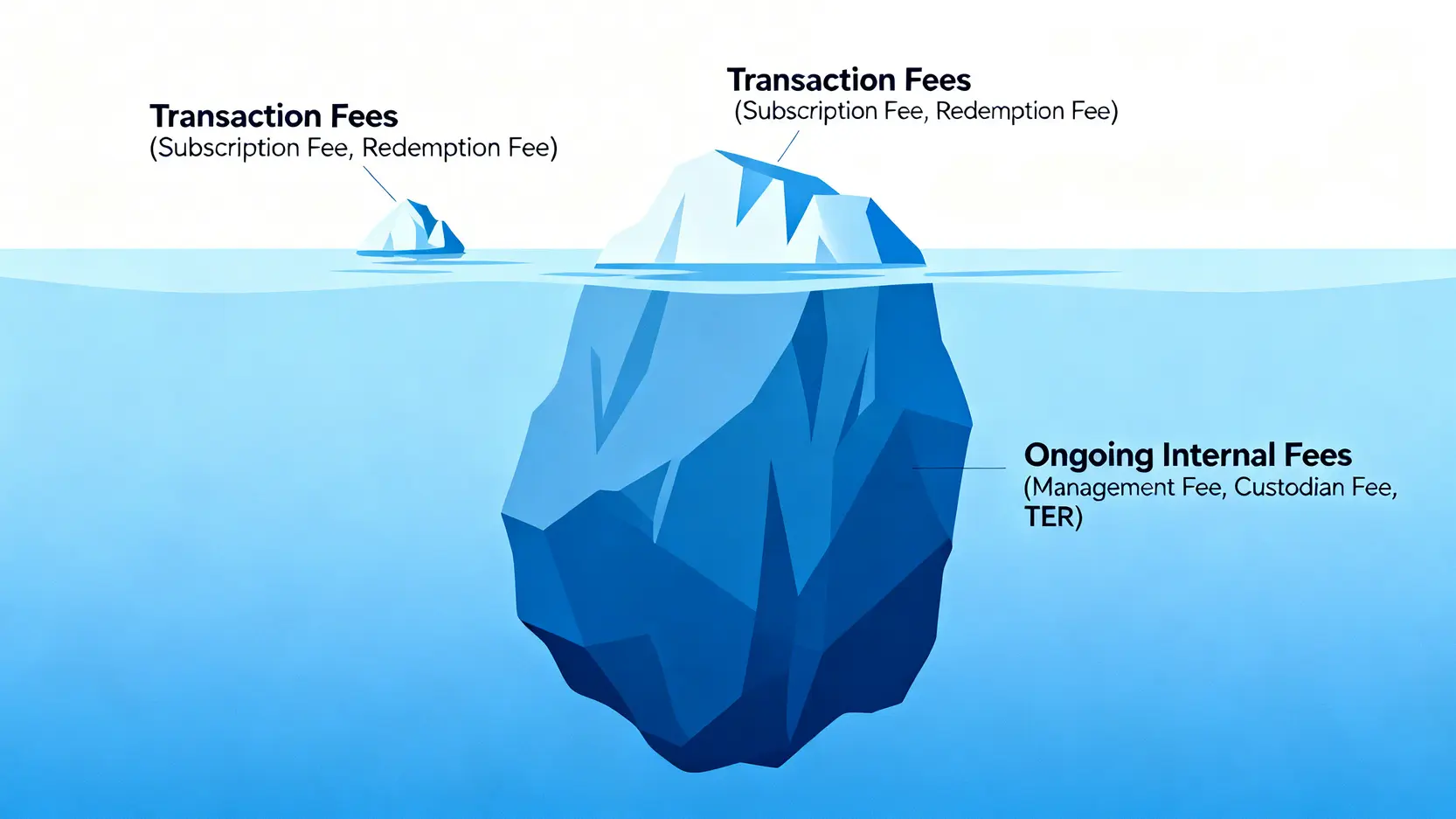

Fund fees are like an iceberg. Transaction fees are only the tip, while ongoing expenses are the main factor that erodes returns.

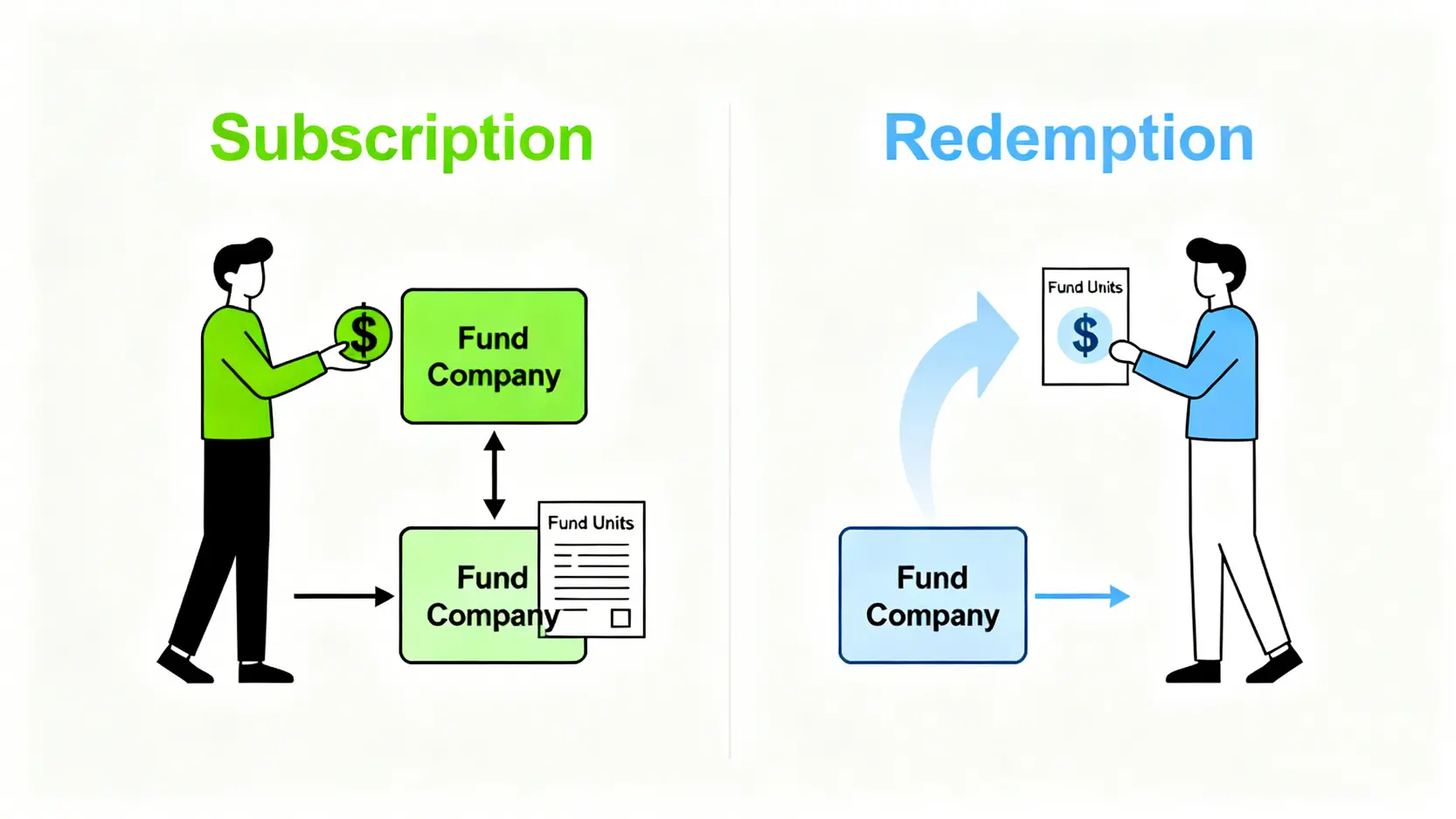

Transaction Fees: Subscription Fee, Redemption Fee, Switching Fee

These are one-time charges incurred when you buy, sell, or switch funds.

- Subscription Fee: This is the most common fee, charged as a percentage of the subscription amount when you purchase a fund. The rate varies depending on the fund type and sales channel, usually ranging from 1% to 5%. Online fund platforms often offer discounts or even waive this fee.

- Redemption Fee: Some funds charge a fee for redemption within a short holding period, (such as within one year) to encourage long-term holding. This fee is usually returned to the fund assets to compensate other long-term holders.

- Switching Fee: When you transfer funds from Fund A to Fund B within the same fund company, a switching fee may be charged, which is usually lower than the subscription fee.

Ongoing Expenses: Management Fee, Custodian Fee

These fees are not directly charged to you but are deducted daily from the fund’s NAV, making them easier to overlook.

- Management Fee: Paid to the fund company and managers as compensation for managing the fund’s assets. This is the main ongoing expense, usually charged at 0.5% to 2% of assets annually.

- Custodian Fee: Paid to the third-party financial institution (usually a bank), responsible for safeguarding the fund’s assets to ensure security and independence.

- Other Operating Expenses: Include administrative, legal, and accounting costs.

All ongoing expenses are combined into a ratio called the “Total Expense Ratio” (TER). This represents the total annual operating cost of the fund as a percentage of its assets and is an important metric for comparing the actual cost of different funds. You can find this information in the fund’s prospectus or monthly reports.

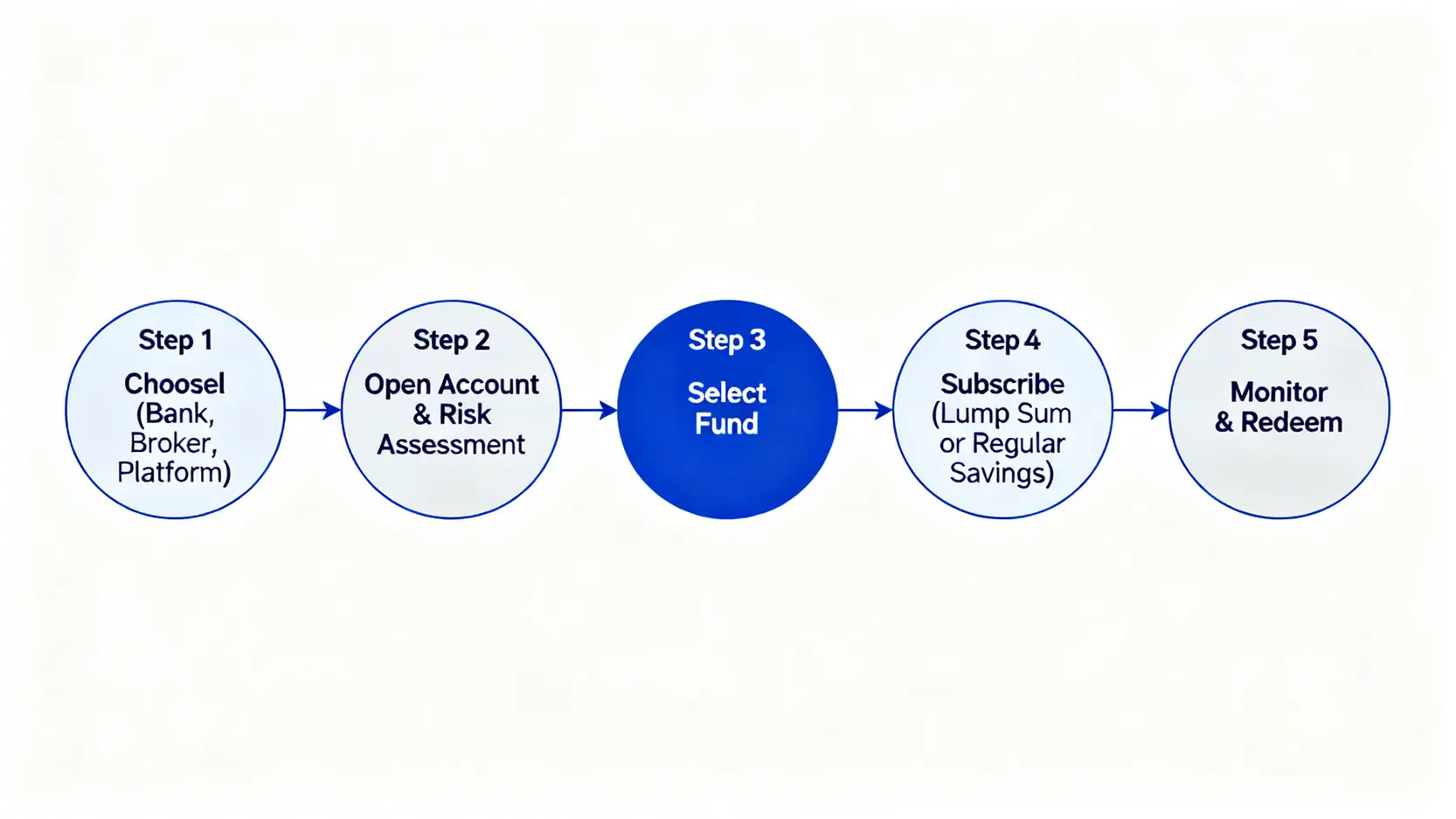

How to Compare Total Costs Across Different Platforms? Practical Tips to Save Money

To reduce the cost of fund investing, you can focus on the following:

- Prioritize Online Fund Platforms: They offer the most discounts on subscription fees, sometimes even zero fees, saving a significant upfront cost.

- Compare Total Expense Ratio (TER): When deciding between two similar funds, choose the one with a lower TER, as the long-term compounding effect will be more significant.

- Avoid Frequent Switching: Unless there is a major change in your investment strategy, frequent switching only accumulates unnecessary switching fees.

- Pay Attention to Redemption Fee Terms: Before subscribing, understand whether the fund has redemption fees and holding period requirements to avoid penalties due to short-term liquidity needs.

Frequently Asked Questions About Fund Trading (FAQ)

Q: How long does it take for redemption proceeds to be credited?

A: This depends on the fund type and registration location. Generally, equity funds have shorter settlement periods (typically 3 to 5 working days), while funds investing in overseas markets or less liquid assets may take 7 to 10 working days or longer.

Q: What are T+1 and T+2 trading days, and how do they affect fund trading?

A: “T” represents the transaction day, which is the day you place the order. T+1 and T+2 refer to the first and second working days after the transaction day. Fund transactions use the NAV calculated after the market closes on T day as the transaction price, while settlement and unit confirmation are usually completed on T+N days. For example, T+2 settlement means the funds are credited to your bank account on the second working day after placing the order.

Q: Can I cancel a regular investment plan or redeem funds at any time?

A: Yes, most funds allow investors to pause or terminate a regular investment plan at any time and to submit redemption requests at any time, offering high liquidity. However, changes or cancellations usually require several working days in advance to take effect before the next deduction date. When redeeming, you should also consider the settlement time and whether short-term redemption fees apply.

Q: Do I need to pay taxes when buying and selling funds?

A: This depends on your tax jurisdiction. In Taiwan, capital gains from fund trading are currently tax-free, but if the fund’s income includes domestic dividends or interest, it will be included in personal income tax or subject to separate taxation. In Malaysia, capital gains from funds for local residents are generally also tax-free. It is recommended to consult a local tax professional for the most accurate information.

Conclusion

In summary, mastering a clear fund trading process, understanding fund subscription and redemption mechanisms, and carefully evaluating all fund fees are the foundation of successful investing. Although the process may seem complex, by following the steps in this guide, from choosing the right channel and opening an account to selecting funds and executing transactions, you can get started with ease. Most importantly, take the first step and continue learning along the way. Start comparing different investment platforms now, choose the plan that suits you best, and implement your financial plan!