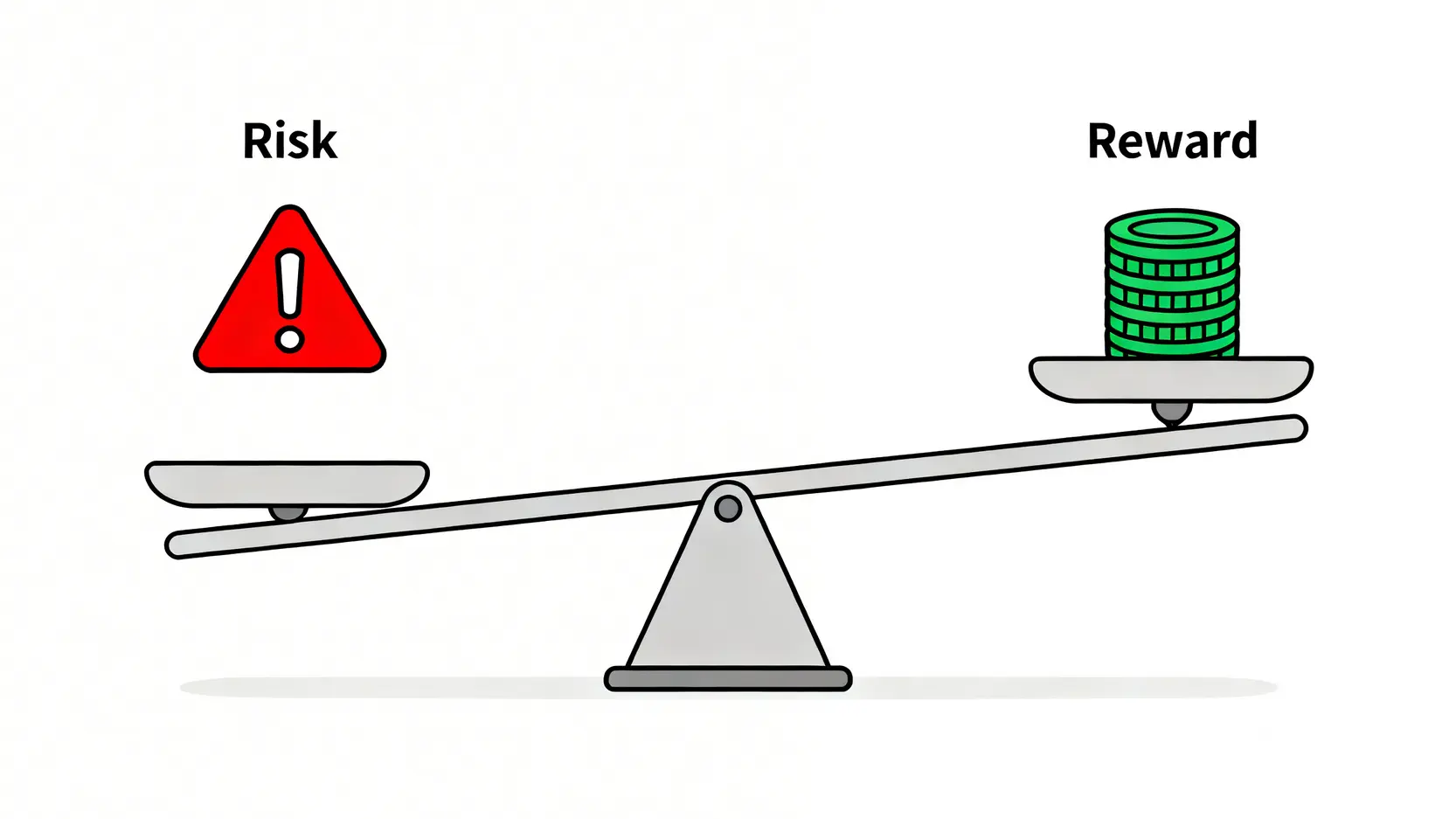

The Art of Balancing Risk and Return: Higher potential returns are usually accompanied by higher potential risks.

What Is the Risk-Reward Ratio? Why Do High Returns Often Come with High Risk?

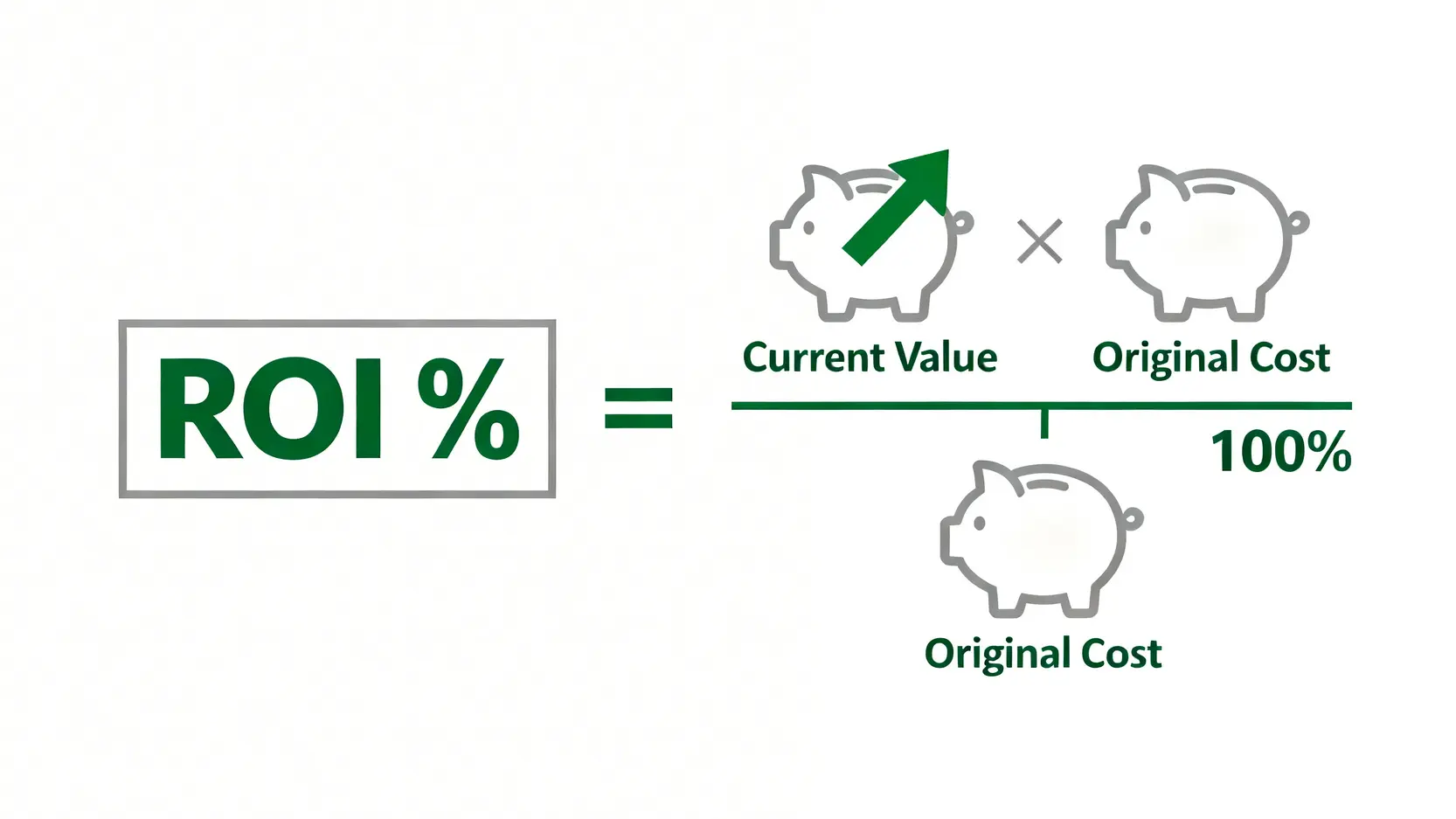

The risk-reward ratio is a metric used to measure potential returns against potential losses. Simply put, it tells you how much risk you are willing to take to earn 1 unit of profit. For example, if an investment has an expected return of 30% and a maximum potential loss of 10%, then the risk-reward ratio is 1:3.

The reason high returns often come with high risk is that the market reflects uncertainty through pricing. A startup company with strong prospects but not yet profitable may see its stock price double within a year, or drop to zero; whereas a mature utility company, with low price volatility and stable annual dividends, naturally has lower return potential. Smart investors do not completely avoid risk, but learn to manage it, ensuring that the potential return justifies the risk taken.

Assess Your Personal Risk Tolerance: Are You Aggressive, Balanced, or Conservative?

Before deciding on any return-enhancing strategy, evaluate yourself honestly. Your risk tolerance depends on multiple factors, including age, income stability, investment goals, and psychological resilience. Try answering the following questions:

- Investment horizon: How long do you plan to use this money? (A. 1-3 years / B. 5-10 years / C. More than 10 years)

- Reaction to losses: If your portfolio drops by 20% within a month, what would you do? (A. Panic and sell everything / B. Feel worried but continue holding / C. Treat it as a buying opportunity and increase investment)

- Financial situation: Is your income stable? Do you have sufficient emergency savings? (A. Not very stable / B. Stable / C. Very stable with substantial savings)

If most of your answers are A, you may be conservative; mostly B, you may be balanced; mostly C, you may be aggressive. Understanding your type allows you to choose the most suitable investment tools and strategies.

5 Practical Strategies to Enhance Returns (2026 Edition)

With the theory covered, it is time to move into practice. The following five strategies have been validated over time and can effectively help you gradually improve investment returns under controllable risk.

Strategy 1: Smart Asset Allocation and Diversification

“Do not put all your eggs in one basket”. This old saying is the core of global asset allocation. Smart asset allocation refers to distributing funds across different types, regions, and industries of assets, such as stocks, bonds, real estate, and cash. The advantage is that when one type of asset performs poorly, the strong performance of others can offset part of the loss, reducing overall portfolio volatility and achieving smoother growth.

A typical balanced investor’s asset allocation may be as follows:

- 50% global equities (covering different markets such as the US, Europe, and Asia)

- 30% various bonds (government bonds, investment-grade corporate bonds)

- 10% real estate investment trusts (REITs)

- 10% cash or money market funds

Strategy 2: Use Dollar-Cost Averaging to Reduce Volatility

Trying to “buy low and sell high” by timing the market is nearly impossible for most people. Dollar-cost averaging (DCA) is a smarter and more effortless approach. It means consistently investing a fixed amount at regular intervals regardless of market movements. The core advantages of this strategy are:

- Cost averaging: When prices are high, you buy fewer units; when prices are low, you buy more units. Over time, your average purchase cost is effectively reduced.

- Emotional control: DCA is a disciplined investment approach that helps you avoid impulsive decisions driven by market fear or greed.

For investors aiming for long-term investment in index funds or large blue-chip stocks, dollar-cost averaging is an excellent tool for wealth accumulation.

Further Reading (Highly Recommended)

[2026 US High-Dividend Stock Recommendations] Top 10 High-Dividend Stock Portfolio

Strategy 3: Build Stable Cash Flow Through High-Dividend Stocks and Bonds

Do you want your portfolio not only to achieve capital appreciation but also to generate regular cash flow like rental income? Then you should focus on high-dividend stocks and bonds. These assets provide stable dividend or interest income, adding a layer of defense to your portfolio. During market volatility, this cash flow offers psychological comfort and can be reinvested to further benefit from the compounding effect. This is also an effective strategy to enhance returns, especially for investors seeking stable income. For more details, refer to the complete guide on US high-dividend stock portfolios.

Strategy 4: Regularly Review and Rebalance Your Portfolio

Investing is not a one-time effort. As markets change, your carefully designed asset allocation will gradually drift. For example, if the stock market rises significantly, the proportion of stocks in your portfolio may increase from 50% to 60%. This means your portfolio’s risk exposure is increasing.

“Rebalancing” means selling part of the assets that have performed well and reallocating the funds into underperforming assets, restoring the portfolio to its original target allocation. This process may seem counterintuitive (selling what has risen more and buying what has risen less), but it effectively locks in profits and forces you to buy assets when they are relatively cheaper, forming the core of disciplined risk management.

It is recommended to review and rebalance your portfolio at least once a year.

Strategy 5: Invest for the Long Term and Embrace the Power of Compounding

Einstein once referred to compounding as the “eighth wonder of the world”. It means that your investment returns themselves generate returns, commonly known as “earning interest on interest”. Time is the best ally of compounding. In the short term, its effect may not be obvious, but over time, its power grows exponentially.