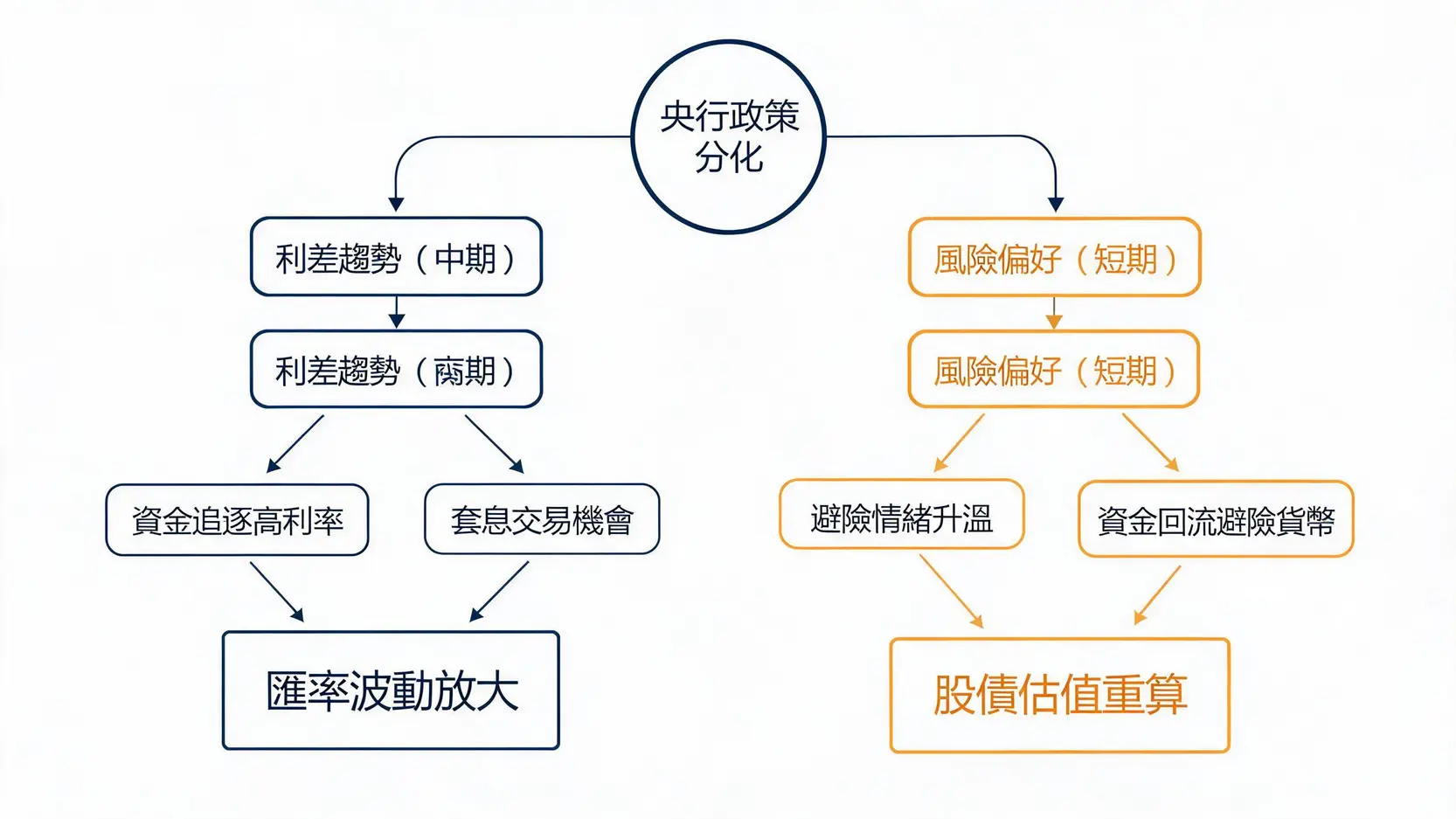

Central bank policy divergence: interest rate differentials (medium term) + risk appetite (short term) jointly determine FX and asset volatility

Breaking Down the Core Landscape of Central Bank Policy Divergence and Repeated Shifts in Rate Cut Expectations

In plain language, central bank policy divergence means that at the same point in time, interest rate directions across different countries are not aligned. Some are hawkish (tightening, relatively high interest rates, or rate hike pressure), some are dovish (preparing to cut rates or maintain easing), and some are waiting on the sidelines. This environment most easily leads to two things:

- Amplified exchange rate volatility: As capital chases interest rate differentials, and can also instantly flow back into safe-haven currencies when risk rises.

- Asset valuation repricing: stock and bond markets will repeatedly reprice based on “discount rates” and “economic expectations”.

Taking the US as an example, the Federal Reserve’s meeting statements and interest rate decisions remain the anchor for global risk assets. To grasp the most authoritative original policy text and meeting schedule, you can directly refer to: The Fed – Meeting calendars and information. When the market becomes overly optimistic about rate cut expectations, but economic data remains inconsistent, the US dollar and US Treasury yields often enter a tug-of-war of “falling first, then rebounding”, driving synchronized volatility in Asian currencies and stock markets.

The key is: under policy divergence, you cannot think only in terms of “long/short US dollar”. You must look at both interest rate differential trends and risk appetite. Interest rate differentials are the medium-term driver, while risk appetite is the short-term switch. When the two point in the same direction, the trend is the smoothest; when the two conflict, retail investors’ positions are most easily shaken out.

Tightening Pressure and FX Implications from the Hawkish Camp (Bank of Japan, Bank of Korea)

When Japan or South Korea’s policy stance leans tighter, the market usually interprets it on two levels:

- The relative attractiveness of local-currency interest rates rises: capital has the potential to flow back, supporting the yen and Korean won.

- Risk asset valuations come under pressure: if tightening leads to tighter financial conditions, stock market volatility may increase in the short term.

However, note that yen trends are driven not only by interest rate differentials, but also by “risk-off sentiment”. In other words, when risk events intensify, the yen may experience sharper short-term volatility than interest rate differentials would suggest. If you already hold positions in Japanese stocks or yen assets, be sure to treat “FX hedging” as part of your allocation, rather than a remedy after the fact.

For further reference, you can read: Must-Read Japan Investment Risks: 5 Major Potential Risks Beyond Yen Depreciation You May Not Know, which provides a very practical overview of yen risk sources and tools (such as FX forwards).

The Policy Swings of the Wait-and-See and Moderate Camp (Federal Reserve, ECB): How They Affect Asset Allocation

When the Federal Reserve and the ECB are caught in the awkward zone where “inflation has cooled, but the economy cannot be allowed to stall”, the most common market pattern is: rate cut expectations are fully priced in first → data fails to cooperate → expectations are unwound. For investors in Taiwan and Malaysia, the biggest impacts are:

- Amplified volatility in US dollar assets: the US Dollar Index, US Treasuries, and technology stocks can easily fluctuate together.

- The euro’s trend becomes more like a “combined question of policy and economic conditions”: if you have euro exposure (such as European stock ETFs or euro deposits), you need to watch both policy and growth momentum.

If you want to fully understand the euro’s exchange rate logic in one read, you can also read: Complete Guide to the Euro Exchange Rate: Master the Latest Trends, Currency Exchange Strategies, and Historical Data. This type of content is very helpful for investors trading euro-related pairs (such as EUR/USD and EUR/JPY).

FX Investment Strategies amid Central Bank Policy Divergence: How to Use Interest Rate Differential Trades and Rate Cut Expectations

In an environment of policy divergence, the most “repeatable” core of the FX market is actually two words: interest rate differentials. However, interest rate differential trades (carry trades) do not mean blindly buying high-yielding currencies, because the interest you earn may be wiped out by FX losses in one move. A truly robust FX investment strategy must break the “reason for entry” into three layers:

- Direction of interest rate differentials: widening differentials usually support trend continuation; narrowing differentials increase reversal risk.

- Market risk appetite: when risk appetite rises, high-yielding currencies usually perform well; when risk appetite weakens, capital flows back into safe-haven currencies.

- Event schedule: central bank meetings, inflation data, and employment data are the switches for sharp short-term volatility.

The same applies to rate cut expectations. If the market has already priced them in early, their actual implementation may instead become a case of “good news fully priced in”. Therefore, FX trading requires learning to distinguish whether you are trading an expectations gap or chasing news headlines.

How to Use Widening and Narrowing Interest Rate Differentials for Carry Trades: The Risk Bottom Line of FX Investment Strategies

The essence of carry trades is to borrow low-yielding currencies and buy high-yielding currencies to earn the interest rate differential. To make it more like a “strategy” rather than a “directional bet”, you can use the following three checkpoints:

- Are interest rate differentials still widening? If the high-yielding country signals a shift toward rate cuts, or the low-yielding country may turn hawkish, carry positions should become more conservative when differentials narrow.

- Has the exchange rate entered a high-volatility zone? When volatility surges, interest income is usually not enough to offset margin fluctuations and drawdowns.

- Do you have a stop-loss and deleveraging mechanism? Leverage is common in forex trading. The problem is not leverage itself, but the lack of “exit rules”.

For Taiwanese investors, a common scenario is holding US dollar time deposits or US dollar-denominated bonds on one hand, while wanting to pursue higher returns through FX on the other. In this case, FX should be treated more as a “satellite strategy”. First ensure that the core asset allocation can withstand drawdowns, then discuss enhancement.

Keyword variation reminder: during periods of central bank policy divergence, changes in the interest rate path are usually more important than a single meeting; and changes in the interest rate path will first be reflected in exchange rates before transmitting to stock and bond valuations.

Practical Strong-Weak Currency Pairing: Trading Ideas for Shorting a Weak Euro and Going Long a Potential Yen

FX pairing is not limited to “long or short the US dollar”. A more efficient approach is to identify currencies with differences in both policy direction and economic direction for pairing. Two common frameworks:

- Shorting weak currencies (example: a weaker euro): when Europe’s economy weakens and policy also leans moderate, the euro may come under pressure against stronger currencies.

- Going long potential currencies (example: the yen’s safe-haven attribute): when global risks rise and capital seeks safety, the yen may be relatively resilient or even strengthen.

In practice, it is recommended to first divide FX strategies into two types of trades: trend trades and event trades. Trend trades focus on interest rate differentials and policy paths, while event trades specifically handle short-term volatility after central bank meetings and data releases. It is best to separate the position size and stop-loss range for these two types of trades. Otherwise, it is very easy for “short-term moves to shake out medium-term positions”.

If you also follow volatility in the renminbi and offshore renminbi and want to use a more technical approach for range-bound strategies, you can refer to: 2026 Offshore Renminbi Range-Bound Arbitrage Tutorial: Mastering the CNH and CNY Spread Code. The range and grid concepts inside are very helpful for building trading discipline that avoids chasing prices.

Asset Allocation and Safe-Haven Strategies amid Policy Uncertainty: Using Gold and Short-Term US Treasuries as a Protective Net

The most troublesome part of central bank policy divergence is that the market frequently shifts from “inflation trades” to “recession trades”, then back to “soft-landing trades”. If an investment portfolio only bets on a single scenario, it can easily be hit back and forth. A more practical approach is to divide asset allocation into a three-layer structure, so you do not have to guess the central bank’s next sentence every time.

| Layer |

Objective |

Common Tools |

| Core Layer |

Resist volatility and withstand drawdowns |

Short-term US Treasuries, investment-grade bonds, partial cash |

| Growth Layer |

Pursue long-term returns |

Global equities, sector ETFs (diversified) |

| Safe-Haven Layer |

Hedge event risk |

Gold, partial US dollar or yen exposure |

Defensive Stocks and High-Dividend ETFs: The “Cash Flow” Value of Asset Allocation Under Rate Cut Expectations

When rate cut expectations heat up, the market often focuses on the recovery in growth stock valuations. But do not overlook this: if the economy is actually cooling, defensive stocks and high-dividend ETFs are more like a “safe harbor for capital”. The reason is straightforward:

- Stable cash flow: when the economy pulls back, the market is more willing to pay a premium for stable dividends.

- Relatively controllable volatility: defensive sectors (such as utilities and consumer staples), usually experience smaller drawdowns.

However, high dividends are not a cure-all. If interest rates rise again or credit spreads widen, high-dividend assets may also correct as “bond-like” assets. Therefore, in an environment of central bank policy divergence, defensive allocation must be paired with interest rate sensitivity management to avoid buying the same type of risk too many times.

Keyword variation reminder: when the market swings between “rate cut expectations” and “inflation stickiness”, the advantage of a dividend strategy lies in providing a partially predictable source of returns, reducing your dependence on a single scenario.

How to Pair Gold and Short-Term US Treasuries: Resisting Liquidity Risk and Sudden Events

The combination of gold and short-term US Treasuries is often used to handle two different risks:

- Gold: tends to hedge geopolitical risks, fluctuations in financial confidence, and long-term monetary credit risk.

- Short-term US Treasuries: tend to hedge the need for capital parking when “risk assets fall sharply”, and are also less vulnerable to large fluctuations in long-term interest rates.

If you are an investor in Taiwan or Malaysia, you often encounter the practical issue that “most assets on hand are highly correlated with the US dollar” (US stocks, US Treasuries, US dollar deposits). In this case, the value of gold is not only safe-haven protection, but also the diversification of a single US dollar factor. However, it should also be noted that gold can also fluctuate in the short term, and the allocation ratio should be determined based on the investment horizon and risk tolerance, rather than chasing in and out based on one or two weeks of price movements.

If you also care about the impact of geopolitical risks on exchange rates (especially the tug-of-war between Asian currencies and safe-haven currencies), you can further read: The FX Impact of the Taiwan Strait Premium: Hong Kong Dollar and Renminbi Trends and Taiwan Strait Crisis Investment Strategies. Understanding the behavior of safe-haven assets from an event perspective will make it easier to connect FX investment strategies with asset allocation.

Further Reading (Highly Recommended)

Must-Read Japan Investment Risks: 5 Major Potential Risks Beyond Yen Depreciation You May Not Know

FAQ

What Is Central Bank Policy Divergence? How Does It Affect Me?

A: Central bank policy divergence refers to interest rates and monetary policy directions across countries moving out of sync. The most direct impact is on exchange rates and capital flows: capital will chase interest rate differentials and may also flow back into safe-haven currencies when risk rises, leading to greater FX volatility. At the same time, stock and bond valuations will be repriced according to the “interest rate path”, and asset allocation that is overly concentrated is more prone to drawdowns.

Should I Hold More Cash or Stocks During Policy Divergence?

A: The key is not choosing one or the other, but structure. Under policy divergence, a more robust approach is to divide the portfolio into a core layer (cash, short-term bonds, and other low-volatility assets), a growth layer (diversified stocks/ETFs), and a safe-haven layer (gold or partial exposure to safe-haven currencies). This way, even if rate cut expectations reverse, you do not need to make extreme decisions during periods of high volatility.

How Can FX Beginners Quickly Track the Latest Developments from Central Banks?

A: The most effective approach is to first focus on sources with “official original texts + fixed schedules”, such as the Federal Reserve’s FOMC calendar and statements: The Fed – Meeting calendars and information. Then build your own tracking table: interest rate decisions, inflation, employment, and central bank officials’ remarks. Beginners do not need to follow news every day, but should avoid being fully positioned and highly leveraged around major event dates.

Are Rate Cut Expectations Always Bullish for Stocks?

A: Not necessarily. If rate cuts come from “economic weakness” or risk events, stocks may fall first and then rise, or even only rebound without reversing. What matters is the reason behind the rate cuts and whether corporate earnings can hold up. In practice, defensive stocks and high-dividend ETFs can be paired with short-term US Treasuries and some gold to reduce dependence on a single scenario.

What Is the Most Common Pitfall in Carry Trades (Interest Rate Differential Trades)?

A: Treating “interest income” as a guaranteed profit while ignoring single-day FX volatility and leveraged drawdowns. Under central bank policy divergence, once risk appetite reverses, high-yielding currencies often give back gains quickly. Before entering carry trades, you should at least have rules for stop-losses, deleveraging, and position management around event dates, to avoid giving back months of interest income in just one or two days.

Conclusion

Central bank policy divergence is not short-term noise, but the “underlying setting” of the 2026 investment environment. To make asset allocation more stable in this environment, three principles are enough:

- Break down rate cut expectations into “interest rate differential trends + risk appetite”: do not chase news, trade the expectations gap.

- Manage drawdowns before discussing returns in FX investment strategies: carry trades need exit rules, and pair trades need to clearly distinguish between trend trades and event trades.

- Build a cross-asset safe-haven protection network: use short-term US Treasuries, partial cash, gold, and defensive dividend assets to reduce the damage from a single scenario going wrong.

When you translate “central bank policy” into executable position rules, you are less likely to be led by emotions no matter how much the market swings. What remains is to patiently wait for high-probability ranges to appear, then take action.