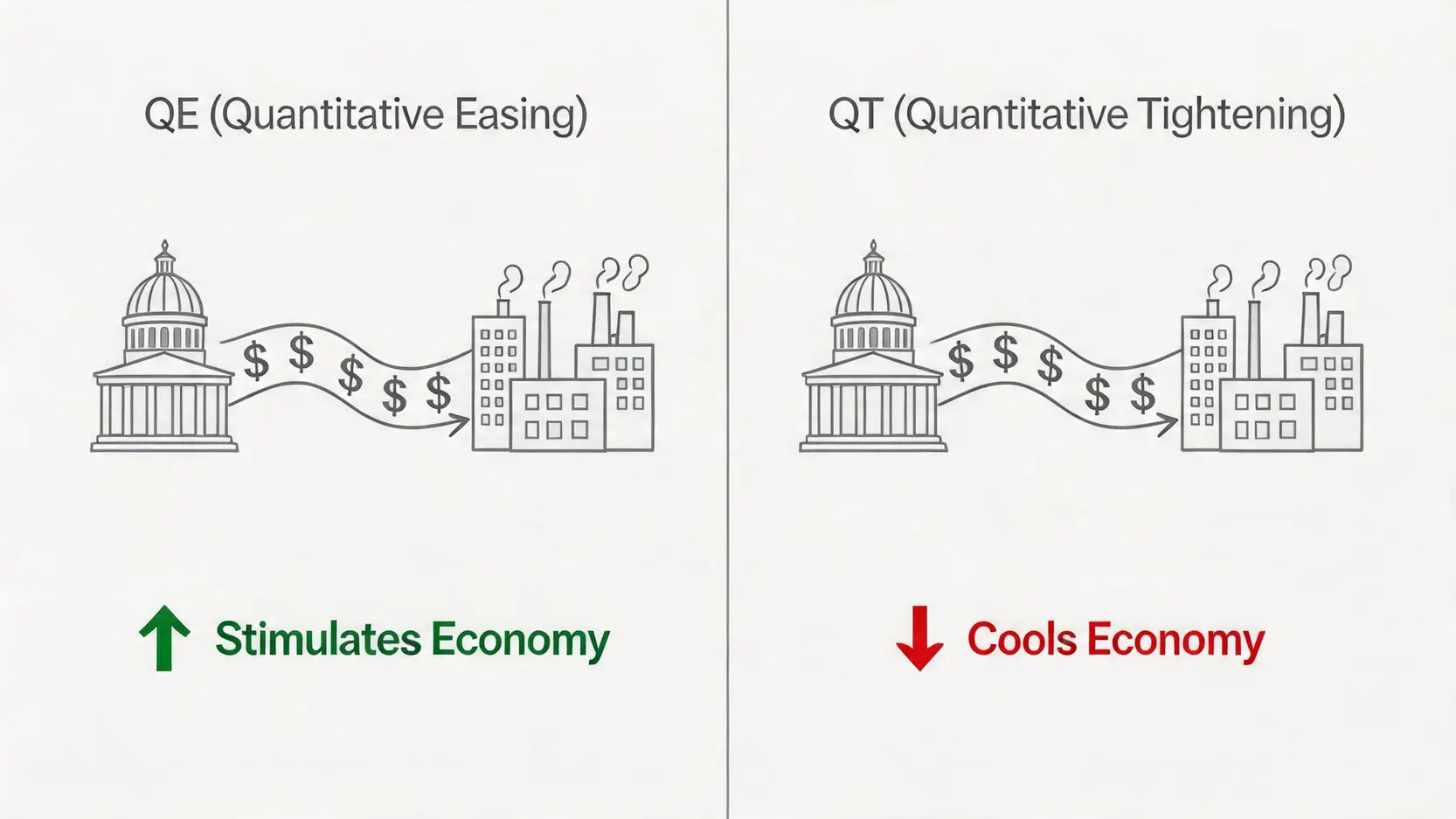

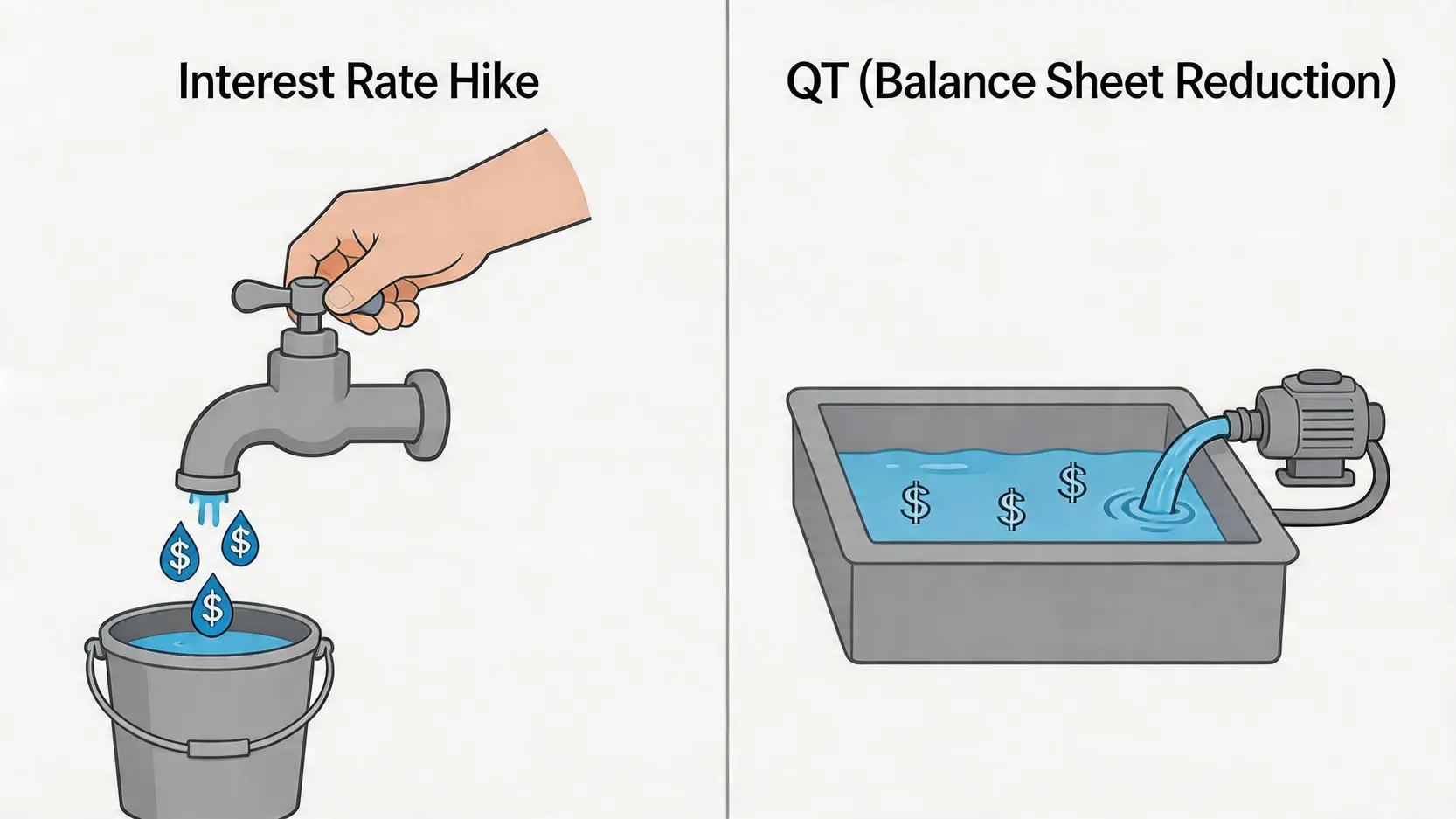

Interest rate hikes vs. balance sheet reduction: one regulates the “price of money”, while the other reduces the “quantity of money”.

In simple terms, interest rate hikes increase the cost of borrowing, while balance sheet reduction decreases the amount of money in the market. The two are often used together, forming a dual “price and volume contraction” impact, and their influence on financial markets should not be underestimated.

Five Major Core Impacts of Balance Sheet Reduction on the Stock Market

When the central bank begins “withdrawing liquidity” the stock market, as one of the most sensitive areas to capital flows, is inevitably affected. Understanding these potential impacts of balance sheet reduction on the stock market is the first step in adjusting investment strategies.

Impact 1: Reduced market liquidity leads to downward pressure on asset valuations

This is the most direct impact. With less money in the market, there is naturally less capital chasing stocks. During the QE era, abundant liquidity pushed up almost all asset prices, creating a “rising tide lifts all boats” effect. In the QT era, the opposite occurs. Asset valuations (such as P/E ratios) face downward pressure due to liquidity withdrawal. Even if corporate fundamentals do not deteriorate, stock prices may still decline.

Impact 2: Rising borrowing costs put pressure on corporate profitability

Balance sheet reduction pushes up long-term interest rates, meaning that companies, especially those reliant on debt financing for expansion, will face higher funding costs. Increased interest expenses directly erode corporate profits and weaken profitability. For highly leveraged companies, this is particularly damaging and may even trigger financial distress.

Impact 3: Greater impact on tech stocks and growth stocks

Technology stocks and startups typically derive their valuations from expectations of “strong future growth”. In financial models, future cash flows are discounted using a rate that is closely tied to long-term interest rates. When balance sheet reduction pushes long-term rates higher, the discount rate rises, and the present value of distant future earnings declines significantly, leading to sharp price corrections. This is why high-valuation tech stocks are often the hardest hit during tightening cycles.

Impact 4: Rising risk aversion among investors leads to a shift toward defensive assets

Uncertainty caused by balance sheet reduction lowers risk appetite in the market. Investors become more cautious and shift capital away from high-risk equities into safer assets, such as:

- Cash: holding cash to wait for better opportunities.

- Short-term government bonds: very low risk, and rising interest rates increase their attractiveness.

- Defensive stocks: such as utilities and consumer staples, which have relatively stable demand and are less affected by economic cycles.

Impact 5: Increased currency volatility affects import and export companies

When a country is among the first to implement balance sheet reduction and rate hikes, its currency typically appreciates due to interest rate advantages. While a stronger currency helps suppress import-driven inflation, it hurts export industries because foreign buyers need to spend more to purchase the country’s goods, reducing export competitiveness and profitability. For large export-oriented companies, this is a significant negative factor.

Further Reading (Highly Recommended)

What is QE? A Complete Guide to Quantitative Easing, Its Impact, and Investment Strategies

What Is a 25 Basis Point Rate Hike? Full Explanation of Interest Rate Conversions, Definitions, and Impact on Your Finances

How should investors respond during a quantitative tightening period?

Faced with market volatility driven by QT, investors should not panic. Crises often come with opportunities. Adopting a stable and flexible strategy can help not only survive the tightening period but also position for the next bull market.

Strategy 1: Reassess your portfolio and increase cash allocation

When the market outlook is uncertain, the timeless wisdom of “cash is king” becomes relevant again. Increasing cash allocation in your portfolio has two main benefits:

- Reduce overall risk: Lower exposure to high-risk assets and reduce losses during market declines.

- Preserve dry powder: Allow you to “buy the dip” when quality assets become undervalued during panic selling.

Review your holdings and consider reducing overvalued speculative stocks with weak or unstable profitability.

Strategy 2: Focus on companies with strong cash flow and low debt

In a tightening environment, corporate “financial strength” becomes especially important. Truly strong companies are those that generate stable cash flow from operations rather than relying on cheap debt. When selecting investments, focus on the following characteristics:

- Strong free cash flow: Indicates sufficient funds to cover interest expenses and sustain operations.

- Low leverage ratio: Lower debt means less pressure from rising interest costs.

- Pricing power (economic moat): Strong brands or technological advantages that allow companies to pass rising costs to consumers while maintaining profit margins.

Strategy 3: Use volatility for tactical positioning

Increased volatility is normal during balance sheet reduction, but it also creates opportunities for long-term investors. Instead of trying to predict market bottoms (which is nearly impossible), adopt more disciplined approaches:

- Dollar-cost averaging: continuously invest over time to buy more units during price declines and reduce average cost in the long run.

- Staggered buying: when you are optimistic about an asset but concerned about further declines, split your capital into multiple entries at different time points to diversify risk.

This approach helps overcome emotional fear and keeps focus on long-term value rather than short-term price fluctuations.

Frequently Asked Questions (FAQ) on Central Bank Balance Sheet Reduction

Q: How long does central bank balance sheet reduction last?

A: There is no fixed timeline for balance sheet reduction. Its duration depends on economic data, particularly inflation and labor market conditions. Central banks continuously monitor these indicators. If inflation is effectively under control or signs of economic recession emerge, they may slow down or even stop balance sheet reduction. In general, a full QT cycle may last several years.

Q: Does balance sheet reduction always lead to a bear market?

A: Not necessarily, but it is indeed one of the key catalysts of bear markets. Historical experience shows that during quantitative tightening periods, stock markets often perform weakly or enter a consolidation phase. It removes an important driver of market gains: liquidity and increases downside risk. However, market trends are also influenced by corporate earnings, geopolitics, and other factors, so it cannot be generalized.

Q: Should ordinary investors worry about balance sheet reduction?

A: There is no need to panic, but investors should remain alert and understand its impact. For most investors, the key is proper asset allocation and avoiding concentration in a single high-risk asset. Understanding how balance sheet reduction affects the market can help you make more informed decisions, such as increasing defensive assets during tightening periods and using market pullbacks to build long-term positions in quality assets.

Q: Does balance sheet reduction affect my mortgage?

A: Yes, but indirectly. Balance sheet reduction mainly affects long-term interest rates, and mortgage rates (especially fixed-rate mortgages) are closely linked to long-term government bond yields. When QT pushes bond yields higher, new mortgage rates usually rise as well. For existing fixed-rate mortgages, there is no impact. However, for floating-rate mortgages, rates may increase as overall market interest rates rise.

Conclusion

In summary, understanding the “meaning of central bank balance sheet reduction” and “quantitative tightening (QT)” is an essential subject for every modern investor. The essence of this policy is to withdraw excess liquidity from the market in order to combat inflation. However, this process inevitably places significant pressure on the stock market, especially on high-valuation growth stocks. In the face of market volatility caused by balance sheet reduction, investors should not panic or lose discipline. Instead, they should return to investment fundamentals, remain vigilant, carefully assess their asset allocation, and focus on high-quality companies that can maintain stable operations even in adverse conditions. Review your portfolio now, prepare for structural changes in the market, and only then can you move forward steadily and sustainably.