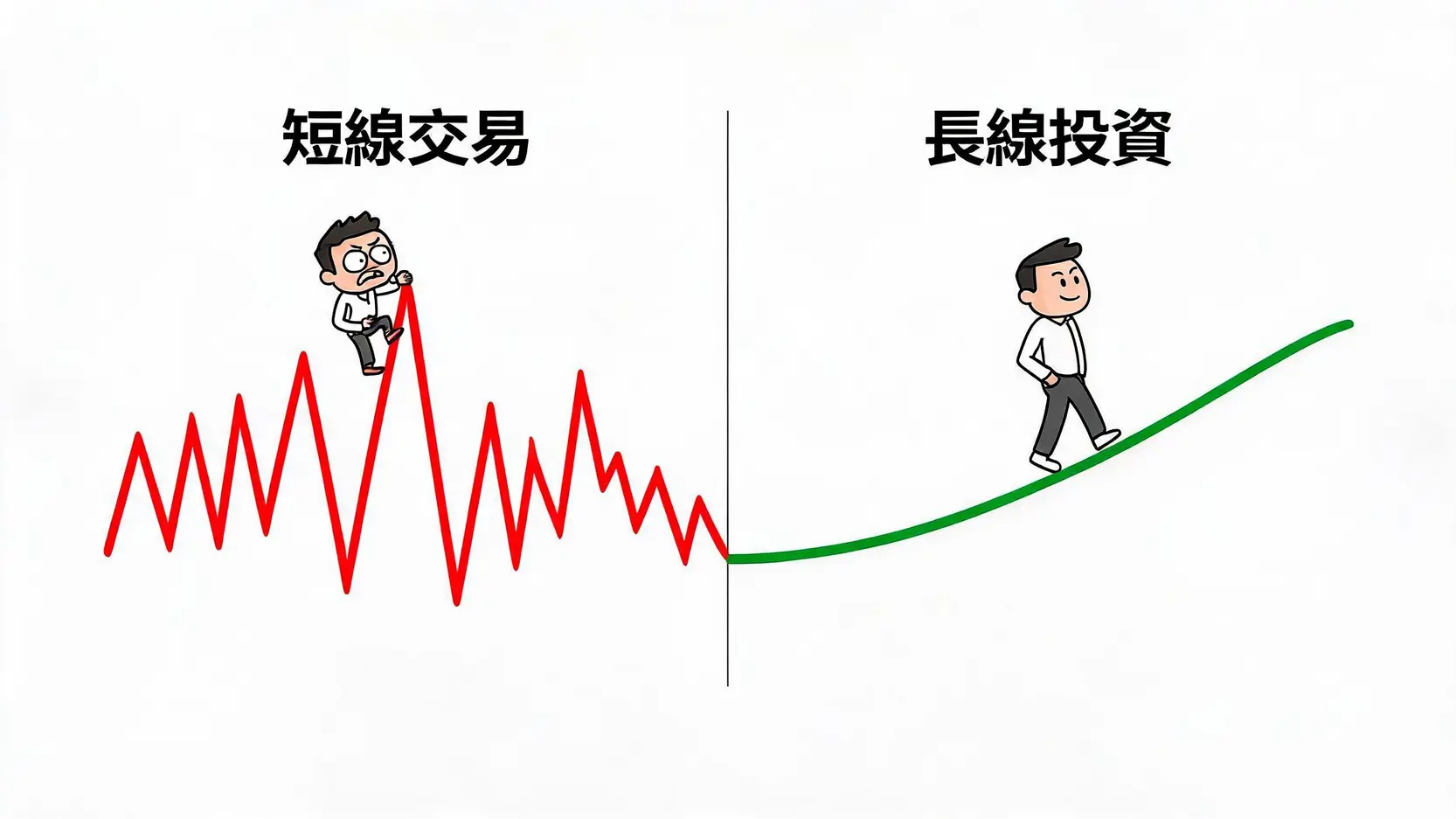

Q: Which is better, long-term investing or short-term investing?

A: There is no absolute good or bad, only whether it is suitable. Short-term investing pursues price differences, requires a large amount of time, precise market judgment, and strict discipline, making it suitable for professional traders. Long-term investing, on the other hand, shares the fruits of corporate growth and is more like a financial management philosophy. It is suitable for the vast majority of ordinary people who hope to accumulate wealth through investing. For beginners, starting with long-term investing is a more stable approach with a higher success rate.

Conclusion

In summary, “long-term investing” is an investment philosophy focused on the future. It does not pursue overnight wealth, but relies on compounding and the long-term value growth of companies to steadily accumulate wealth. It requires investors to have patience, independent thinking, and a focus on company fundamentals rather than short-term market sentiment. Through the five major strategies introduced in this article, including buy and hold, dollar-cost averaging into ETFs, value investing, growth investing, and dividend growth investing, as well as key stock-picking methods, you can begin building a solid investment portfolio for yourself. Start taking action now, choose the long-term investment strategy that suits you best, and let your wealth grow steadily over time.