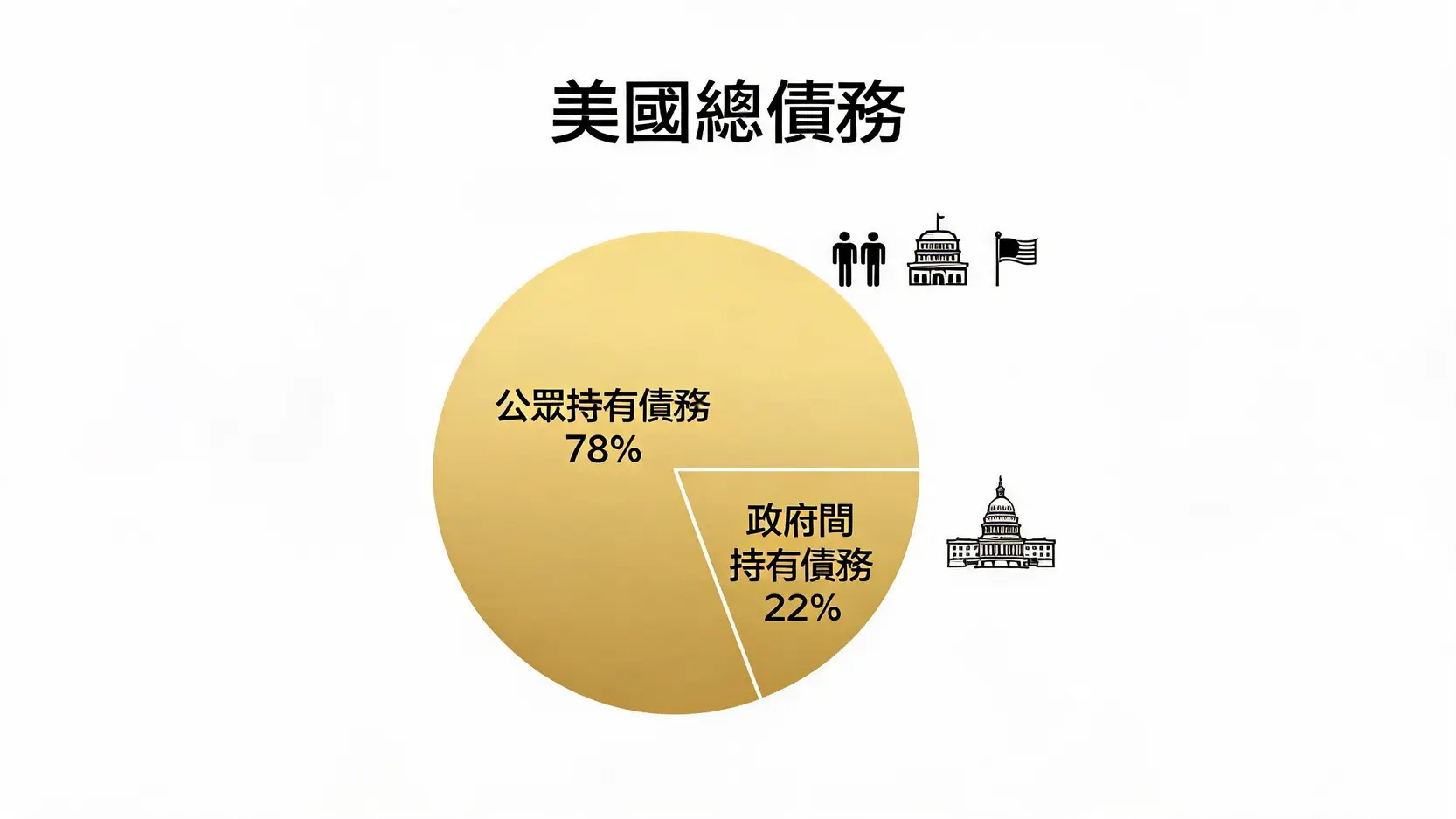

Composition of US National Debt: Public Debt vs. Intragovernmental Debt

Distinguishing between these two categories is crucial because when discussing “who owns US debt”, the focus is primarily on the first category, namely the domestic and foreign entities that hold publicly traded US government debt.

The History of US Debt Growth and Future Projections

The explosive growth of US debt did not happen overnight. Looking back, several major events accelerated debt accumulation, including the economic stimulus measures following the 2008 global financial crisis, years of spending on the War on Terror, and the massive fiscal relief packages introduced after the COVID-19 pandemic in 2020. Each crisis has largely been addressed through increased borrowing. According to projections from the Congressional Budget Office (CBO), if current policies remain unchanged, the US fiscal deficit will continue expanding over the next decade, with publicly held debt projected to reach an unprecedented 180% of GDP by around 2035. This steep upward trajectory lies at the heart of growing global market concerns.

The US Debt Ceiling: A Recurring Political Standoff

No discussion of US debt would be complete without mentioning the “debt ceiling”, a unique mechanism that has repeatedly turned into a political drama, leaving global financial markets on edge each time.

What Is the Debt Ceiling and Why Does It Exist?

The debt ceiling is the maximum amount the US federal government is legally allowed to borrow, as established by Congress. Unlike a credit card limit, it does not restrict future spending. Instead, it limits the government’s ability to finance expenditures that have already been approved (such as military salaries, Social Security benefits, and interest payments on government debt). The system was introduced during World War I to provide the Treasury with greater borrowing flexibility without requiring Congressional approval for every issuance. Today, however, it has evolved into a bargaining chip in political negotiations, allowing both parties to pressure each other during budget debates.

Historical Debt Ceiling Crises and Their Market Impact

Debt ceiling negotiations have become increasingly difficult in recent years. The most notable example occurred during the 2011 debt ceiling crisis, when political deadlock prompted Standard & Poor’s (S&P) to downgrade the US sovereign credit rating for the first time, from AAA to AA+, triggering severe volatility across global equity markets. A similar scenario unfolded again in 2023. Although lawmakers ultimately reached a last-minute agreement that suspended the debt ceiling through early 2025, the prolonged uncertainty damaged market confidence and increased the US government’s borrowing costs.

How Real Is the Risk of a “Technical Default”?

Although each debt ceiling crisis attracts widespread attention, the likelihood of the US actually “defaulting on its debt” is extremely low. If it were to happen, the consequences would be catastrophic, including:

- Destroy global confidence in the US dollar and US Treasuries.

- Trigger a sharp surge in interest rates, severely impacting businesses and consumers.

- Potentially spark a global financial recession.

For these reasons, no rational political leader would willingly accept responsibility for such an outcome. However, the risk of a “technical default” is real. This refers to a temporary delay in payments because Congress fails to raise the debt ceiling in time, forcing the Treasury to postpone certain obligations, such as government employee salaries or payments to contractors. Even a brief delay would be sufficient to damage economic confidence and unsettle financial markets. This recurring political standoff has become an unnecessary source of risk in itself.

Further Reading (Highly Recommended)

Safe-Haven Currency Rotation Strategy: Which Currencies Should You Buy During Times of Uncertainty? The Complete Guide to the US Dollar, Japanese Yen, and Swiss Franc

How to Reduce Investment Risk? Five Risk Management Strategies and Practical Diversification Techniques

Who Owns US Debt? Understanding the Holders of US Treasuries

Understanding who holds US Treasuries is key to assessing their stability. Many people mistakenly believe that China is the largest creditor to the US, but that is no longer the case. In reality, the ownership structure of US Treasuries is highly diversified, which helps spread risk to some extent.

Domestic Holders: The Federal Reserve, Social Security Funds, and Individual Investors

In fact, the largest holders of US Treasuries are domestic institutions and investors. They mainly include:

- The Federal Reserve (The Fed): Through open market operations (particularly during periods of monetary easing), the Fed purchases large amounts of US Treasuries to regulate market liquidity and interest rates.

- Government funds such as the Social Security Trust Fund: As mentioned earlier, these funds invest their surplus assets in US Treasuries, making them the largest holders of intragovernmental debt.

- Mutual funds, pension funds, banks, and insurance companies: These institutions hold US Treasuries as core portfolio assets due to their liquidity and safety.

- State and local governments, as well as individual investors: They also hold a substantial portion of US Treasuries as a conservative investment.

Foreign Holders: The Influence of Major Creditors Such as Japan and China

Among all foreign holders, Japan has long remained the largest overseas holder of US Treasuries. According to data from early 2026, the largest foreign holders of US Treasuries are ranked approximately as follows:

| Rank |

Country/Region |

Holdings (Approximate)

|

| 1 |

Japan |

~US$1.2 trillion |

| 2 |

United Kingdom |

~US$0.9 trillion |

| 3 |

China |

~US$0.7 trillion |

| 4 |

Belgium |

~US$0.45 trillion |

| 5 |

Canada |

~US$0.44 trillion |

| … |

Taiwan |

~US$0.3 trillion (Ranks Among the Top 10) |

Note: The data is subject to change and reflects an overview as of early 2026.

The Geopolitical and Economic Implications of Foreign Reductions in US Treasury Holdings

In recent years, one notable trend has been the gradual reduction of US Treasury holdings by several countries, including China. There are multiple reasons behind this trend:

- Geopolitical considerations: Against the backdrop of rising US-China tensions, reducing US Treasury holdings is viewed as a strategy to lessen dependence on the US dollar and mitigate the risk of potential financial sanctions.

- The need for economic diversification: Central banks around the world are seeking to diversify their foreign exchange reserves by allocating more assets to gold, the euro, and other alternatives.

- Market operations: In some cases, reductions in US Treasury holdings are intended to support exchange rate intervention and stabilize domestic currencies.

Although this trend has attracted considerable attention, it has not undermined the US Treasury market in the short term. Whenever a major seller emerges, other buyers (such as the United Kingdom and Belgium) have stepped in. However, over the long term, if global “de-dollarization” accelerates, it will undoubtedly increase US financing costs and challenge its financial dominance.

The Long-Term Economic Impact of Massive Government Debt

America’s continuously expanding national debt is like a frog slowly being boiled. Its long-term effects are gradually becoming more apparent, creating challenges for the economy on multiple fronts.

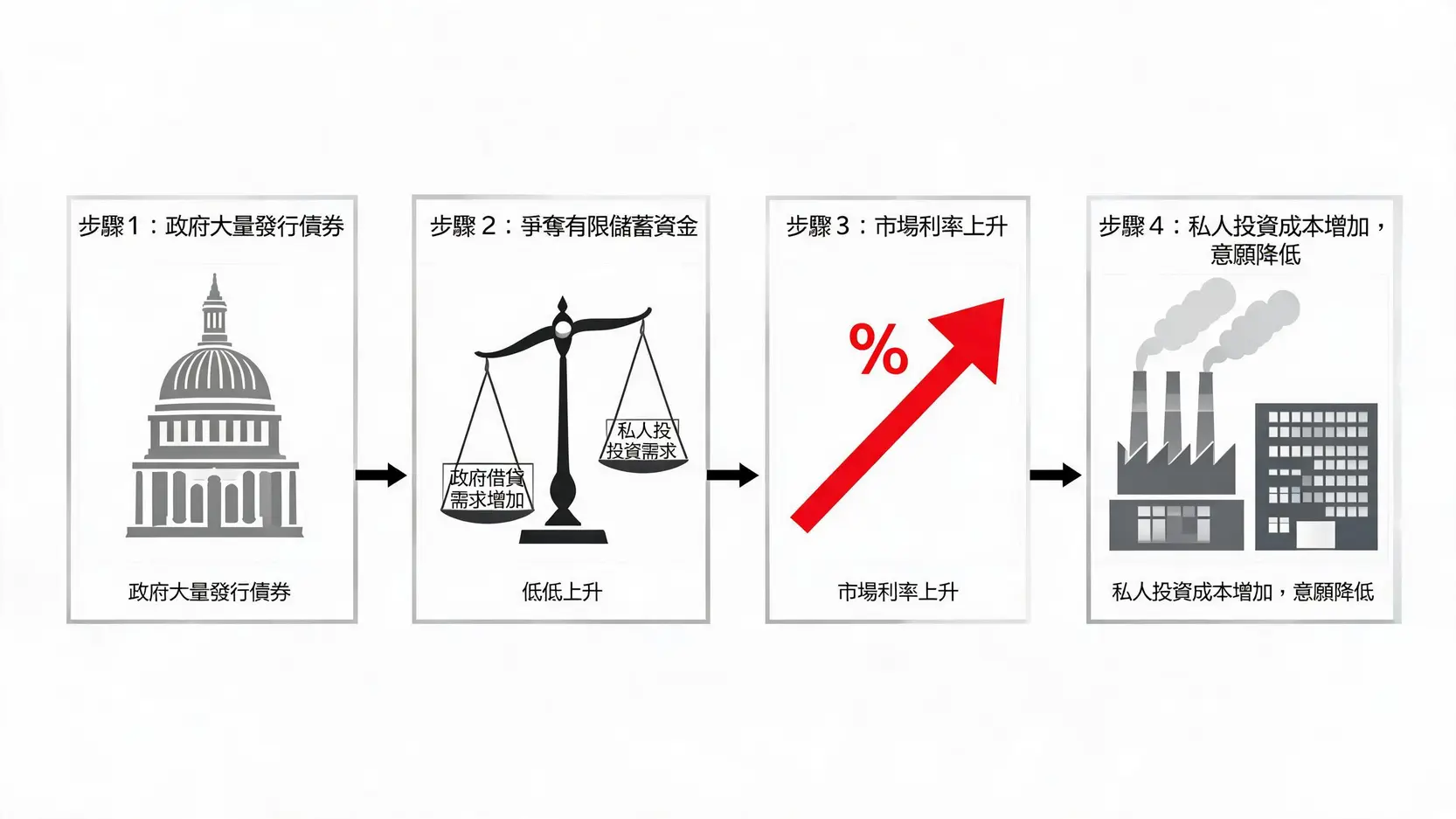

Crowding Out Effect: How Government Borrowing Affects Private Investment

When the government issues large amounts of bonds to raise funds, it competes with the private sector (including businesses and individuals) for a limited pool of savings. This pushes interest rates higher, increases borrowing costs for businesses, and reduces their willingness to invest and expand. This phenomenon is known as the “Crowding Out Effect”. Over time, innovation and productivity growth in the private sector may slow, ultimately reducing the economy’s long-term growth potential.