How the Yen Carry Trade Operates

The Defenders (Japan’s Ministry of Finance): From Verbal Intervention to Direct Action

In response to speculative pressure, Japan’s Ministry of Finance, which oversees exchange rate policy, employs a layered defense strategy:

- Stage One – Verbal intervention: The Finance Minister and senior financial officials frequently issue warnings that excessive and speculative currency movements are undesirable, attempting to cool market sentiment through public statements.

- Stage Two – Direct intervention: When verbal warnings fail and the exchange rate breaks through key defense levels such as 160, the Ministry of Finance instructs the Bank of Japan, acting as its agent, to sell US dollars and buy yen directly in the market. Although this can temporarily strengthen the yen, the sustainability of the effect depends on both the scale and timing of the intervention.

Corporations and Households: Hedging and Adapting to Exchange Rate Volatility

Amid this battle between major market participants, Japanese corporations and households cannot remain unaffected. Large exporters (such as automobile and electronics manufacturers), benefit from a weaker yen through higher profits. However, they often engage in currency hedging to lock in those gains. Meanwhile, importers and companies dependent on imported raw materials face substantial cost pressures and may be forced to raise product prices. For ordinary households, the most immediate impact comes through rising prices, higher living costs, and increasingly expensive overseas travel.

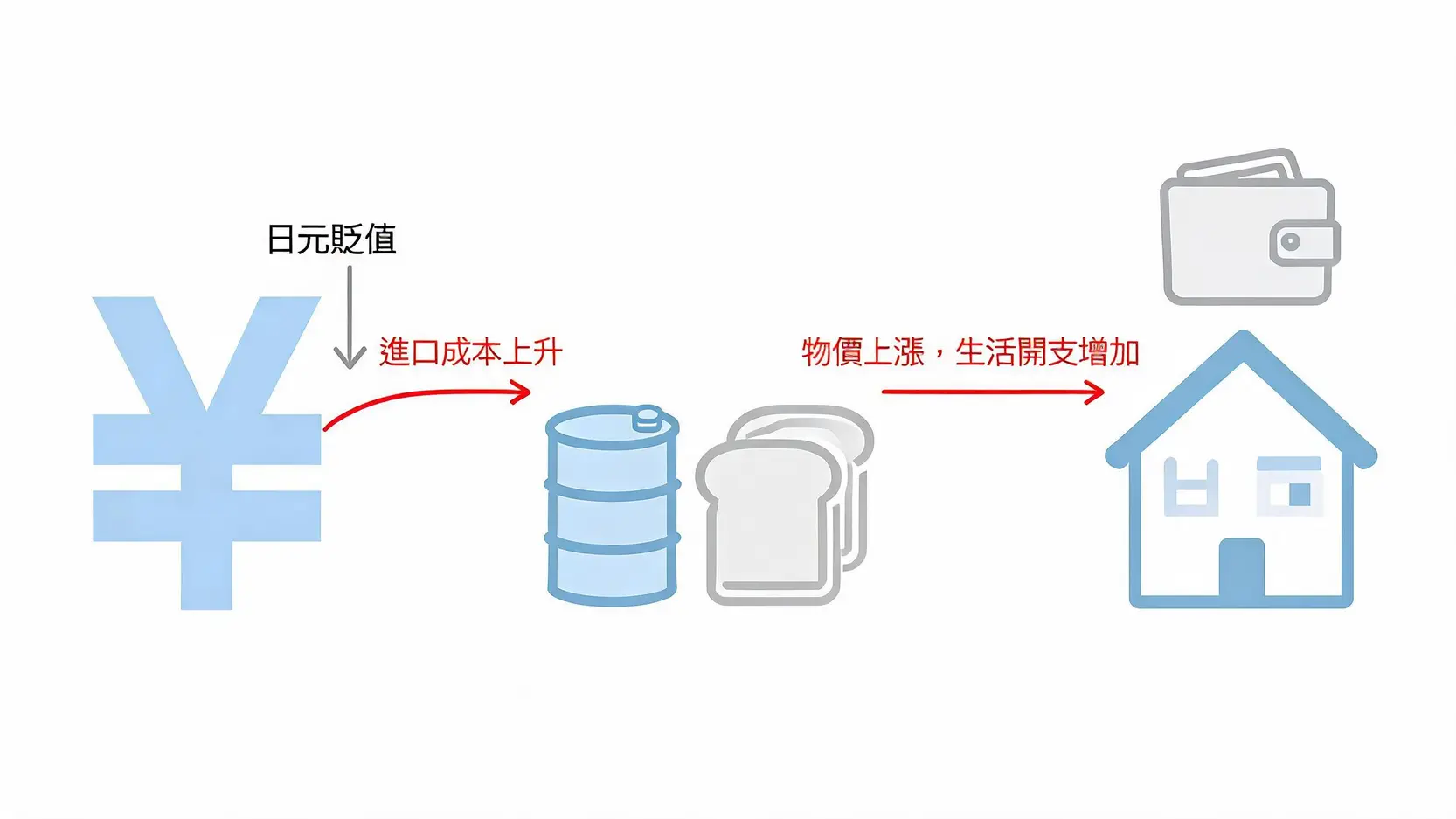

The Chain Reaction of Breaking Above 160: A Comprehensive Impact From the Economy to Daily Life

If the USD/JPY 160 psychological threshold is ultimately breached and continues to move higher, the resulting chain reaction will have broad and far-reaching consequences for Japan’s economy and society. This is precisely the scenario policymakers are trying their hardest to avoid.

“Bad Yen Depreciation”: How Rising Energy and Food Prices Impact Household Spending

Once the market begins to expect “continued yen depreciation”, the pressure from imported inflation can intensify rapidly. This is not merely a matter of paying a little more at the gas station or supermarket. It can evolve into a “cost-push” inflation spiral. Businesses are forced to pass rising costs on to consumers, resulting in broad-based price increases. Wage growth often fails to keep pace with inflation, causing household purchasing power to decline and consumer spending to weaken, ultimately dragging down overall economic growth.

Diverging Corporate Profits: Exporters’ Joy and Importers’ Nightmare

Yen depreciation further “widens the gap” between winners and losers in Japan’s corporate sector.

Exporters’ joy: Export giants such as Toyota benefit significantly, as overseas revenues translate into more yen, boosting earnings reports and supporting share prices.

Importers’ nightmare: Companies dependent on imported energy, such as utility providers, as well as retailers sourcing products from overseas (including Nitori and Fast Retailing), the parent company of Uniqlo, face soaring costs and severely compressed profit margins. This structural divergence in profitability is not conducive to balanced economic development.

Triggering a Vicious Cycle: How Yen Depreciation Further Accelerates Capital Outflows

Persistent yen depreciation can undermine confidence in Japanese assets among both domestic and international investors. Japanese investors (including individuals and large institutions such as insurance companies and pension funds) may become increasingly motivated to move capital overseas in pursuit of higher returns and to avoid exchange rate losses. This capital outflow itself creates additional demand to sell yen and buy US dollars in the foreign exchange market, placing even greater downward pressure on the yen and creating a vicious cycle that becomes increasingly difficult to break.

Further Reading (Highly Recommended)

Timing Reverse Trades Around Yen Intervention: Identifying Profitable Turning Points When the Bank of Japan Steps In

The Complete Guide to Japanese Yen Deposit Rates: Understanding Yen Time Deposit Recommendations and Exchange Rate Trends

Policy Options and Market Outlook After Breaking Above 160

Although Japanese authorities have mounted a strong defense around the 160 level, market challenges will persist as long as the root cause of yen weakness, namely the large US-Japan interest rate differential, remains in place. If 160 is ultimately breached, what options remain available to Japan?

Increasing Intervention Efforts: How Much “Ammunition” Does the Bank of Japan Have Left?

Foreign exchange intervention requires the use of a country’s foreign exchange reserves. According to data from Japan’s Ministry of Finance as of early 2026, Japan’s foreign exchange reserves totaled approximately US$1.2 trillion, ranking among the largest in the world. This means Japan possesses substantial “ammunition” to counter speculative market attacks. However, foreign exchange reserves are not unlimited, and large-scale intervention may itself be interpreted by the market as a sign of desperation. Therefore, intervention alone is unlikely to reverse a long-term trend driven by economic fundamentals.

Monetary Policy Shift: Is a Rate Hike the Ultimate Solution?

To fundamentally solve the yen depreciation problem, the most effective tool is to narrow the US-Japan interest rate differential through a shift in Bank of Japan monetary policy, namely higher interest rates. However, this presents an extremely difficult decision for the Bank of Japan:

- Government debt burden: Japan carries one of the heaviest government debt burdens among developed economies. Any rate increase would sharply raise annual interest payments on government bonds, placing significant pressure on public finances.

- Risk of economic disruption: Japan’s economy has long depended on a low-interest-rate environment. Many businesses and households have loans tied to low borrowing costs. A rapid increase in rates could trigger corporate bankruptcies and significantly increase mortgage burdens, threatening the country’s fragile economic recovery.

As a result, even after exiting negative interest rates in 2024, the Bank of Japan is likely to proceed with extreme caution. Any future rate hikes are expected to be gradual and limited, making it difficult to significantly reduce the approximately 5% interest rate gap with the US in the near term.

FAQ

Q: If USD/JPY breaks above 160, how much further could it rise?

A: There is no definitive answer. The outcome depends primarily on three factors: 1) Federal Reserve policy. If the US begins cutting rates, pressure on the yen could ease. 2) The pace of Bank of Japan rate hikes. If tightening occurs faster than expected, the yen may rebound. 3) The determination and scale of intervention by Japan’s Ministry of Finance. If no stronger measures follow a break above 160, the market may begin targeting the next psychological levels at 165 or even 170.

Q: At what key levels has the Japanese government intervened in the past?

A: Significant interventions in recent years include September and October 2022, when the Japanese government purchased yen as USD/JPY approached 145 and 151.9. The most recent major intervention occurred between late April and May 2024, after the exchange rate first broke above 160. The record-sized intervention temporarily pushed USD/JPY from above 160 back below 155.

Q: As an ordinary person, how does yen depreciation affect my daily life?

A: The impact is multifaceted. For people who enjoy traveling to Japan or purchasing Japanese products, a weaker yen is good news because the same amount of Taiwan dollars or Malaysian ringgit can be exchanged for more yen, effectively providing a discount. On the other hand, if you frequently purchase imported Japanese automobiles, electronics, cosmetics, or food products, their prices may rise because of exchange rate movements.

Q: Why doesn’t the Bank of Japan simply raise interest rates aggressively to stop yen depreciation?

A: This is a difficult trade-off. While aggressive rate hikes could effectively support the yen, they could also trigger a domestic “debt bomb”. The Japanese government carries substantial debt, and higher rates would significantly increase debt servicing costs. At the same time, many businesses and households have become accustomed to low-interest-rate borrowing. Sudden rate hikes could result in widespread defaults and bankruptcies, causing economic damage potentially greater than the impact of yen depreciation itself. Consequently, the Bank of Japan must walk a tightrope between “exchange rate stability” and “financial stability”.