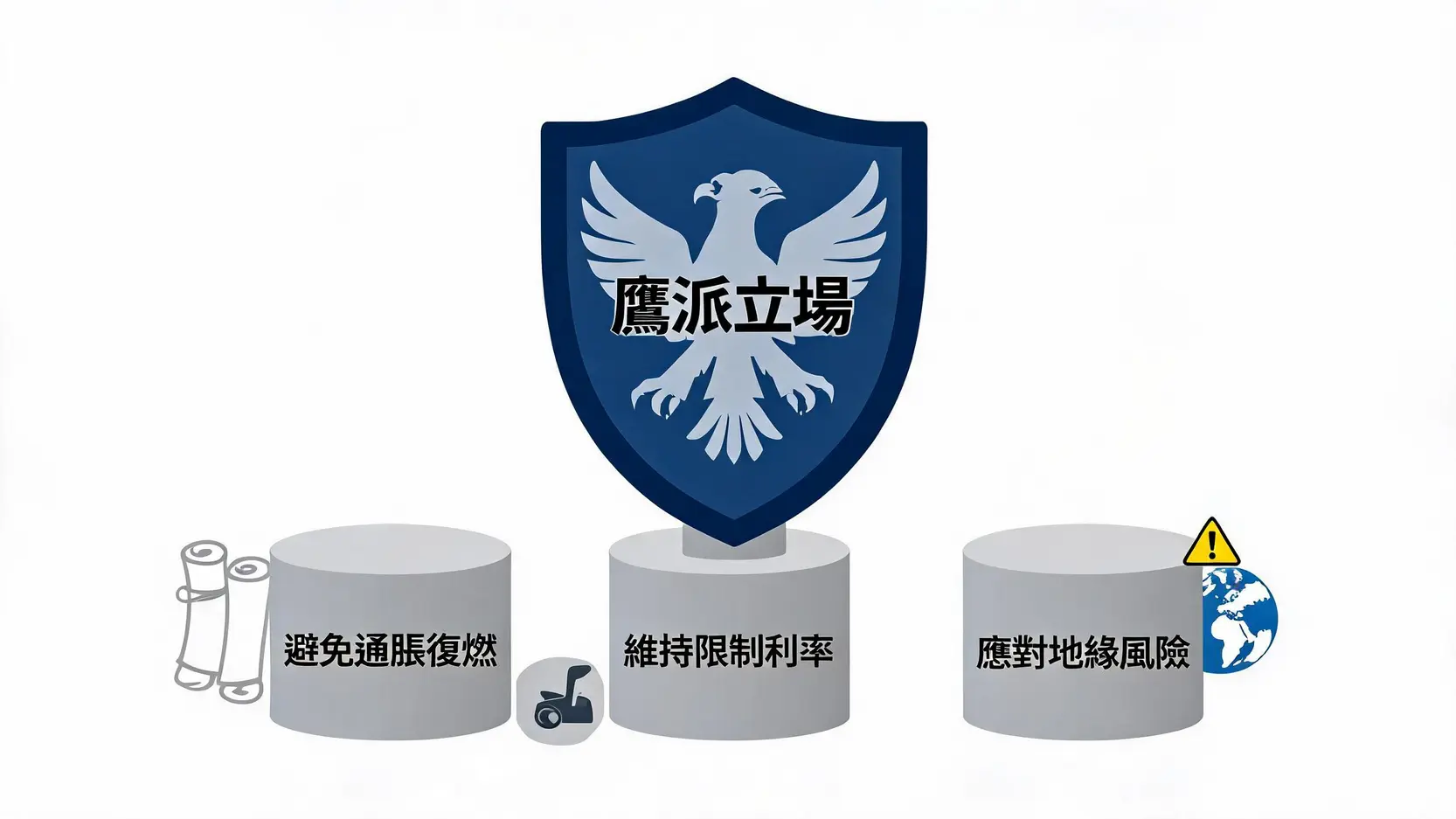

The Three Core Reasons Behind the Federal Reserve’s Hawkish Stance

Further Reading (Highly Recommended)

Your Money Is Losing Value! Understanding How Inflation Affects the Purchasing Power of the Taiwan Dollar and Wealth Preservation in One Article

[2026 Beginner’s Guide to US Stocks] The Ultimate Guide to Investing in US Stocks for Beginners: Everything You Need to Know About Opening an Account

How to Understand the Federal Reserve’s Next Move Through the “Dot Plot” and Officials’ Remarks

In such a complex macroeconomic environment, investors are eager to find clues about the Federal Reserve’s next move. Among the most important indicators are the Federal Reserve’s “dot plot” and public remarks made by its officials.

Interpreting the Dot Plot: Understanding Committee Members’ Interest Rate Expectations

The dot plot is a chart released quarterly by the Federal Reserve that anonymously displays each Federal Open Market Committee (FOMC) member’s projections for the policy interest rate over the coming years. Although it is not an official policy commitment, it provides an excellent window into policymakers’ thinking.

- Watch for changes in the median: The median dot (representing the midpoint of all projections) receives the most market attention. If the median shifts higher in the latest dot plot, it suggests the Federal Reserve’s overall interest rate outlook has become more hawkish, signaling fewer rate cuts or later timing.

- Analyze the distribution: Observe whether the dots are tightly clustered or widely dispersed. A wide dispersion indicates significant disagreement within the committee, while a tighter cluster suggests stronger consensus and greater certainty regarding the policy path.

- Pay attention to the long-term rate projection: The long-term rate projection reflects committee members’ views on the “neutral rate”. If this projection moves higher, it may indicate that the Federal Reserve believes the economy can sustain higher interest rates over the long run.

Analyzing Officials’ Remarks: The Tug of War Between Hawks and Doves

Between each FOMC meeting, public remarks from Federal Reserve Bank presidents and Board members become the market’s focal point. Their comments often reveal their views on current economic data and their policy preferences. Investors should learn to distinguish between “hawkish” and “dovish” positions.

- Hawks: More concerned about inflation and generally favor maintaining higher interest rates or raising rates further. When hawkish voices dominate, market expectations for rate cuts typically weaken.

- Doves: More concerned about economic growth and employment and generally favor rate cuts. When dovish voices become more prominent, expectations for rate cuts tend to strengthen.

By following the remarks of these officials (including key figures such as Chair Jerome Powell and New York Fed President John Williams) while also considering the latest economic data, investors can more accurately gauge shifts in the Federal Reserve’s internal thinking and form more reasonable expectations about future policy changes.

Further Reading (Highly Recommended)

Long-Term Investment Strategy Guide: Short-Term Tools, Dividend Investing, and Passive Investment Allocation Strategies

[Investment Guide for Uncertain Times] Geopolitical Risks Are Rising? A Complete Comparison of the Five Major Safe-Haven Assets

Conclusion

In summary, the market’s shift from the early-year “rate cut euphoria” to today’s “reversal in interest rate expectations” does not reflect inconsistency on the part of the Federal Reserve. Rather, it reflects a major Federal Reserve pivot driven by economic realities. Persistent core inflation, an exceptionally strong labor market, and resilient consumer spending have collectively led to the failure of expected rate cuts. Driven by concerns over a resurgence in inflation, the need to maintain restrictive monetary policy, and geopolitical risks, the Federal Reserve has adopted a more cautious and hawkish stance. For investors, understanding the deeper logic behind this shift is essential. It means abandoning expectations of rapid rate cuts in the near term, reassessing asset allocation, and preparing for a new normal in which interest rates may remain higher for longer. Going forward, closely monitoring inflation and employment data while learning to interpret the dot plot and officials’ remarks will be key to navigating an increasingly uncertain market with confidence.

Frequently Asked Questions (FAQ)

Q: Why Is There a Gap Between Market Expectations and the Federal Reserve’s Projections?

A: The gap between market expectations and the Federal Reserve’s projections mainly stems from their different perspectives and approaches. Market pricing, particularly in the interest rate futures market, reflects traders’ collective “bets” on future economic data. It is heavily influenced by sentiment and short-term data, allowing it to react very quickly. In contrast, the Federal Reserve’s projections (such as the dot plot) are based on its internal economic models and the professional judgment of each committee member. They focus more on medium- to long-term trends, with a more cautious decision-making process designed to avoid overreacting to short-term market fluctuations. As a result, the Federal Reserve’s projections often appear more “lagging” or “conservative”.

Q: How Long Will Higher for Longer Last?

A: There is no definitive answer, as it depends entirely on future economic data. Federal Reserve Chair Jerome Powell has repeatedly emphasized the Fed’s “data-dependent” approach to policymaking. Generally, the Federal Reserve is expected to see several consecutive months (such as three to six months) of inflation clearly moving toward its 2% target, along with signs of moderate cooling in the labor market (such as a slight rise in the unemployment rate and slower wage growth) before seriously considering rate cuts. Until then, the high interest rate environment is likely to persist.

Q: How Will the Federal Reserve’s Policy Pivot Affect My Mortgage?

A: The Federal Reserve’s policy pivot has a direct impact on mortgage rates. When markets expect interest rates to remain higher for longer, yields on long-term government bonds typically rise, and mortgage rates are closely linked to long-term government bond yields. This means borrowers applying for fixed-rate mortgages are likely to face higher borrowing costs. For those with adjustable-rate mortgages, monthly payments are likely to remain elevated as long as the Federal Reserve does not cut interest rates.

Q: How Should I Adjust My Stock Portfolio in the Current Environment of Reversed Interest Rate Expectations?

A: A high interest rate environment affects different types of stocks in different ways. Interest rate-sensitive growth stocks, technology stocks (whose valuations rely on discounted future cash flows) and industries that depend heavily on financing (such as real estate and utilities), generally face greater pressure. In contrast, value stocks with strong cash flow and healthy balance sheets, financial stocks, especially banks that benefit from wider interest margins, and inflation-resistant sectors such as energy may perform relatively better. Investors should consider making their portfolios more defensive while placing greater emphasis on corporate fundamentals and profitability rather than growth narratives alone.

Q: Could the Federal Reserve Raise Interest Rates Again in the Future?

A: Although further rate hikes are not the base-case scenario at present, Federal Reserve officials have never completely ruled out the possibility. If inflation unexpectedly rebounds significantly or financial conditions become excessively loose, causing the economy to overheat, the Federal Reserve may be forced to raise interest rates again to preserve its credibility in fighting inflation. Therefore, although the probability remains low, investors should still factor “the risk of further rate hikes” into their considerations.