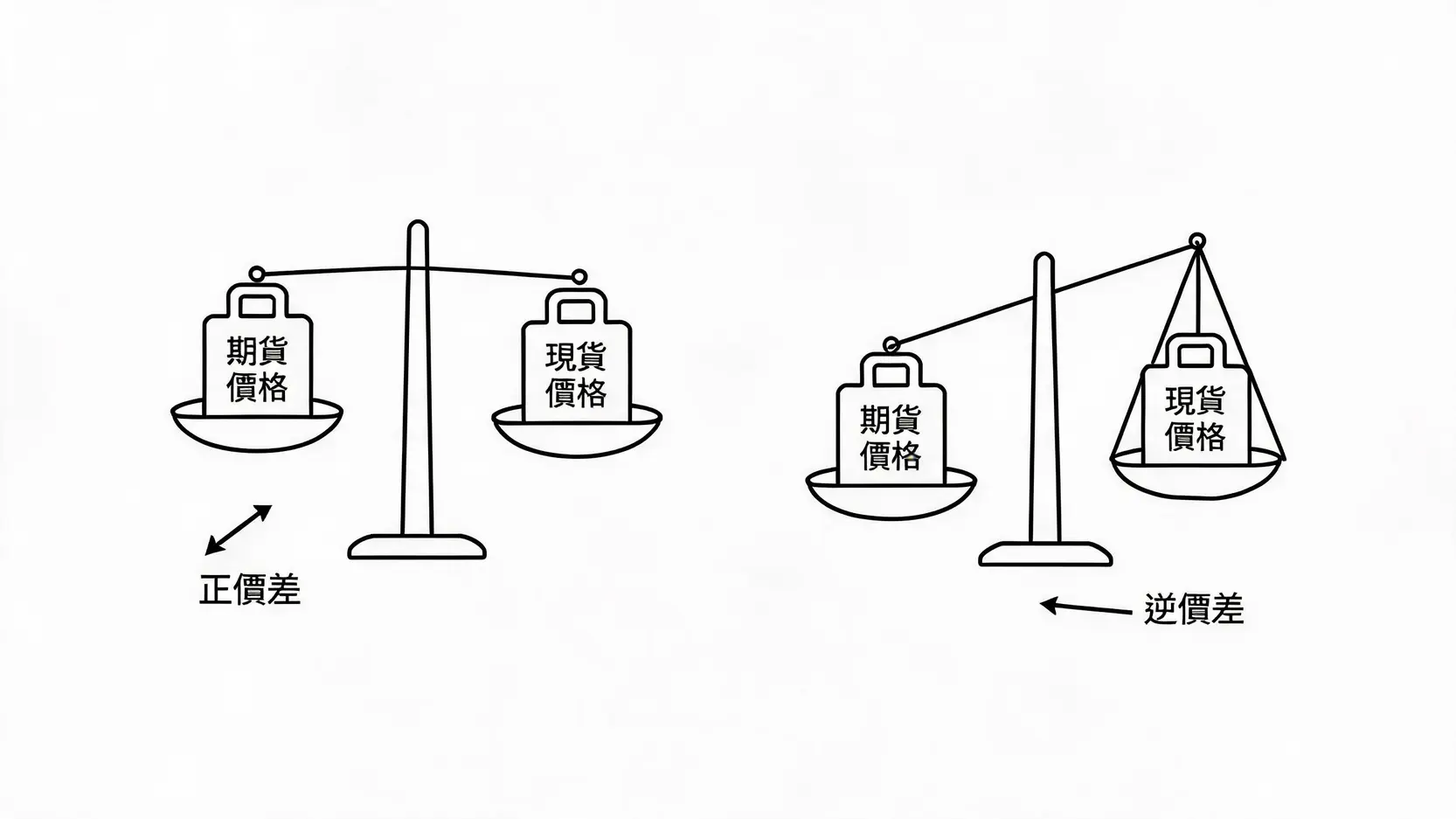

Basic Concept Diagram of Contango and Backwardation

Contango Expansion: Excessive Market Optimism or Abundant Liquidity?

Under normal circumstances, a stable contango indicates that investors are optimistic about the future market and are willing to buy forward contracts at a higher premium. However, if contango expands sharply within a short period, it often suggests that market sentiment has entered an overheated stage, and irrational buying at high levels may even appear. At this point, experienced traders will begin to guard against the risk of a pullback from elevated levels and consider deploying a reverse contango/backwardation arbitrage strategy, locking in risk-free or low-risk profits when the two prices converge by shorting futures and going long spot.

Sharp Backwardation Expansion: Spreading Panic or an Excellent Buying Opportunity?

An abnormal expansion in backwardation is usually accompanied by market panic and strong hedging demand. When Taiwan stocks face a sharp selloff, institutional investors and major market players often build short positions in the futures market to protect their spot assets, and strong selling pressure quickly pushes futures prices below spot prices. If the backwardation is far beyond the historical average and is accompanied by massive trading volume, this is often a signal that panic has reached an extreme, also known as the “oversold zone”. Investors who know how to observe this phenomenon can look for excellent swing buying opportunities, or decisively execute backwardation arbitrage to profit from prices returning to a reasonable level after market sentiment stabilizes.

Analysis of the Linkage Between Market Trends and Spread Changes: Practical Analysis of Backwardation Arbitrage

There is a close relationship between overall stock market trend changes and spread movements. Simply observing the rise and fall of the index can easily lead investors into traps set by major players. If spread changes are included as an auxiliary indicator, the win rate of market judgment can be significantly improved.

Spread Characteristics in a Bull Market

In a steady bull market, spot and futures markets usually rise in sync and at a moderate pace. If a slight backwardation appears during the upward process, it is usually a healthy sign of position consolidation, indicating that the market has not yet become overheated and still has upward momentum ahead. If sudden negative news causes short-term backwardation to expand abnormally, it is often a good time to buy high-quality assets on dips.

Spread Characteristics and Hedging Demand in a Bear Market

When the broader market enters a bear trend, risk-off sentiment rises sharply in the investment market, and the futures market often faces heavy institutional short-side pressure, causing backwardation to become normalized and continue deepening. At this stage, during every technical rebound, if contango appears, or the original backwardation quickly converges to parity, it is often a sign that institutional investors are taking short-term profits and luring buyers into the market, meaning the rebound may end at any time. Therefore, in a bearish structure, do not rashly build heavy long positions simply because the spread briefly turns positive.

Beyond Futures-Spot Arbitrage: Advanced Futures-Spot Spread Arbitrage Trading Strategies

Although traditional futures-spot spread arbitrage (such as buying spot and shorting futures, or doing the reverse), carries relatively controllable risk, it often requires a large amount of capital, and the potential profit space is limited. For traders seeking higher capital efficiency and more diversified operations, the following advanced spread trading models can be used flexibly:

Calendar Spread: Using Spreads Between Contracts with Different Expiry Months

Calendar spread arbitrage refers to simultaneously buying and selling futures contracts with different expiry months but the same underlying asset. For example, buying near-month Taiwan Index Futures while shorting far-month Taiwan Index Futures. This strategy does not predict the absolute direction of the broader market, but focuses on the convergence or divergence characteristics of the spread between the two contracts. Compared with one-sided speculative trading, calendar spread arbitrage carries lower systematic risk, and exchanges usually offer more flexible margin requirements for such positions, making it suitable for prudent investors.

Inter-Commodity Arbitrage: Between Different Products with High Correlation

This type of strategy targets two financial products with historically high correlation in price movements, such as Taiwan Index Futures and Electronics Futures, or gold and silver futures. When the relative price relationship between the two deviates from its long-term statistical normal range, investors can buy the relatively undervalued product while selling the relatively overvalued product. Once the price relationship returns to its historical mean, the position can be closed for profit.

Spread Protection Strategies Combined with Options Portfolios

When executing large-scale futures-spot spread arbitrage, the biggest concern is encountering an extreme black swan event, causing the spread to diverge sharply in an instant and triggering margin calls. By combining options, traders can build a strong protective net for arbitrage positions. For example, while executing a spread trade, they can buy deep out-of-the-money options as tail risk protection. Although this slightly sacrifices part of the potential profit, it can strictly lock the maximum loss under extreme market conditions within a tolerable range. Investors who want to conduct an in-depth analysis of historical trends can refer to Taiwan: Taiwan Stocks vs. Taiwan Index Futures Spread Historical Data to build a more stable statistical model.

Frequently Asked Questions FAQ: Common Issues in Futures-Spot Spread Arbitrage

Can I decide whether to buy or sell stocks based only on spreads?

Although spread data is an excellent leading market indicator, it is absolutely not suitable as the sole basis for entry and exit decisions. Many factors affect the divergence and convergence of spreads, including index points lost from corporate ex-dividend adjustments, institutional settlement strategies, and foreign capital FX arbitrage demand. In practice, it should be combined with technical chart structures, capital flow trends (such as net buying and selling by the three major institutional investors) and the macroeconomic backdrop for a comprehensive evaluation.

Is foreign investors’ futures open interest related to spreads?

The relationship is extremely close. Foreign investors have absolute pricing influence in Taiwan’s stock index futures and spot markets. When foreign investors significantly accumulate short futures open interest, the massive hedging and speculative selling pressure often deliberately suppresses futures prices, causing backwardation to expand rapidly. Tracking the linkage between open interest and spread changes at the same time can help you more accurately uncover the true intentions of major foreign institutional players.

Are retail investors suitable for calendar spread arbitrage?

As long as they have solid knowledge of how futures work and strict awareness of capital control, retail investors can absolutely participate in calendar spread arbitrage. Compared with one-sided long or short trades that carry extremely high leverage risk, the net position volatility of calendar spread arbitrage is relatively moderate, making it very suitable for traders who do not want to withstand sharp market swings and are seeking long-term stable returns.

Under what circumstances is backwardation arbitrage most suitable?

When the overall market experiences irrational panic selling, causing the degree of backwardation to far exceed the statistical average of the past three to five years, while the fundamentals have not seen any explosive, devastating major negative event, it is usually an excellent time to initiate backwardation arbitrage (buying severely undervalued futures while shorting spot or an equivalent ETF). As long as you patiently wait for panic sentiment to fade and futures and spot prices to forcibly converge back to a reasonable range, you can smoothly take profit.

Conclusion

Treating contango and backwardation as a thermometer for market sentiment and cross-checking them with technical and capital flow factors can give you market insight beyond that of ordinary retail investors. Whether you only use them as an auxiliary tool for judging bullish or bearish market conditions, or are preparing to personally execute futures-spot spread arbitrage, contango/backwardation arbitrage, or advanced backwardation arbitrage strategies, this knowledge will become a practical weapon for surviving volatile markets. Continue refining your sensitivity to subtle changes in spreads, and you will be able to achieve a higher win rate and more substantial stable returns over the long investment journey.