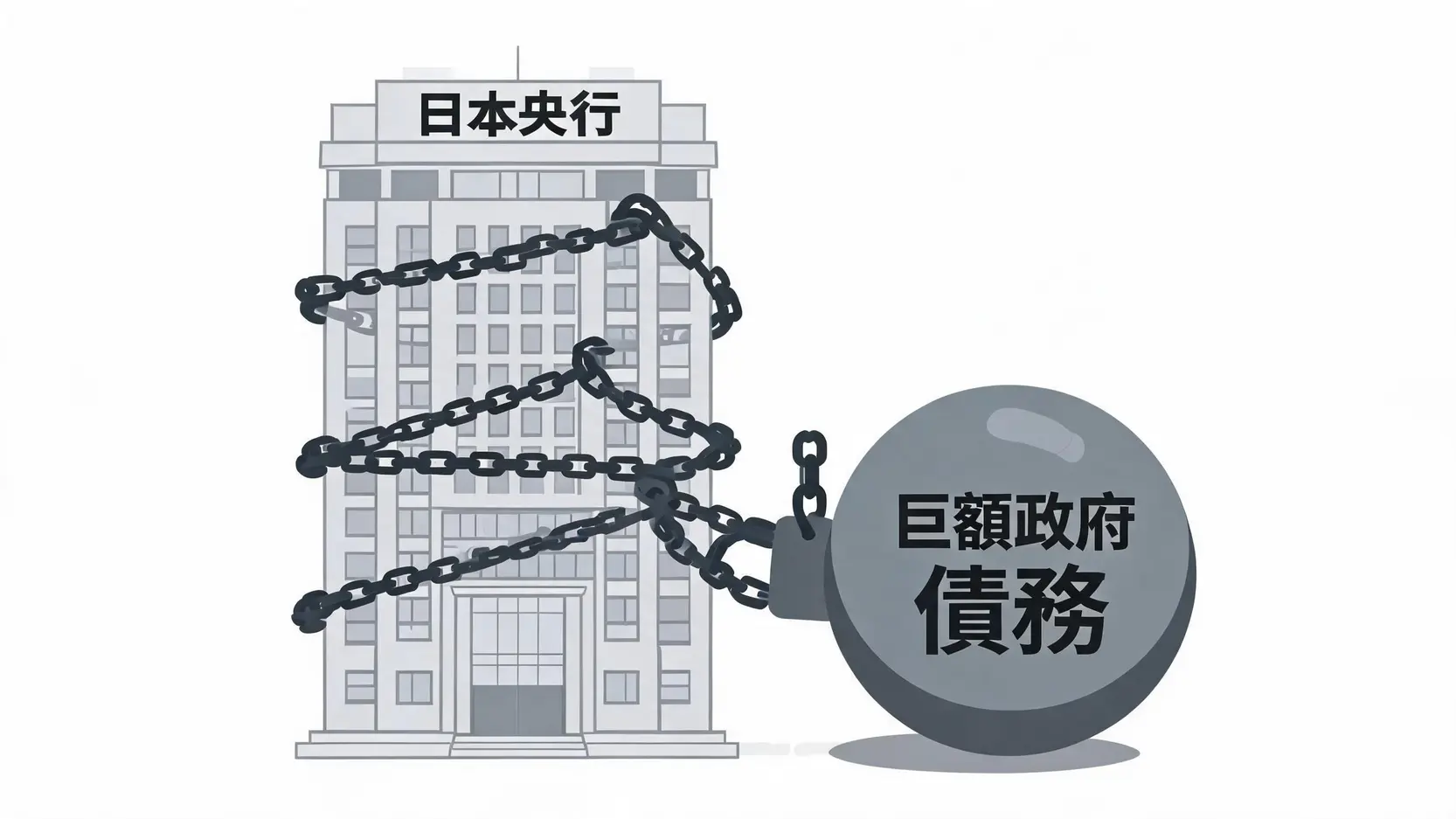

The Bank of Japan Remains Tightly Constrained by the “Shackles” of Massive Government Debt

Shackle Two: The Survival of Zombie Companies and Their Dependence on Cheap Credit

Decades of ultra-low interest rates have allowed the emergence of large numbers of so-called “Zombie Companies” in Japan. These firms are often inefficient and uncompetitive and would normally struggle to survive in a competitive market. However, because borrowing costs remain exceptionally low, they can continue operating by rolling over cheap loans. If the Bank of Japan were to raise rates significantly, financing costs for these companies would surge. Many could face liquidity crises, triggering widespread bankruptcies and rising unemployment. Such an outcome could threaten both financial stability and social stability. To avoid a hard landing, policymakers often prefer maintaining accommodative conditions and allowing these companies to continue operating.

Shackle Three: The Deflation Ghost Still Lingers, and Confidence in Sustainable Inflation Remains Weak

Although Japan’s inflation rate has recently risen and even exceeded the 2% target, the Bank of Japan remains unconvinced. Policymakers believe that much of the recent inflation has been driven by higher import costs for energy and raw materials, representing “cost-push inflation” rather than “demand-pull inflation” generated by strong domestic demand and sustained wage growth.

After decades of deflation, Japanese households and businesses have developed deeply ingrained deflationary expectations. Consumers remain cautious about spending, while companies are reluctant to raise prices and wages. Without clear evidence that wage growth and inflation are reinforcing one another in a healthy cycle, the Bank of Japan fears that raising rates could quickly push the economy back into deflation. This lack of confidence continues to slow the path toward monetary policy normalization.

Further Reading (Highly Recommended)

A Complete Analysis of USD/JPY Trends: Investment Opportunities Amid Expectations of Federal Reserve Rate Cuts

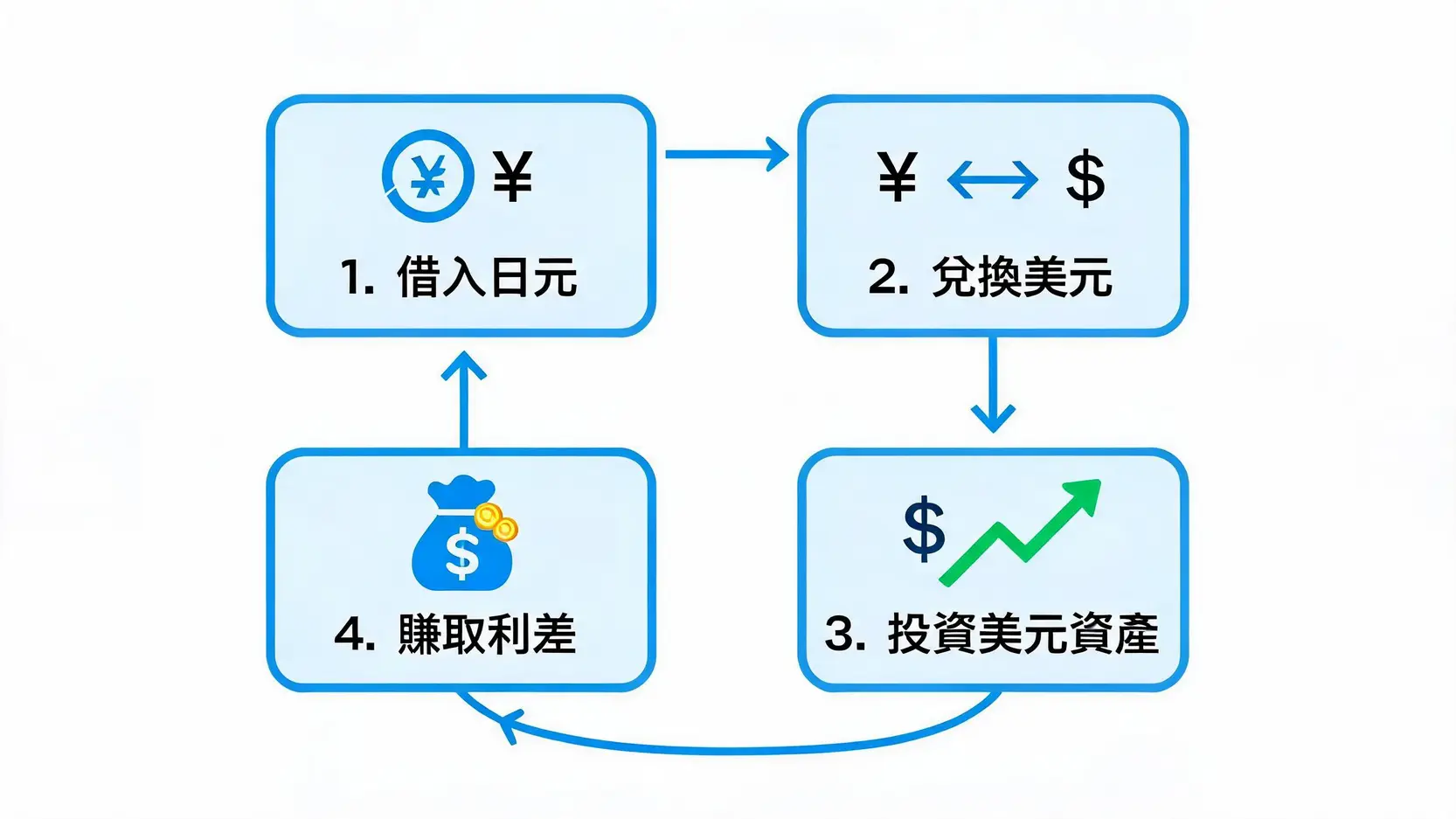

Yen Leverage Blow-Up Case Study: Understanding Interest Rate Differential Trading Risks Through the Mrs. Watanabe Tragedy

The Path Forward: Possible Ways to Break the Deadlock

Faced with mounting internal and external challenges, the yen will require a combination of domestic and international factors to truly escape its depreciation cycle. Market participants generally believe that the most likely paths to breaking the current deadlock come from two directions.

External Variable: Waiting for a Federal Reserve Policy Shift (Rate Cuts)

This is the most direct, yet also the most passive, solution. If US inflation comes under control and economic growth begins to slow, the Federal Reserve may initiate a rate-cutting cycle. Once the Fed starts lowering interest rates, the attractiveness of the US dollar would diminish, and the US-Japan interest rate differential would naturally narrow. This would significantly ease depreciation pressure on the yen and could even trigger large-scale carry trade unwinding, potentially driving a rapid appreciation of the Japanese currency. As a result, global markets closely monitor every piece of economic data and every statement from the Federal Reserve, searching for signs of a policy shift. In many respects, the fate of the yen remains heavily influenced by the decisions of the Federal Reserve.

Internal Reform: The Necessity and Challenges of Structural Economic Reform in Japan

Fundamentally, if Japan wishes to reduce its dependence on ultra-loose monetary policy, it must pursue meaningful structural economic reforms. These include:

- Improving labor productivity: Enhancing corporate profitability through technological innovation and deregulation.

- Promoting wage growth: Reforming the labor market and encouraging businesses to translate profits into higher wages, thereby supporting domestic demand.

- Addressing population aging: Implementing more effective policies to cope with labor shortages and the growing burden of social welfare costs.

However, these structural reforms are far easier to propose than to implement. They often involve challenging vested interests and require substantial political determination and broad social consensus. Such changes cannot be achieved overnight. Nevertheless, they represent the most effective long-term solution for restoring Japan’s organic growth potential and permanently escaping the shadow of deflation.

FAQ

Q: What are Quantitative Easing (QE) and Yield Curve Control (YCC)?

A: Quantitative Easing (QE) and Yield Curve Control (YCC) are both unconventional monetary policy tools. Quantitative Easing refers to a central bank purchasing large quantities of government bonds and other assets in the open market to inject liquidity into the financial system and lower long-term interest rates. Yield Curve Control goes a step further by directly setting a target yield level for long-term government bonds (such as the 10-year Japanese government bond) and committing to unlimited bond purchases to ensure yields do not rise above that target. Both policies have been central tools used by the Bank of Japan to combat deflation and maintain an extremely accommodative financial environment.

Q: What impact would a Bank of Japan rate hike have on the Japanese economy?

A: It would be a double-edged sword. On the positive side, higher interest rates could narrow the US-Japan interest rate differential, support the yen, and reduce imported inflation. However, the negative consequences could be substantial. First, the government’s enormous debt-servicing costs would rise sharply, increasing concerns about fiscal sustainability. Second, borrowing costs for businesses (particularly zombie companies) and households would increase, potentially reducing investment and consumption and even triggering a wave of bankruptcies. Finally, asset prices, including real estate and equities, could come under pressure as liquidity tightens. Overall, given the fragility of the current economy, the short-term pain of rate hikes may outweigh the benefits.

Q: Besides the US-Japan interest rate differential, what other factors influence the yen?

A: Although the US-Japan interest rate differential is the dominant driver, several other factors also matter. 1. Risk sentiment: During financial crises or periods of geopolitical uncertainty, the yen is often viewed as a “safe-haven currency” due to Japan’s low interest rates and stable financial system, attracting capital inflows and supporting appreciation. 2. Trade balance: Japan’s import and export performance also affects the exchange rate. Persistent trade surpluses tend to support the yen, while deficits create depreciation pressure. In recent years, high energy prices have contributed to larger trade deficits and have been one factor behind yen weakness. 3. Market sentiment and speculative activity: In the short term, positioning changes by large hedge funds and shifts in expectations regarding central bank policy can generate significant exchange rate volatility.

Q: What opportunities and risks does yen depreciation create for ordinary investors?

A: Yen depreciation creates both opportunities and risks. On the opportunity side, it lowers costs for those planning to travel to Japan or purchase Japanese goods. It may also benefit foreign investors in the Japanese stock market (such as those investing in the Nikkei 225 Index), as weaker yen levels can improve the earnings of Japanese exporters and support equity prices. On the risk side, individuals holding yen-denominated assets or earning income in yen may see the global purchasing power of those assets decline. In addition, anyone trading yen-related foreign exchange products should be mindful of the risk of sudden Bank of Japan intervention or sharp market reversals driven by changes in global sentiment.

Conclusion

In summary, foreign exchange intervention by Japan’s Ministry of Finance is ultimately a short-term measure that treats the symptoms rather than the underlying problem. If the yen is to genuinely escape its depreciation cycle, the fundamental solution lies in a meaningful narrowing of the US-Japan interest rate differential. This largely depends on two key factors: externally, when the Federal Reserve begins cutting interest rates, and internally, whether the Bank of Japan can gradually free itself from its policy constraints without triggering a domestic fiscal or economic crisis, while simultaneously pursuing effective structural economic reforms. Until then, yen volatility driven by interest rate differentials is likely to remain a defining feature of global financial markets, and investors should approach this reality with clear understanding and adequate preparation.