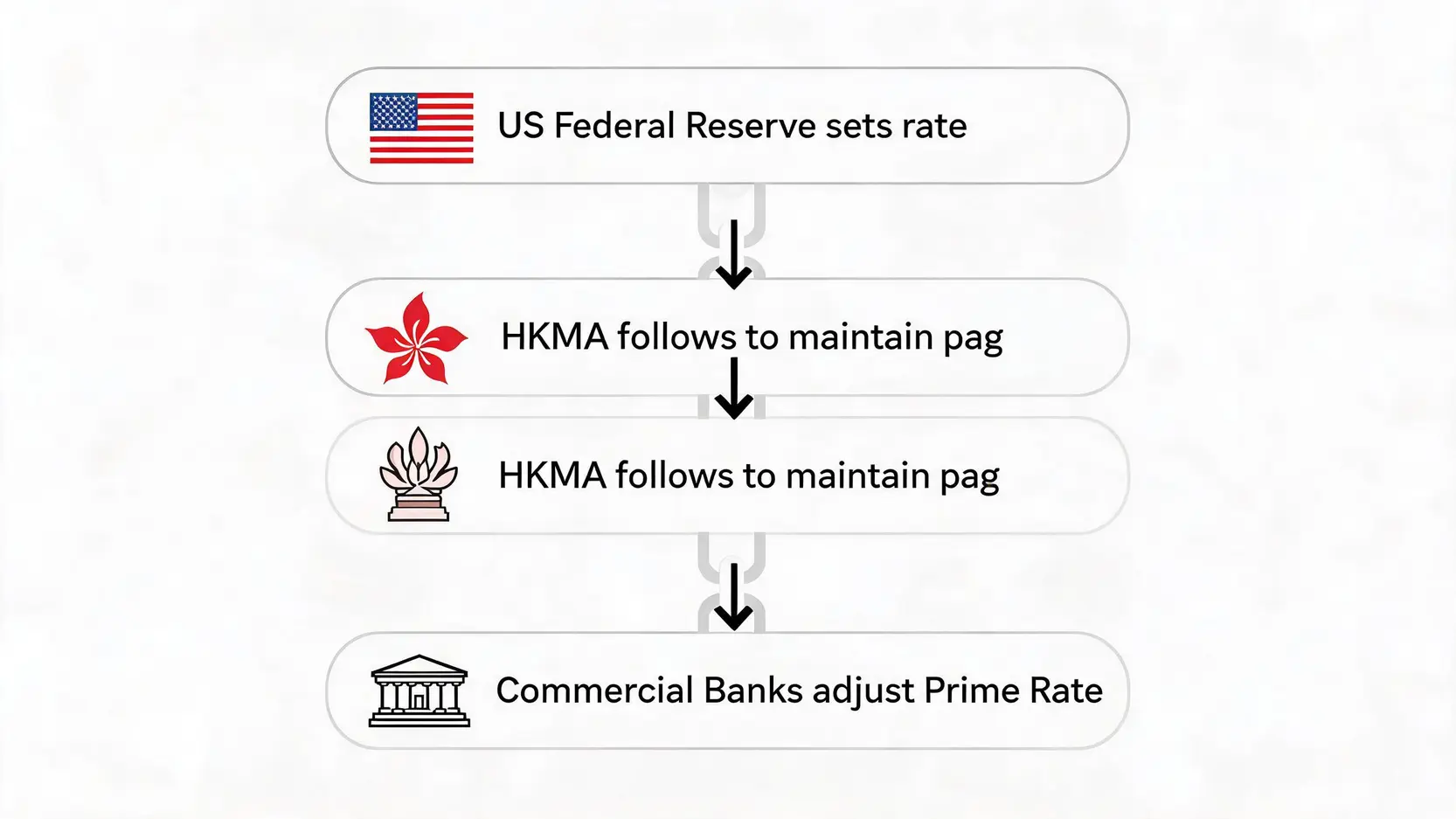

Figure 3: Interest Rate Transmission Mechanism Under the Linked Exchange Rate System

Expert Forecasts: Full Analysis of Hong Kong Prime Rate (P) Trends in 2026

Although the HKMA’s Base Rate closely follows the US, what the public cares about more is the commercial banks’ Prime Rate (P), which is directly linked to mortgage and loan costs. Prime Rates are independently determined by commercial banks and are mainly divided into “Large P” and “Small P”.

- Timing of adjustments: When deciding whether to adjust Prime Rates, commercial banks consider not only the HKMA’s benchmark rate, but also their own funding costs, the aggregate balance of the banking system, and market loan demand. Therefore, even if the US announces a rate cut, Hong Kong’s Prime Rate may not “immediately follow”. Banks may wait for a period of observation or for cumulative rate cuts to reach a certain level before making adjustments.

- Forecast direction: The market generally expects that once the US begins a rate cut cycle, Hong Kong’s Prime Rate will also move lower. Forecasts suggest that if the US cuts rates by 25 to 50 basis points in the second half of 2026, Hong Kong’s Prime Rate may also be reduced accordingly, although the magnitude may not fully match the US adjustment.

The Actual Impact of a Rate Cut Cycle on Hong Kong’s Property Market and Household Mortgage Burdens

The impact of rate cuts on Hong Kong’s property market is direct and significant. Lower interest rates mean lower monthly mortgage payments, directly reducing the financial burden on homeowners. This is referred to as an improvement in “mortgage affordability”.

- Stimulating buying demand: Lower mortgage burdens help improve the willingness and affordability of potential buyers to enter the market, supporting transaction volumes in the property market.

- Stabilizing asset prices: Lower borrowing costs help support asset prices, easing downward pressure on property prices and potentially driving a recovery if market sentiment improves.

- Releasing consumer spending power: For existing homeowners, lower monthly mortgage payments effectively increase disposable income. This additional capital may flow into the retail and consumer sectors, supporting the local economy.

In summary, although Hong Kong’s rate cut timeline remains passive, once rate cuts begin, the positive impact on the stock market, property market, and overall economy is worth anticipating. Investors and the public should closely monitor US interest rate developments in order to prepare and plan ahead.

Further Reading (Highly Recommended)

Complete Analysis of the Nasdaq ETF QQQ: From Beginner Basics to Advanced Strategies, Fully Understanding How to Invest in Technology Giants!

Complete Analysis of the Impact of US Interest Rate Hikes: 5 Major Effects on Hong Kong’s Stock and Property Markets and Response Strategies

Frequently Asked Questions (FAQ)

Q: If the US Cuts Interest Rates, Will Hong Kong Immediately Follow?

A: Not necessarily “immediately”. Under the Linked Exchange Rate System, the HKMA’s benchmark interest rate (or Base Rate) closely follows movements in the US federal funds rate in order to maintain Hong Kong dollar stability. However, the commercial banks’ Prime Rate (P), which is of greater concern to the public, is determined by banks based on their own funding costs and market conditions, and usually involves a certain lag. Banks may wait until the US has accumulated a certain level of rate cuts before reducing Prime Rates.

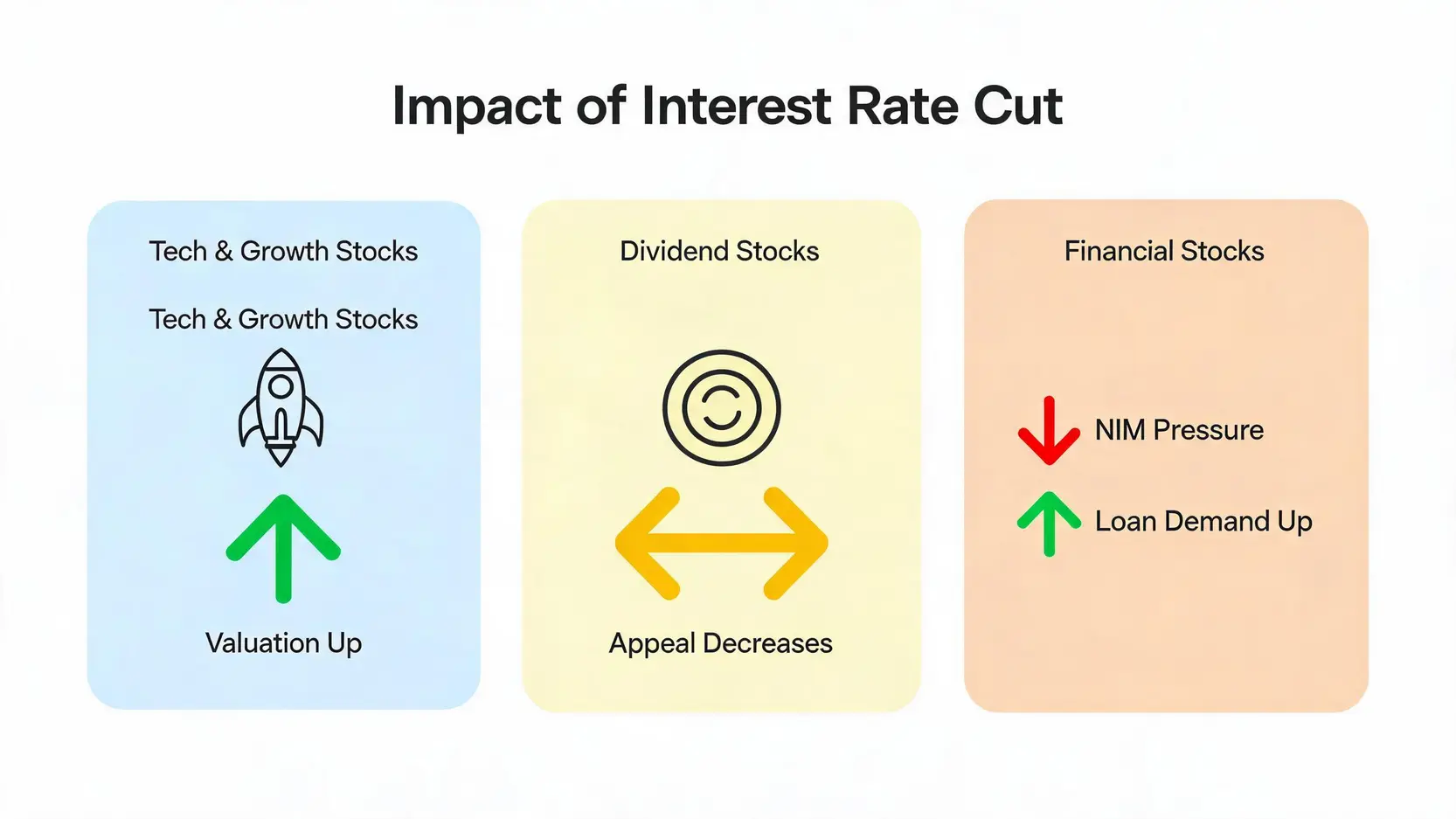

Q: What Specific Benefits Do Rate Cuts Bring to My Stock Investment Portfolio?

A: Rate cuts mainly provide three major benefits: First, they reduce corporate borrowing costs, helping improve profitability. Second, for technology stocks and growth companies, lower interest rate environments increase the present value of future cash flows, supporting valuation expansion. Third, increased market liquidity and stronger risk appetite help attract more capital into the stock market, supporting broader market gains.

Q: Besides Rate Cuts, What Other Factors Will Affect Stock Market Performance in 2026?

A: Beyond interest rate policy, key factors affecting stock market performance in 2026 include whether corporate earnings growth meets expectations, the strength of the global macroeconomic recovery (especially in the US, China, and Europe), geopolitical risks (such as regional conflicts and major national elections) as well as technological innovation in specific industries (including the development and application of artificial intelligence). Rate cuts only provide a favorable macroeconomic environment, while the long-term performance of the stock market still depends on fundamental factors.

Q: How Will Gold Prices React if Inflation Continues Cooling?

A: Traditionally, gold is viewed as a hedge against inflation, so cooling inflation may weaken its attractiveness. However, gold also functions as an alternative to the US dollar and as a safe-haven asset. If cooling inflation is accompanied by US rate cuts, the US dollar may weaken, which would benefit gold prices denominated in US dollars. In addition, if geopolitical instability persists, safe-haven demand for gold may also rise. Therefore, gold price movements are the result of multiple factors interacting, and cannot be judged solely based on inflation.

Q: During a Rate Cut Cycle, Should All Capital Be Invested Into the Stock Market?

A: No. At any time, diversification remains the golden rule of risk management. Although rate cut cycles are generally favorable for equities, markets still contain significant uncertainty. Investors are advised to allocate assets reasonably according to their own risk tolerance. For example, before rate cuts begin, investors may lock in yields from high-quality medium- and long-term bonds, while also allocating part of their capital into stocks with growth potential and retaining a certain proportion of cash to respond to sudden market volatility.

Conclusion

In summary, the core themes shaping the 2026 investment market revolve around cooling inflation, interest rate shifts, and the pace of economic recovery. Clearly understanding the structural impact mechanism of cooling inflation on different stock market sectors, closely monitoring Federal Reserve policy direction to forecast Hong Kong’s rate cut timeline, and combining this with broader global economic outlook analysis are key factors for investors seeking to outperform the market during the current cycle. From valuation recovery in technology stocks to the positive effects of rate cuts on Hong Kong’s property market, potential opportunities exist throughout the market. Facing the coming changes in market conditions, investors should immediately review and flexibly adjust their portfolios in order to secure stronger positioning and capture the next wave of growth potential.