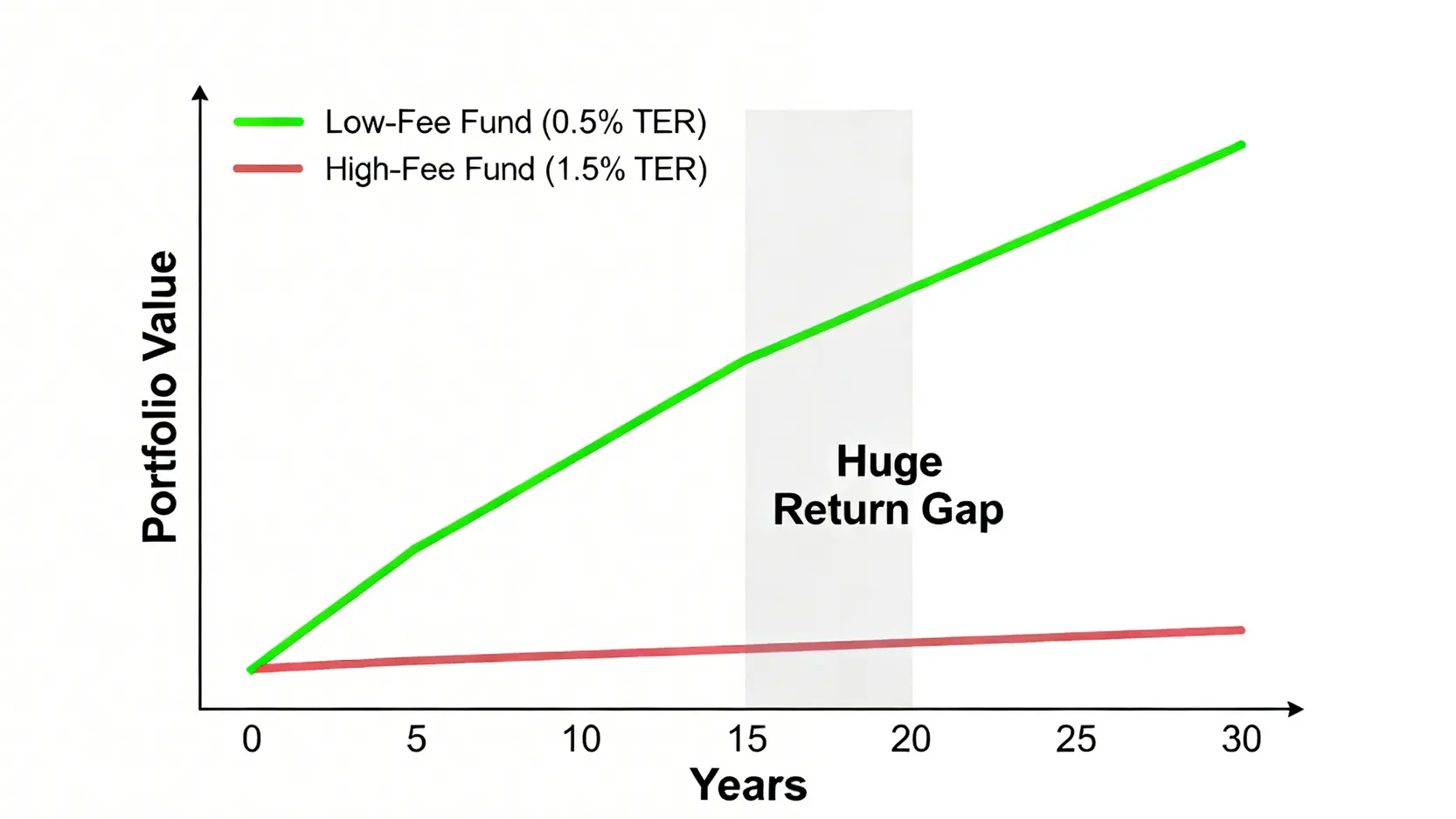

A 1% annual fee difference, under the compounding effect over 30 years, is enough to create a return gap of over one million.

With just a 1% difference in annual fees, after 30 years, Xiao Hua’s portfolio ends up with more than HKD 1 million less than Xiao Ming’s. This substantial amount is enough to impact the quality of an entire retirement. This is the most real and harsh effect of costs on long-term investing. Controlling costs directly improves your net returns.

Further Reading (Highly Recommended)

Are Funds Risky? A Complete Guide to Understanding Fund Risk and Return Analysis and RR1–RR5 Ratings

Three Practical Strategies to Easily Identify High-Quality Low-Cost Funds

Now that you understand the importance of controlling fees, the next step is to take action. With a wide array of fund products available in the market, how can you efficiently find low-cost funds that are reasonably priced and high quality? Here are three practical strategies to help you easily complete your selection.

Strategy 1: Actively Managed Funds vs Passive Index Funds (ETFs), Which Is More Cost-Effective?

Fund investments can be broadly divided into two categories: active and passive, with vastly different cost structures.

- Actively Managed Funds: Managed by fund managers and their teams who actively research and select stocks in an attempt to outperform the market. Due to high research and labor costs, their TER is typically higher, usually ranging from 1.5% to 2.5% or more.

- Passive Index Funds / ETFs: Instead of trying to beat the market, they aim to replicate the performance of a specific index (such as the Hang Seng Index or the S&P 500). Because the process is relatively simple and follows index components, management costs are very low. Many ETFs have TERs below 0.5%, with some as low as 0.1%.

Extensive academic research and market data show that, over the long term, most actively managed funds fail to consistently outperform their passive counterparts after accounting for higher fees. For most retail investors, choosing low-cost passive index funds or ETFs is the most reliable core strategy for controlling costs and achieving market-average returns.

Strategy 2: Use the MPFA “Low-Fee Fund List” and Online Comparison Tools

Finding low-cost funds does not have to be difficult. Regulators and financial websites provide useful tools to help investors compare and screen funds.

- Mandatory Provident Fund Schemes Authority (MPFA): For Hong Kong workers, MPF is a key retirement savings tool. The MPFA website provides a “Low-Fee Fund List” that clearly identifies funds with lower costs across MPF schemes, making it a great starting point to review your portfolio.

- Fund Comparison Websites: Professional financial platforms (such as Morningstar and Bloomberg) offer powerful screening tools. You can filter by criteria such as “fund category”, “TER below 1%”, or “five-year performance” to quickly narrow down suitable options.

Strategy 3: Learn to Read Fund Factsheets to Identify Key Cost Data

A “fund factsheet”, also called a “fund prospectus” is an official document that every fund must regularly publish. It serves as the fund’s “ID card” and contains all the key information you need to know, especially the details about fees.

When reviewing a factsheet, focus on:

- Fees & Charges: Lists all costs, including initial charges, redemption fees, switching fees, and most importantly, the Total Expense Ratio (TER).

- Fund Information: Includes inception date and assets under management (AUM). Larger and more established funds often have better efficiency and more competitive costs.

- Portfolio: Review the top holdings to understand whether the investment style aligns with your expectations and whether “the fees are justified”.You may refer to how to read fund reports to learn how to analyze fund prospects.

Developing a habit of regularly reviewing fund factsheets ensures you fully understand your cost structure and avoid unknowingly paying excessive “hidden fees”.

Conclusion

In summary, to maximize long-term investment outcomes, controlling investment costs is just as important as pursuing market returns, if not more critical. Gaining a deep understanding of the compounding impact of the fund expense ratio, mastering how fund management fees are calculated, and applying practical strategies for selecting low-cost funds are key steps in transitioning from an average investor to a sophisticated one. Take action now to review your investment portfolio and MPF account, ensuring every dollar is working efficiently for your financial future rather than quietly flowing into fund companies’ pockets. Smart choices can significantly and positively reshape your long-term wealth trajectory.

FAQ

Q: Does a higher fund expense ratio mean better fund performance?

A: This is a common misconception. A higher expense ratio often indicates an “actively managed fund”, where managers invest more resources in research and analysis to generate excess returns. However, extensive data shows no necessary positive correlation between higher fees and better performance. In many cases, high fees become a drag on long-term returns. When selecting funds, a high TER should not be seen as a sign of quality, but rather as a higher hurdle the fund must overcome.

Q: Besides the expense ratio, what other hidden costs should I watch out for when investing in funds?

A: In addition to operating expenses included in TER, investors may face “transaction costs” that are not reflected in TER. These mainly include:

- Subscription Fee: A one-time fee paid when purchasing the fund, usually a percentage of the investment amount.

- Redemption Fee: A fee charged when selling the fund, sometimes applied to discourage short-term withdrawals.

- Switching Fee: A fee incurred when switching between funds within the same fund company.

- Bid-Ask Spread: The small difference between buying and selling prices, which can accumulate with frequent trading.

Before investing, always read the fund’s offering documents carefully to understand all potential charges.

Q: How should I compare fund fees across different countries or regions?

A: Fee levels vary across markets due to differences in regulatory environments, competition, and investor behavior. For example, US index funds and ETFs are highly competitive and generally have the lowest fees globally. When comparing, follow the principle of comparing similar categories (such as global large-cap equity funds). Also consider currency and tax differences. Using international fund rating platforms (like Morningstar) allows you to compare funds across regions on a consistent basis.

Q: Can MPF fund fees be negotiated?

A: Individual employees usually cannot negotiate management fees directly with MPF trustees. However, through the “employee choice arrangement” (often referred to as the “MPF semi‑DIY”), you can transfer your own contributions to lower‑fee funds within the same plan or to another plan. Therefore, actively comparing fees and performance across different MPF schemes and making use of your transfer rights is an effective way to indirectly “reduce” costs. Regularly reviewing the list of low‑fee funds published by the MPF Authority is an important step in making informed decisions.