Severance Payment vs Long Service Payment: Understand the Differences at a Glance.

In simple terms, severance payment is specifically for “redundancy” while long service payment covers various other qualifying termination circumstances.

As an Employer, How Should You Respond to the Abolition of MPF Offsetting?

The abolition of MPF offsetting undoubtedly increases the potential financial burden on employers. In response, the government has introduced corresponding support measures to assist enterprises (especially small and medium enterprises) in achieving a smooth transition.

Details of the Government Subsidy Scheme: Who Is Eligible? How Is the Subsidy Calculated?

The government has established a 25-year scheme with a total funding amount of tens of billions, known as the “Designated Savings Account Scheme”, to subsidize employers in paying severance payment and long service payment after the abolition of offsetting. The subsidy amount will decrease gradually over the years, with a higher subsidy ratio in the early stage to encourage employers to plan ahead.

- Eligibility: All employers (especially small and medium enterprises) are eligible to apply.

- Subsidy calculation: The subsidy amount is linked to the number of employees, wage levels, and the severance payment or long service payment amount in each dismissal case. In the initial stage of the scheme, the subsidy cap per case can reach tens of thousands of dollars.

- Purpose: To alleviate employers’ cash flow pressure during the initial transition period, rather than to fully exempt them from payment obligations.

Employers should closely monitor the application details and procedures issued by the Labour Department to ensure that they can make full use of this resource when necessary.

Can Early Dismissal Help Employers Avoid the New Legislation?

This is a sensitive but realistic question. In theory, dismissals occurring before the “transition date” of May 1, 2025 will be handled entirely under the old system, and employers may still carry out MPF offsetting. However, if an employer intends to circumvent the long-term financial responsibility under the new legislation through large-scale “early dismissals”, the following risks may arise:

- Legal risk: If proven to be malicious or unreasonable dismissal, it may trigger labor disputes and legal proceedings.

- Reputational damage: Large-scale layoffs may seriously affect corporate image and employee morale.

- Talent loss: Outstanding employees may voluntarily resign due to a lack of security, leading to higher long-term operating costs.

Prudent employers should adopt proactive planning measures, such as making provisions and understanding the government subsidy scheme, rather than engaging in short-sighted avoidance behavior.

Frequently Asked Questions (FAQ)

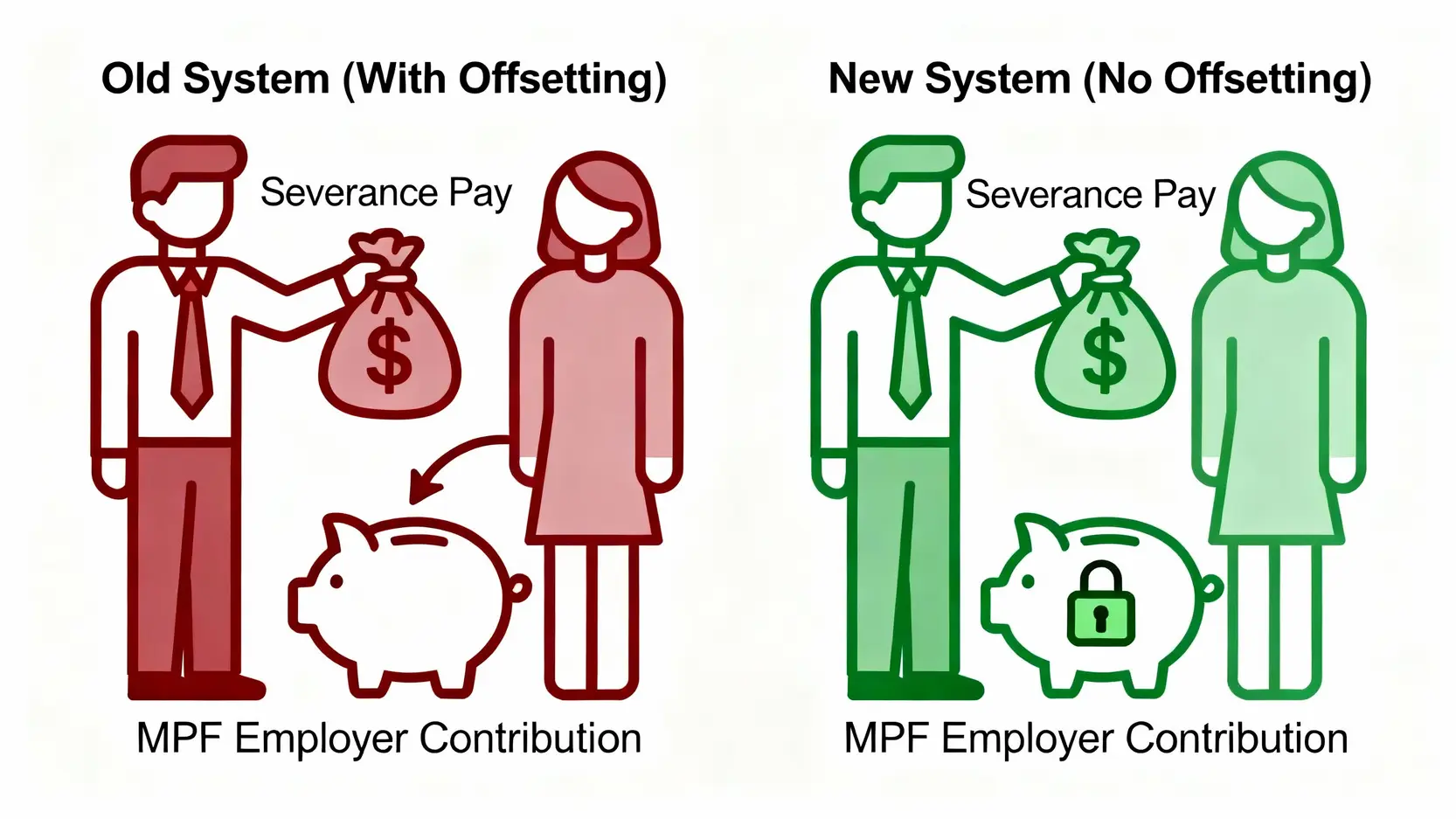

Q: After the abolition of offsetting, are employers completely prohibited from using MPF to pay severance payment?

A: Not entirely. The key lies in the “transition date” (May 1, 2025). For severance payment or long service payment arising from an employee’s service years before the transition date, the employer may still use the accrued benefits derived from MPF contributions to offset the payment. However, for service years after the transition date, offsetting is absolutely prohibited.

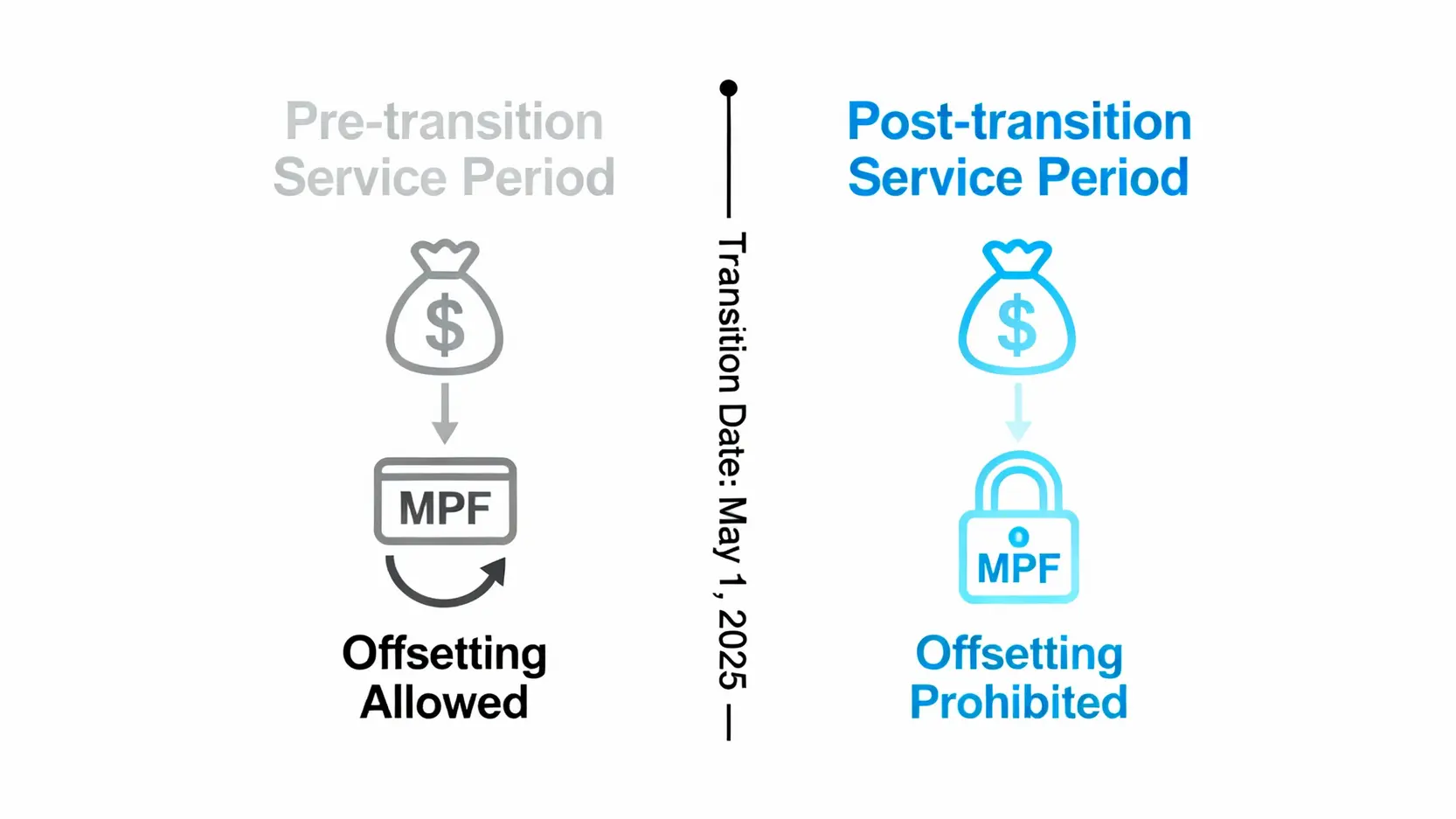

Q: If I commenced employment before May 1, 2025, how will my severance payment be calculated?

A: Your severance payment will be calculated in two parts. The first part is based on your service years before May 1, 2025, and this portion may be offset. The second part is based on your service years after that date, and this portion cannot be offset. Ultimately, you will receive the total of these two parts, but the employer is only required to pay cash separately for the second part.

Q: Where can I find the Labour Department’s official calculator?

A: To facilitate estimation for employers and employees, the government has launched an official online calculation tool. You can visit the Abolition of “Offsetting” website to access this practical calculator. Simply enter the relevant information to obtain an estimate of severance payment, long service payment, and the government subsidy amount.

Q: What Is the Maximum Amount for Severance Payment and Long Service Payment?

A: Under the current “Employment Ordinance”, regardless of your wage level or length of service, the maximum amount of severance payment or long service payment is capped at HK$390,000. This cap applies to both pre-transition and post-transition calculations.

Conclusion

In summary, the abolition of MPF offsetting marks a significant step forward in safeguarding labor rights in Hong Kong, as it rectifies the previous system loophole that eroded employees’ retirement savings. Whether you are an employee or an employer, you must thoroughly understand the new severance payment calculation method, especially the principle of division before and after the “transition date”. Remember the key date of May 1, 2025, and make good use of the Labour Department’s official resources and calculator on severance payment to accurately plan for and safeguard your rights. In the face of this major reform, clear understanding and adequate preparation are the best responses.