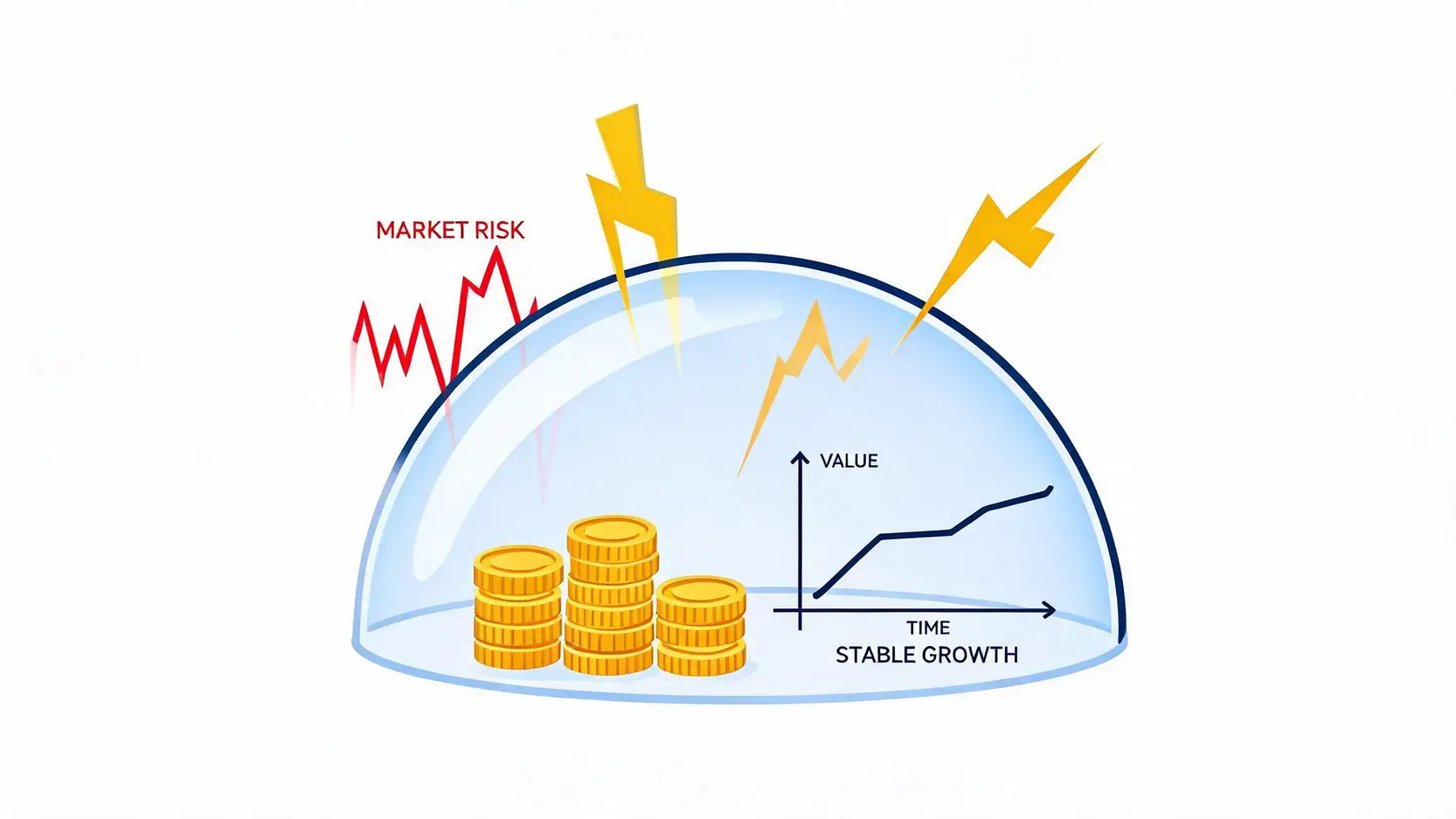

Risk Hedging Protection Mechanisms During Extreme Market Volatility

Using Non-Deliverable Forward Contracts (NDFs) to Lock in Arbitrage Profits

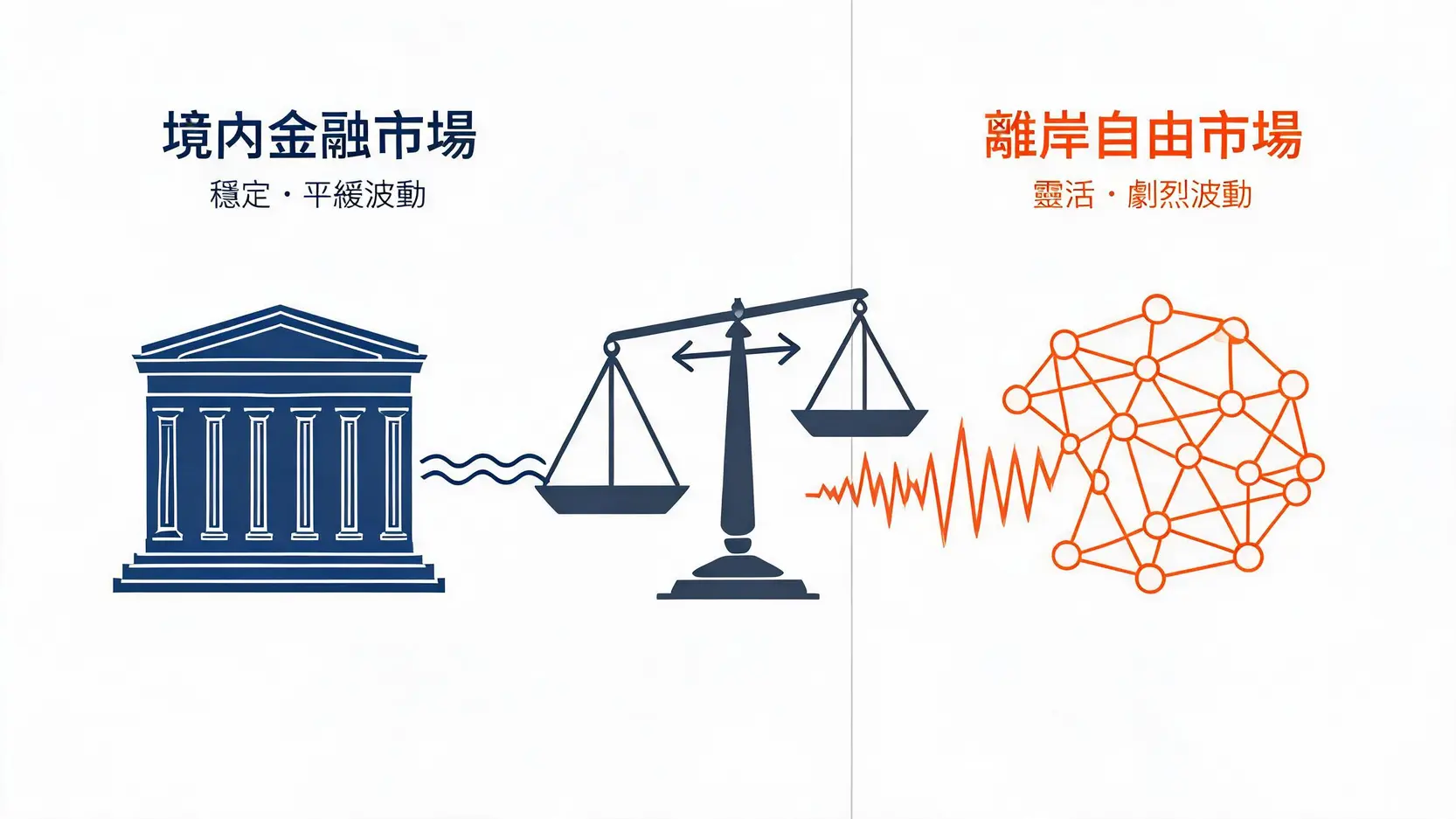

Beyond options, Non-Deliverable Forwards (NDFs) represent one of the most powerful tools available to institutions for managing two-way volatility. Because onshore Renminbi remains subject to strict capital controls, foreign corporations and offshore institutional investors cannot easily conduct large-scale spot market hedging within mainland China. In such situations, NDFs, which trade entirely in offshore markets and settle in US dollars through cash differences, become an irreplaceable investment instrument.

By trading NDF contracts, investors can lock in future exchange rates at a specific point in time. When highly attractive spreads emerge between onshore and offshore Renminbi markets, investors can simultaneously establish offsetting NDF positions in the forward market to eliminate future exchange rate exposure. This not only significantly improves capital efficiency but also transforms what would otherwise be directional speculation into genuine low-risk or near risk-free arbitrage.

Recent authoritative market coverage, including reports from Economic Daily News indicating that both offshore and onshore Renminbi exchange rates have strengthened simultaneously with accelerating appreciation, further demonstrates that under certain macroeconomic conditions, Renminbi exchange rates can display strong resilience and linkage effects. This reinforces the importance of foreign exchange traders monitoring both markets simultaneously.

Further Reading (Highly Recommended)

Renminbi Exchange Rate Forecast: Central Bank Tightens Offshore Liquidity, Complete Analysis of Appreciation and Depreciation Trends

Complete Guide to Onshore and Offshore Renminbi Spread Arbitrage: From CNY and CNH Fundamentals to Risk Management

Frequently Asked Questions: Offshore Renminbi Two-Way Volatility Arbitrage FAQ

Q: Can ordinary retail investors personally execute risk-free arbitrage between offshore and onshore Renminbi markets?

A: In theory, the logic is the same, but in practice, execution is extremely difficult. Onshore Renminbi (CNY) is subject to strict cross-border capital controls, making it difficult for overseas retail investors to freely open domestic bank accounts and conduct large-scale real-time fund transfers. Most retail investors and independent traders typically focus on two-way volatility trading within the offshore Renminbi (CNH) market through regulated foreign exchange margin trading platforms, or indirectly participate in spread hedging strategies through exchange rate ETFs and related derivatives.

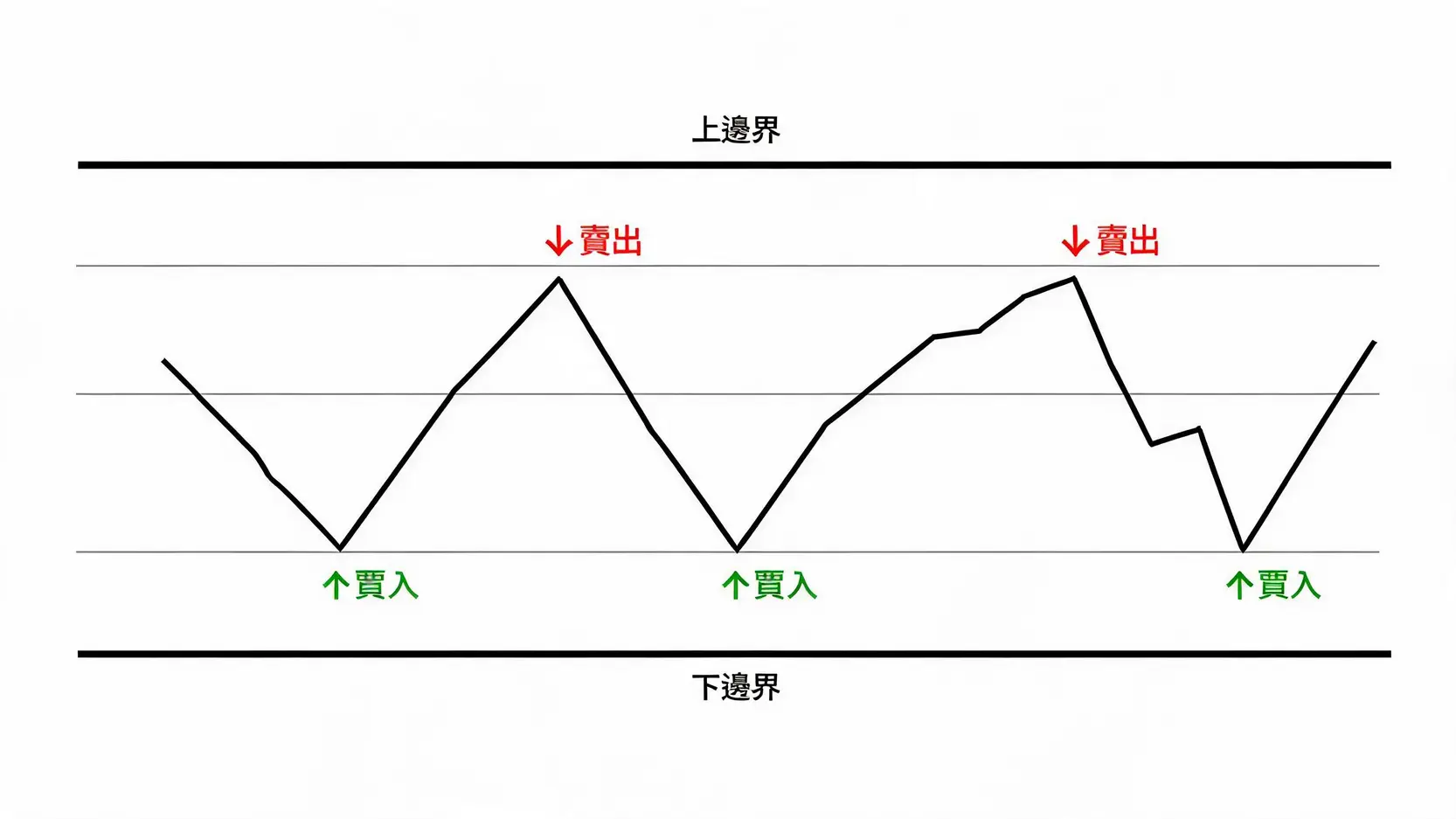

Q: What is the biggest potential risk of a range-bound arbitrage strategy?

A: The most critical risk of this strategy is a “genuine breakout from the trading range”. When structural changes occur in the global macroeconomic and political environment (such as the outbreak of a major geopolitical conflict or the implementation of unexpectedly aggressive monetary easing policies by major central banks) exchange rates may completely break out of their previous equilibrium range and develop into a powerful one-way trend. If arbitrage traders fail to establish strict stop-loss levels or lack effective options hedging mechanisms, they may face substantial unrealized losses or even the risk of liquidation.

Q: How can investors accurately track the real-time impact of the US Dollar Index on Renminbi spreads?

A: The US Dollar Index (DXY) has always served as a key benchmark and directional indicator for the global foreign exchange market. Investors can monitor DXY movements in real time through professional financial terminals (such as Bloomberg and Reuters) or through major financial information websites. As a general rule, when the US Dollar Index rises strongly due to safe-haven demand or expectations of higher interest rates, the more market-driven offshore Renminbi typically depreciates first, rapidly widening the spread relative to the regulated onshore market. The opposite is also true. Overlaying DXY price charts with CNH/CNY spread charts for detailed comparative analysis is a standard operating procedure used by experienced traders to identify high-probability entry opportunities.

Q: Is grid trading still suitable in the volatile foreign exchange environment of 2026?

A: Absolutely. In fact, it may be more effective than ever. The reason is that the 2026 market environment is filled with complex policy variables and conflicting bullish and bearish expectations, making it difficult for exchange rates to sustain long-term one-way trends. Instead, short-term sharp fluctuations and repeated market reversals have become increasingly common. These characteristics of a clearly two-way volatility market create the ideal environment for grid trading strategies to capitalize on their “buy low, sell high” advantages. As long as investors remain disciplined and properly manage overall capital allocation and grid density, they can steadily accumulate meaningful returns amid market volatility.

Conclusion: Finding Stable Spread Returns Amid Two-Way Renminbi Volatility

In summary, successfully executing offshore Renminbi range-bound arbitrage over the long term requires not only a high degree of sensitivity to global macroeconomic developments and central bank policy boundaries, but also trading discipline as precise and consistent as a machine. The recurring expansion and convergence of spreads between onshore and offshore Renminbi vividly reflect the ongoing struggle between market greed and fear, as well as the powerful forces of cross-border liquidity flows.

As professional foreign exchange investors pursuing absolute returns, we should not fear market volatility. Instead, we should view every episode of two-way volatility as a valuable source of profit opportunities. By defining precise and statistically meaningful trading ranges, applying grid trading strategies in a flexible yet disciplined manner, and decisively activating powerful defensive mechanisms such as spread hedging and forward foreign exchange contracts when extreme market conditions threaten, you can confidently unlock your own profit formula within the unpredictable two-way volatility environment of 2026 and achieve steady asset growth under controlled risk conditions.