Evaluating the Success of a Foreign Exchange Intervention Requires a Comprehensive Assessment Across Short-Term, Medium-Term, and Long-Term Dimensions.

Dimension One: Short-Term Stability (Did It Successfully Contain Excessive Volatility?)

The primary objective of intervention is often not to reverse a trend immediately, but rather to restore order to a disorderly market. When an exchange rate experiences a rapid, one-sided decline disconnected from economic fundamentals, market panic can emerge and create a self-reinforcing downward spiral. In such situations, central bank intervention acts like an emergency brake on a rapidly falling elevator. Its main functions include:

- Countering speculative short positions: A sudden surge of official buying can inflict immediate losses on traders who are short the yen, forcing them to cover positions and providing support for the currency.

- Stabilizing market sentiment: Intervention sends a powerful message to the market: “Authorities are monitoring developments closely and possess both the ability and willingness to prevent the exchange rate from becoming disorderly.” This helps restore confidence and break the cycle of panic selling.

- Buying time: Intervention provides market participants and policymakers with a valuable opportunity to reassess conditions, reducing the risk of poor decisions driven by extreme emotions.

From this perspective, intervention often achieves immediate success by curbing excessive short-term volatility.

Dimension Two: Medium-Term Trend Impact (Did It Change Core Market Expectations?)

This represents a higher standard for evaluating whether an intervention truly “succeeded”. A genuinely effective intervention not only stabilizes current market conditions but also influences how market participants view the future direction of the exchange rate. If investors broadly believe that the intervention is temporary and that the fundamental drivers of depreciation (such as widening interest rate differentials) remain unchanged, the exchange rate is likely to resume its previous trend once intervention pressure fades. To alter a medium-term trend, intervention typically needs to be accompanied by at least one of the following conditions:

- A signal of policy change: Intervention serves as a precursor to future monetary policy adjustments (such as interest rate hikes).

- Coordinated international action: Multiple central banks intervene together, demonstrating greater commitment and credibility.

- Fundamental changes: The underlying economic factors driving depreciation begin to reverse, allowing intervention to reinforce an existing shift.

Without these supporting conditions, intervention through currency purchases and sales alone is rarely sufficient to reverse a medium-term trend driven by economic fundamentals.

Dimension Three: Long-Term Cost Effectiveness (What Is the Opportunity Cost of Using Foreign Exchange Reserves?)

Intervention is never cost-free. When a central bank sells US dollars and purchases yen, it consumes the country’s foreign exchange reserves. These reserves are a critical pillar of national financial stability, supporting imports, external debt obligations, and confidence in the financial system. As a result, any assessment of intervention effectiveness must include an evaluation of cost effectiveness:

- Opportunity cost: What alternative investment returns or strategic uses could have been generated by the trillions of yen spent on intervention? Is sacrificing those opportunities justified by the short-term stabilization achieved?

- National credibility: Frequent interventions that fail to produce lasting results may undermine international confidence in the country’s economy and currency.

- Limited resources: Foreign exchange reserves are not infinite. Excessive intervention may reveal the central bank’s limitations, and if markets begin to believe that authorities are “running out of resources”, speculative attacks could intensify.

Consequently, a successful intervention should achieve the greatest possible stabilization effect at the lowest possible cost while creating conditions that help address the underlying causes of exchange rate instability.

Further Reading (Highly Recommended)

A Complete Guide to Currency Appreciation and Depreciation: Understanding Exchange Rates and Their Impact on Prices in 5 Minutes

How to Reduce Investment Risk? Five Risk Management Strategies and Diversification Techniques in Practice

Quantitative Assessment of This Intervention: Was the Money Well Spent?

After understanding the evaluation framework, we can objectively analyze Japan’s record-breaking intervention. Although the full effect will require more time to observe, we can make an initial assessment based on several key indicators.

“How Much Time Was Bought”: An Analysis of the Sustainability of Exchange Rate Stability After the Intervention

From the perspective of short-term stability, this intervention was undoubtedly successful. After news of the intervention emerged, USD/JPY quickly retreated from its highs, and volatility declined significantly, preventing the situation from spiraling out of control. However, the key question is how long this stability can last. Market data shows that in the weeks following the intervention, the yen exchange rate became more stable, but depreciation pressure was not completely eliminated. This indicates that the intervention successfully “bought time”, but did not eliminate the underlying problem.

“How Much Did Expectations Change”: Changes in the Options Market Risk Reversal Indicator

To measure shifts in market expectations, investors can observe the “Risk Reversal indicator” in the foreign exchange options market. This indicator reflects the relative demand for options betting on future currency appreciation (call options) versus depreciation (put options). Before the intervention, the indicator showed that the market was extremely bearish on the yen. After the intervention, bearish sentiment eased but did not reverse into bullishness. This means the market acknowledged the short-term power of intervention, but remained cautious about the yen’s medium-term outlook.

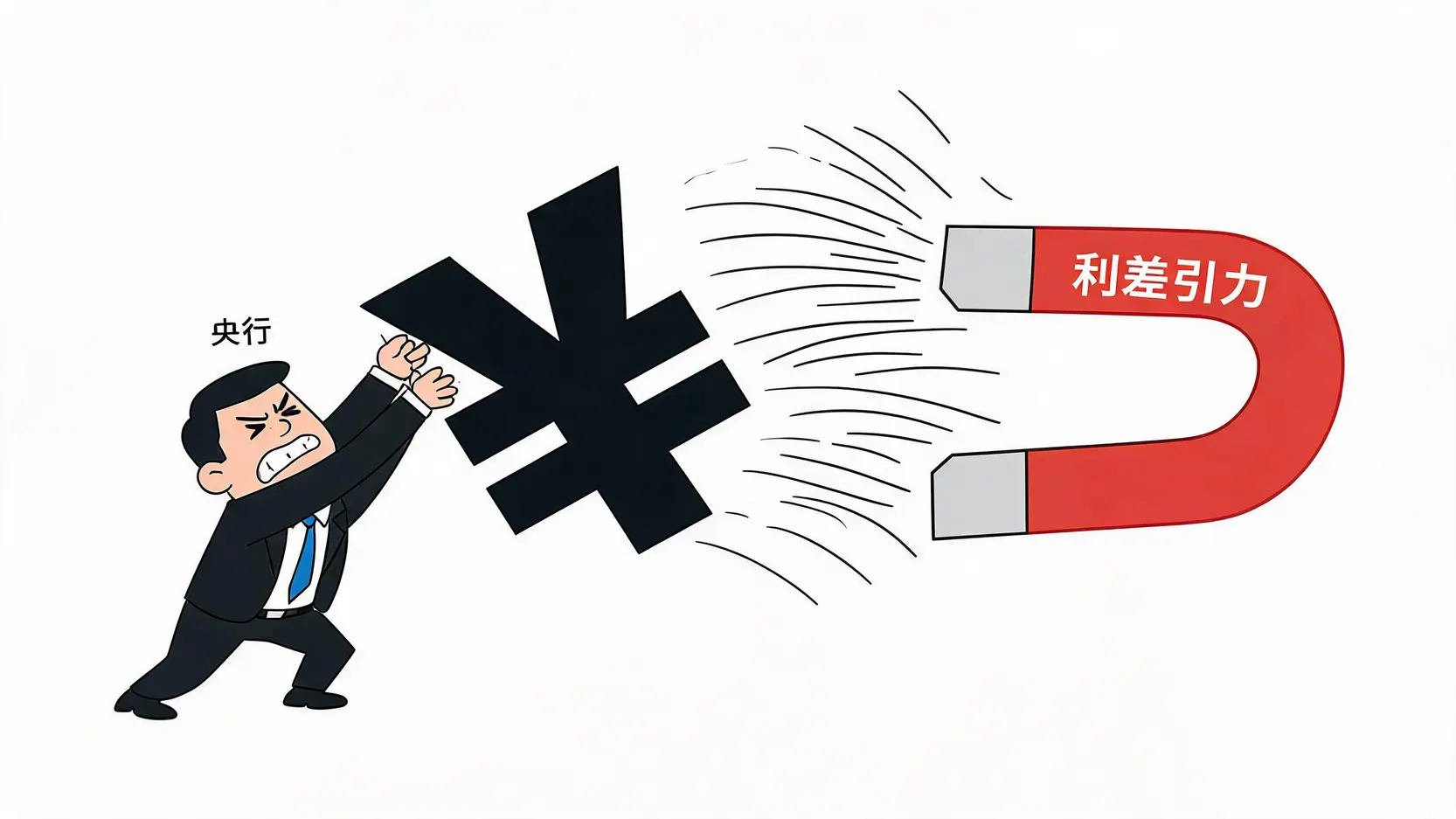

Degree of Divergence From Fundamentals: Can Intervention Fight the Gravitational Pull of Interest Rate Differentials?

The core force currently driving yen depreciation is the large gap between the monetary policies of Japan and the US. The US Federal Reserve has maintained high interest rates to fight inflation, while the Bank of Japan continues to uphold its ultra-loose monetary policy. This large interest rate differential keeps capital flowing from Japan to the US and represents the fundamental “gravitational pull” behind yen depreciation.

Japan’s unilateral intervention is essentially an attempt to use administrative force to resist the market’s underlying trend. Historical experience shows that without accompanying monetary policy adjustments (namely a narrowing of the interest rate differential), the effects of any intervention are likely to be temporary. Capital’s pursuit of returns will ultimately overpower the force of intervention, and the exchange rate will eventually return to fundamentals.