Beware of the Trap: A High Distribution Rate Does Not Necessarily Mean a High Total Return

- The trap of “distributions coming from principal”: This is the risk that requires the most caution. When a fund’s investment income is insufficient to support the high distributions it claims to offer, the fund company may distribute money from the investor’s “principal”, which is also known as “eating its own flesh”. This will cause the fund’s NAV to keep falling, and your total assets to keep shrinking.

- Eroding the compounding effect: Distributing returns means that this money cannot remain in the fund to continue compounding. For younger investors who do not need cash flow, choosing an “accumulation” fund that reinvests returns can provide greater long-term asset growth through the power of compounding.

Further Reading (Highly Recommended)

How Does a Fund’s Expense Ratio Erode Your Returns? Understand Management Fee Calculations and How to Choose Low-Fee Funds

The Complete Guide to Investing in US Treasuries 2025: Understand What US Government Bonds Are and How to Buy Them in One Article

Comparison of 5 Selected High-Yield Fund Recommendations for 2026

The following introduces several types of high-yield funds by way of example and provides a summary comparison table to help you understand the characteristics of different funds. Please note: The following content is for educational examples only and does not constitute any investment advice. When choosing any recommended high-yield fund, be sure to conduct your own detailed research or consult a financial advisor.

Recommendation 1: Brand A Global High-Yield Bond Fund

This type of fund mainly invests in corporate bonds with lower credit ratings (non-investment grade) on a global scale, commonly known as “junk bonds”. Because the risk of default is higher, they offer higher coupon yields as compensation for that risk. It is suitable for investors who can tolerate higher risk and seek higher cash flow.

Recommendation 2: Brand B Asian High-Dividend Equity Fund

This type of fund focuses on investing in high-quality company stocks in Asia (such as Taiwan, South Korea, and Singapore) with a stable record of paying high dividends. In addition to earning dividend income, there is also an opportunity to benefit from the capital appreciation potential brought by Asian economic growth. It is suitable for investors who are optimistic about the development of Asian markets and hope to obtain both dividends and growth.

Summary Comparison Table of Recommended High-Yield Funds

| Fund Type Examples |

Main Asset Class |

Expected Annualized Distribution Rate |

Risk Level |

Features |

| Global High-Yield Bonds |

Non-investment-grade corporate bonds |

6% – 9% |

Relatively high |

Attractive distribution rate, but sensitive to economic downturns |

| Asian High-Dividend Equities |

High-dividend equities in Asia |

4% – 6% |

Medium to high |

Combines dividend income with capital appreciation potential |

| US Multi-Income |

US equities, preferred shares, and bonds |

5% – 7% |

Moderate |

Diversified asset allocation, relatively stable |

| Emerging Market Bonds |

Government and corporate bonds in emerging markets |

5% – 8%

|

Relatively high |

High yield but significantly affected by exchange rate and political risks |

| Real Estate Investment Trust (REIT) Funds |

Globally listed REITs |

4% – 6% |

Medium to high |

Income derived from rental income, with relatively low correlation to the stock market |

How to Choose the Right High-Yield Fund for You? 4 Practical Guidelines

After understanding the basic concepts and risks, choosing a good high-yield fund becomes much clearer. Following the four guidelines below can help you make more informed decisions.

Guideline 1: Evaluate the Fund’s Total Return, Not Just the Distribution Rate

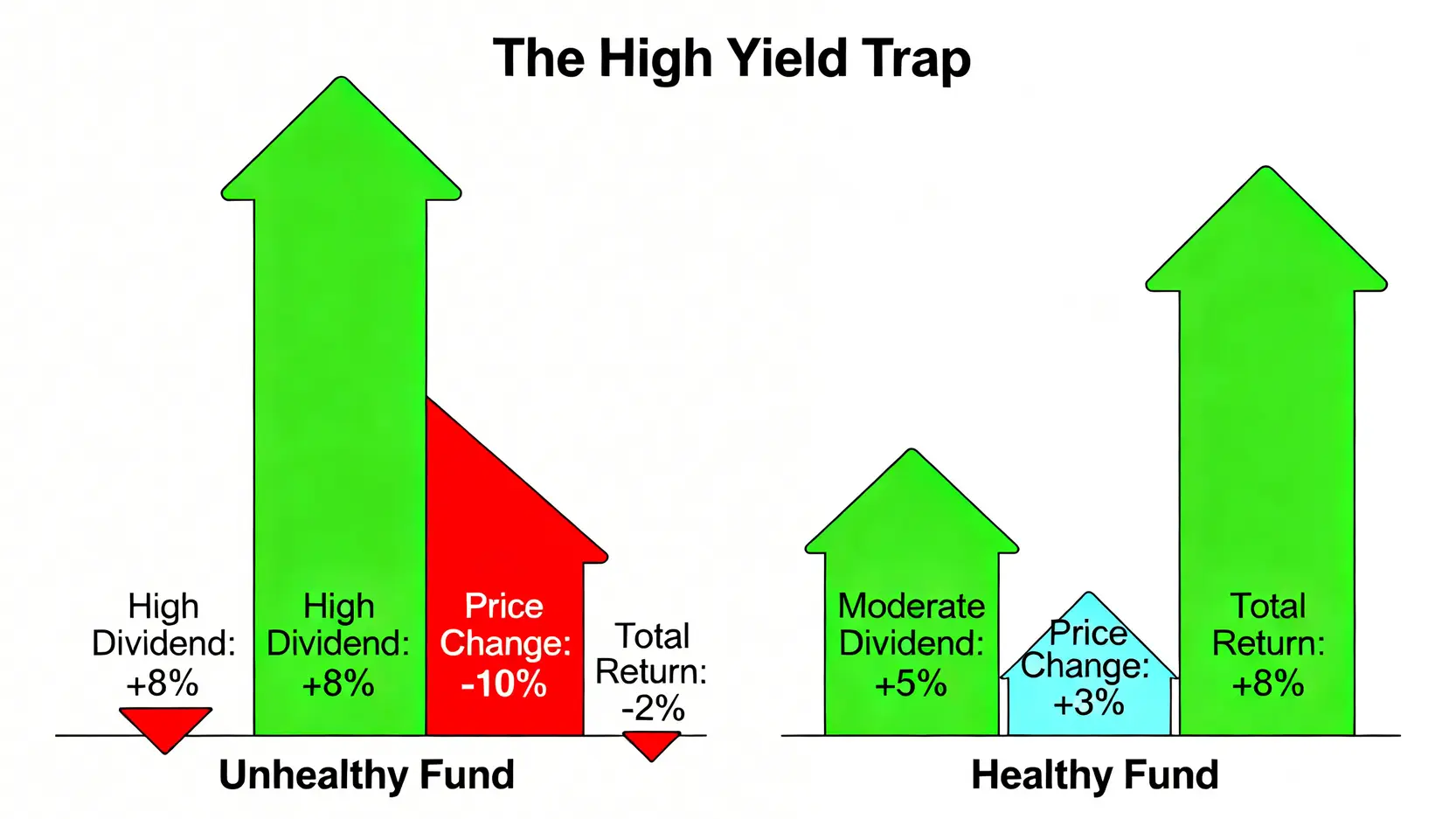

This is the most important rule. Do not be misled by high distribution rates. You need to review the fund’s long-term “total return with distributions included” performance (at least over 3 to 5 years). A healthy dividend-paying fund should have a stable or gradually increasing NAV while providing attractive distributions. You can find these historical data in the fund company’s monthly reports or financial websites. Understanding how to calculate a fund’s total return is the foundation of evaluating investment performance.

Guideline 2: Understand the Fund’s Distribution Source and Policy

In the fund’s prospectus or monthly reports, the composition of distributions is usually disclosed. Pay attention to warnings such as “distributions may come from principal”. Ideally, most distributions should come from interest and dividends generated by the portfolio. If a large portion comes from the principal, you should be highly cautious. Research reports published by authoritative institutions such as J.P. Morgan Asset Management often analyze the stability of distributions across different funds.

Guideline 3: Review the Fund’s Portfolio and Risk Rating

Take a closer look at what the fund actually invests in. Check its top ten holdings or bond positions and analyze whether its exposure to specific industries or countries is overly concentrated. At the same time, refer to risk ratings provided by independent agencies such as Morningstar to ensure the risk level is within your tolerance.

Guideline 4: Compare Related Fees and Expenses

Fund fees directly erode your returns. Major costs include management fees, subscription fees, and redemption fees, which are combined into the “Total Expense Ratio (TER)”. Between two funds with similar characteristics, choosing the one with a lower TER can save significant costs over time and directly improve your net return.

Further Reading (Highly Recommended)

[2026 US High-Dividend Stock Recommendations] Selected Portfolio of 10 High-Yield Stocks, Must-See Dividend Schedules for Beginners…

[CFD Tutorial] The Ultimate Beginner’s Guide to Contracts for Difference: From Account Opening to 5 Practical Investment Strategies

Frequently Asked Questions (FAQ)

Q: Where does the income of a dividend-paying fund come from?

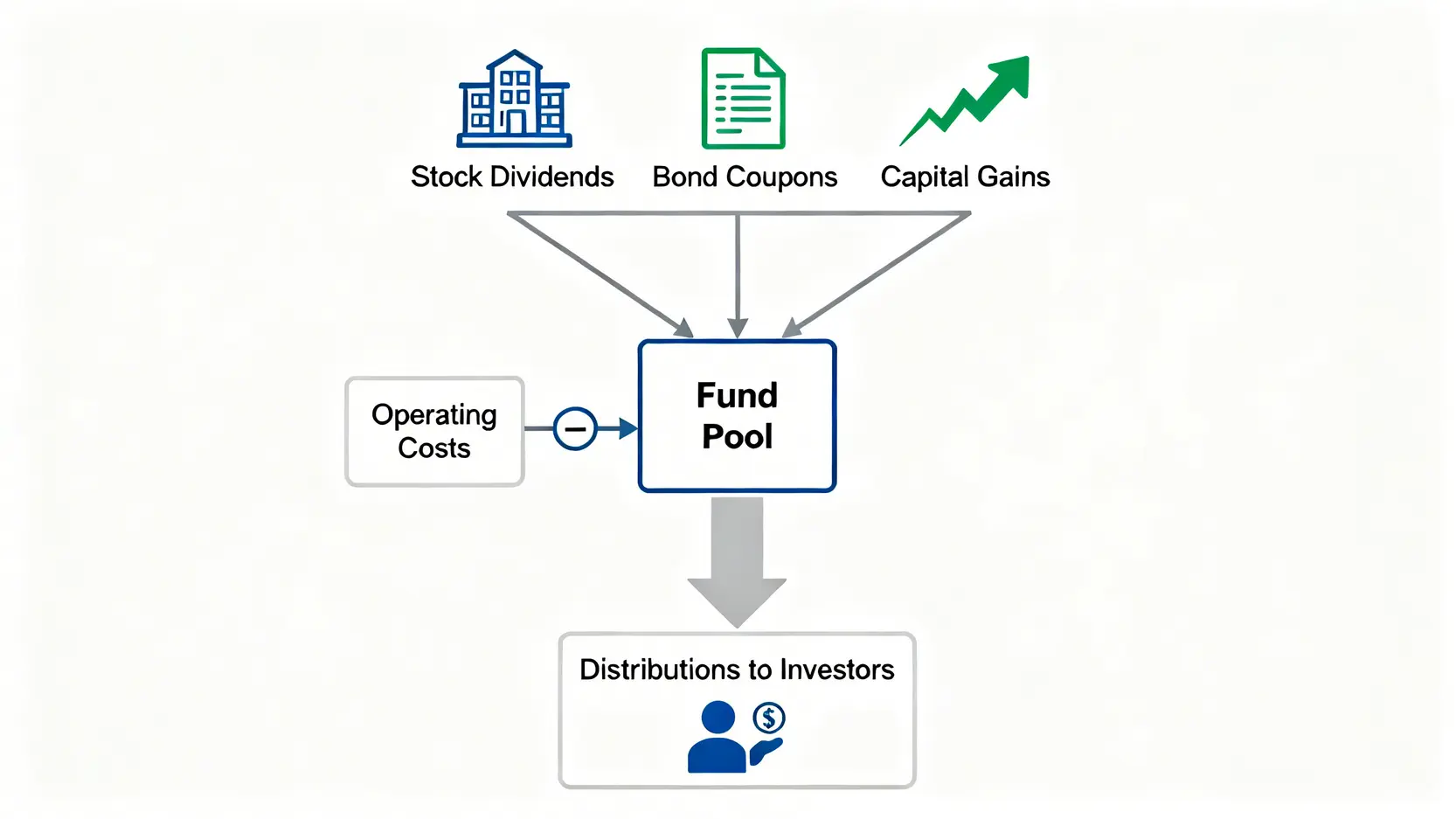

A: It mainly comes from three sources: (1) dividends paid by stocks held by the fund; (2) coupon interest paid by bonds held by the fund; (3) realized capital gains earned by the fund manager through buying and selling assets. After deducting operating expenses, these returns are distributed to investors.

Q: Is a higher distribution rate always better?

A: Absolutely not. Extremely high distribution rates are often accompanied by high risks, or may be achieved by distributing principal. Investors should focus on “total return” (which includes distributions and changes in NAV), rather than relying solely on the distribution rate. A healthy fund should provide stable distributions while maintaining or increasing its NAV.

Q: Can investing in dividend-paying funds result in loss of principal?

A: Yes. All investments carry risk. If the prices of the stocks or bonds held by the fund decline significantly, the fund’s overall NAV may fall even if you receive distributions, resulting in a loss of total assets. In addition, if distributions include principal, it is essentially eroding your capital.

Q: Should I choose monthly, quarterly, or annual distribution funds?

A: This depends entirely on your personal needs. If you require frequent cash flow to cover living expenses, monthly distribution funds may suit you better. If you do not have immediate cash needs, choosing quarterly or annual distributions, or even an “accumulation” fund that does not distribute income, allows returns to remain invested and benefit from stronger compounding effects.

Conclusion

In summary, dividend-paying funds are an effective tool for generating passive income. Monthly dividend funds, in particular, can provide stable cash flow and are highly valuable for investors with specific income needs. However, among numerous high-yield fund recommendations, investors must thoroughly understand “what is a dividend-paying fund” and carefully assess the potential risks, especially the two core concepts that “high yield does not equal high return” and “distributions may come from principal”. When making a selection, do not be attracted solely by high distribution rates, but instead focus comprehensively on long-term total return, fee structure, and portfolio stability. By following the four guidelines provided in this article, you can navigate through the wide range of options, find the dividend-paying fund that best suits your financial goals, and make more informed investment decisions.