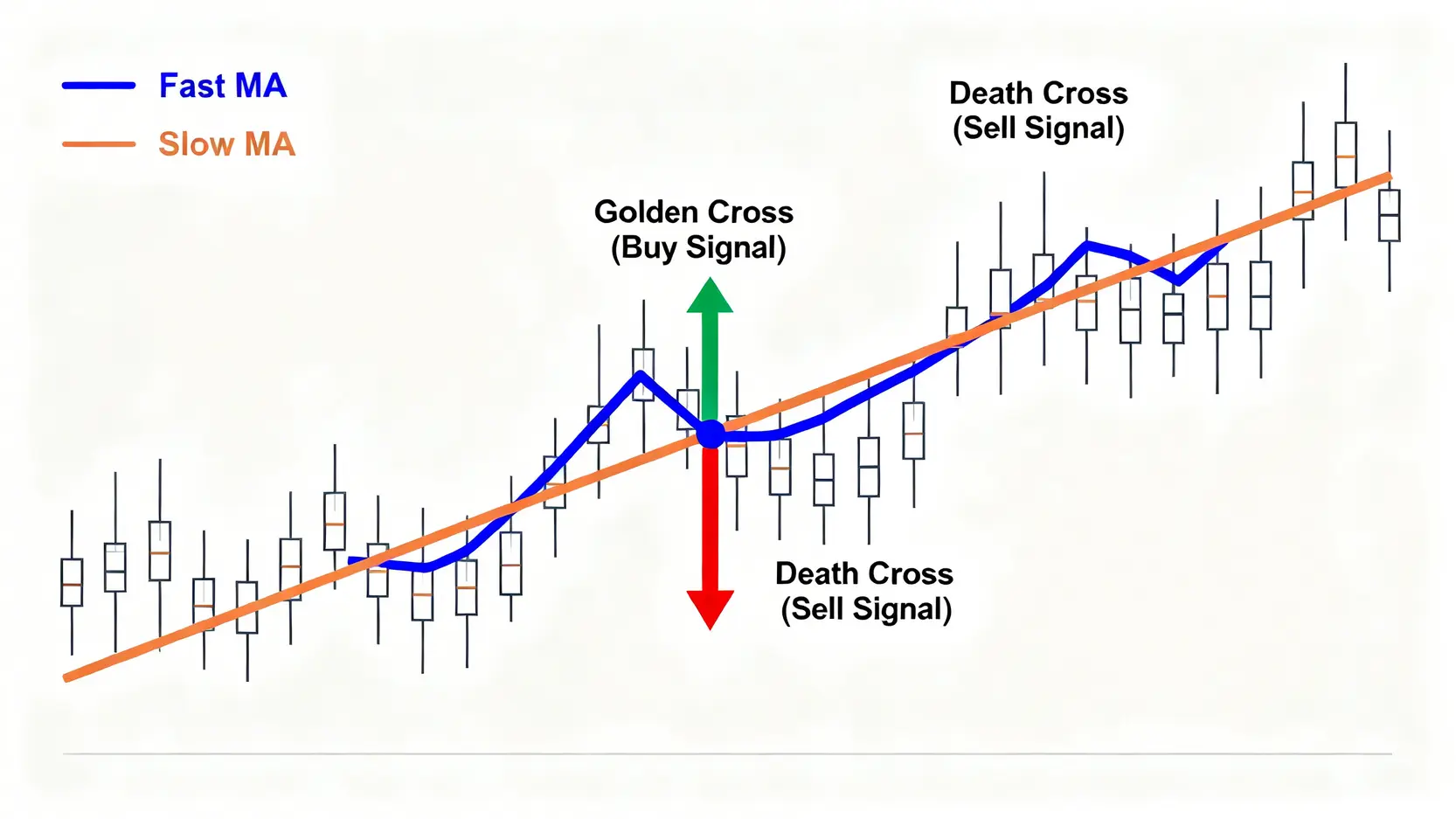

Moving Average Strategy: Golden Cross and Death Cross

We use Python to calculate these two moving averages:

# Calculate the 10-day and 30-day moving averages

df[‘MA10’] = df[‘Close’].rolling(window=10).mean()

df[‘MA30’] = df[‘Close’].rolling(window=30).mean()

# Display the most recent rows of data to observe the calculation results

print(df.tail())

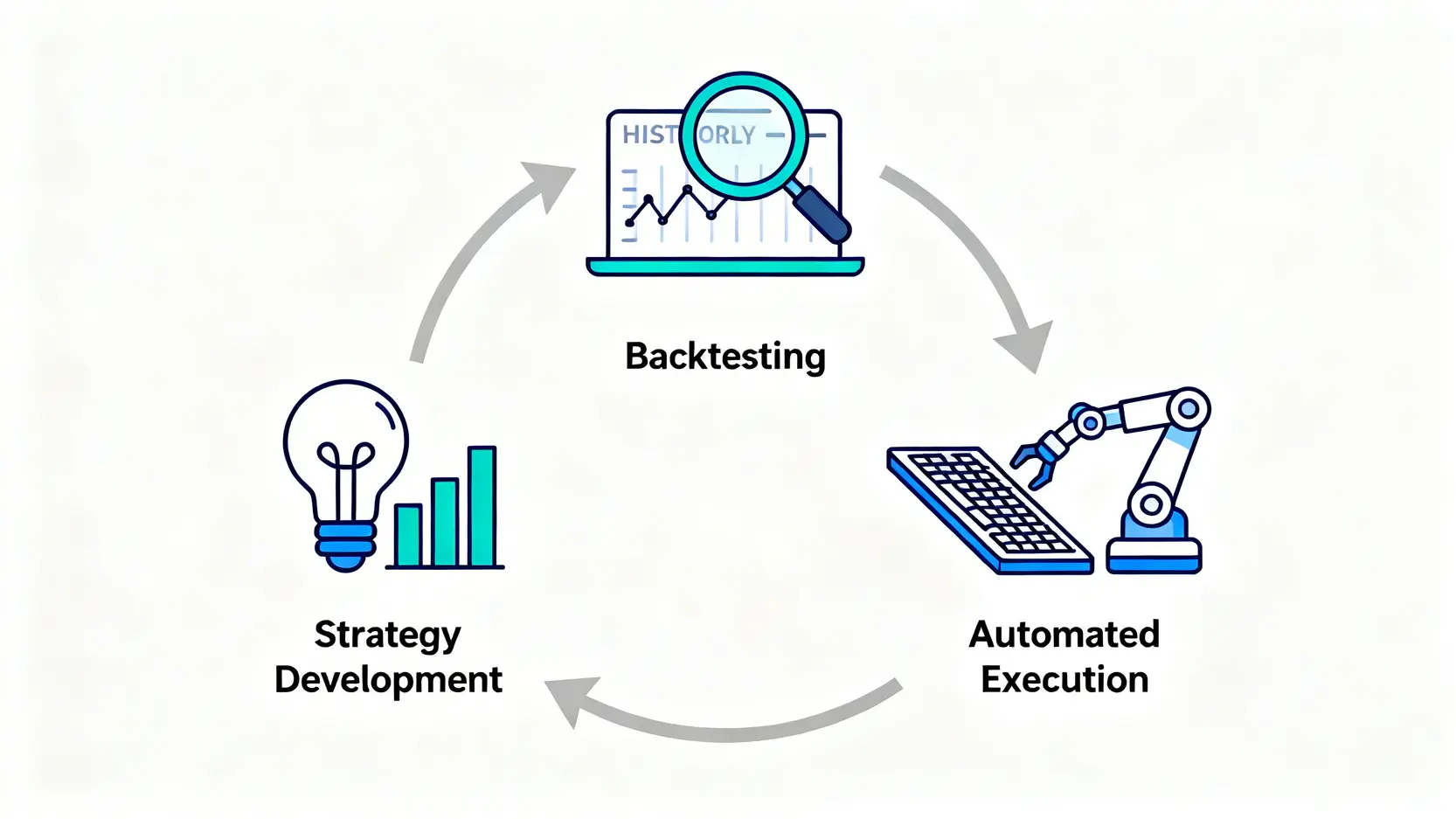

Step 4: Run a Strategy Backtest (Validate Your Idea with Historical Data)

No matter how good a strategy may seem, it must be tested against historical data. Backtesting is the process of simulating trades using past data to see how the strategy would have performed. A simple backtesting process is as follows:

- Generate signals: Go through the data and record a buy signal when a golden cross occurs, and a sell signal when a death cross occurs.

- Simulate trading: Carry out simulated buys and sells based on the signals, and calculate the profit or loss of each trade.

- Evaluate performance: Measure key indicators such as total return, win rate, and maximum drawdown (MDD).

Although a complete backtesting program is relatively complex, its core principle is to objectively evaluate the feasibility of a strategy. Through backtesting, you may find that your original idea is not actually viable in the real market, which can help you avoid paying expensive tuition in live trading.

Step 5: Connect Automated Trading (How to Connect to a Broker API for Live Execution)

When your strategy performs well in backtesting, the final step is to automate it. This is done through a “broker API (Application Programming Interface)”.

An API acts as the bridge between your program and the broker’s order execution system. Your program can send instructions through the API, such as “buy one lot of TSMC at market price”, and the broker’s system will execute the order once it receives the instruction. Many overseas futures and forex brokers, as well as local securities brokers, provide API services, allowing investors to connect their own trading systems to the market and achieve true 24-hour automated trading.

Further Reading (Highly Recommended)

What Is an MT4 EA? Beginner’s Guide: From Automated Trading to Installation and Backtesting Tutorials

Python Quantitative Trading FAQ

I have no programming experience at all. Can I learn Python quantitative trading?

Absolutely. Python is widely recognized as one of the most beginner-friendly programming languages. At the beginning, you can start by imitating and modifying open-source strategy examples available online, focusing on understanding the underlying trading logic. Once you become familiar with the basic syntax, you can gradually try writing your own strategies. The process of learning quantitative trading is also the process of improving your programming skills.

Can quantitative trading guarantee profits? What common risks should I be aware of?

Quantitative trading does not guarantee profits. Its biggest risk comes from “strategy failure”. Common risks include:

- Overfitting: The strategy performs exceptionally well during backtesting, but it is merely overfitting the noise in historical data and performs poorly in live trading.

- Changes in market structure: Previously effective patterns may become invalid due to regulatory changes, black swan events, or other factors.

- Technical risks: Program bugs, network interruptions, API failures, and similar issues may lead to unexpected losses.

Therefore, continuously monitoring strategy performance and establishing a comprehensive risk management framework is crucial.

What financial knowledge is required before learning Python quantitative trading?

Having basic financial knowledge will make your learning process more efficient. It is recommended to understand at least:

- Basic market operations: Understand the trading rules of different instruments such as stocks, futures, and forex.

- Technical analysis indicators: Be familiar with commonly used indicators such as Moving Average (MA), Relative Strength Index (RSI), and Bollinger Bands, including their meaning and applications.

- Risk management concepts: Understand basic risk control principles such as stop-loss, capital management, and position sizing.

Programming is a tool, but financial knowledge is the core factor that determines the effectiveness of a strategy.

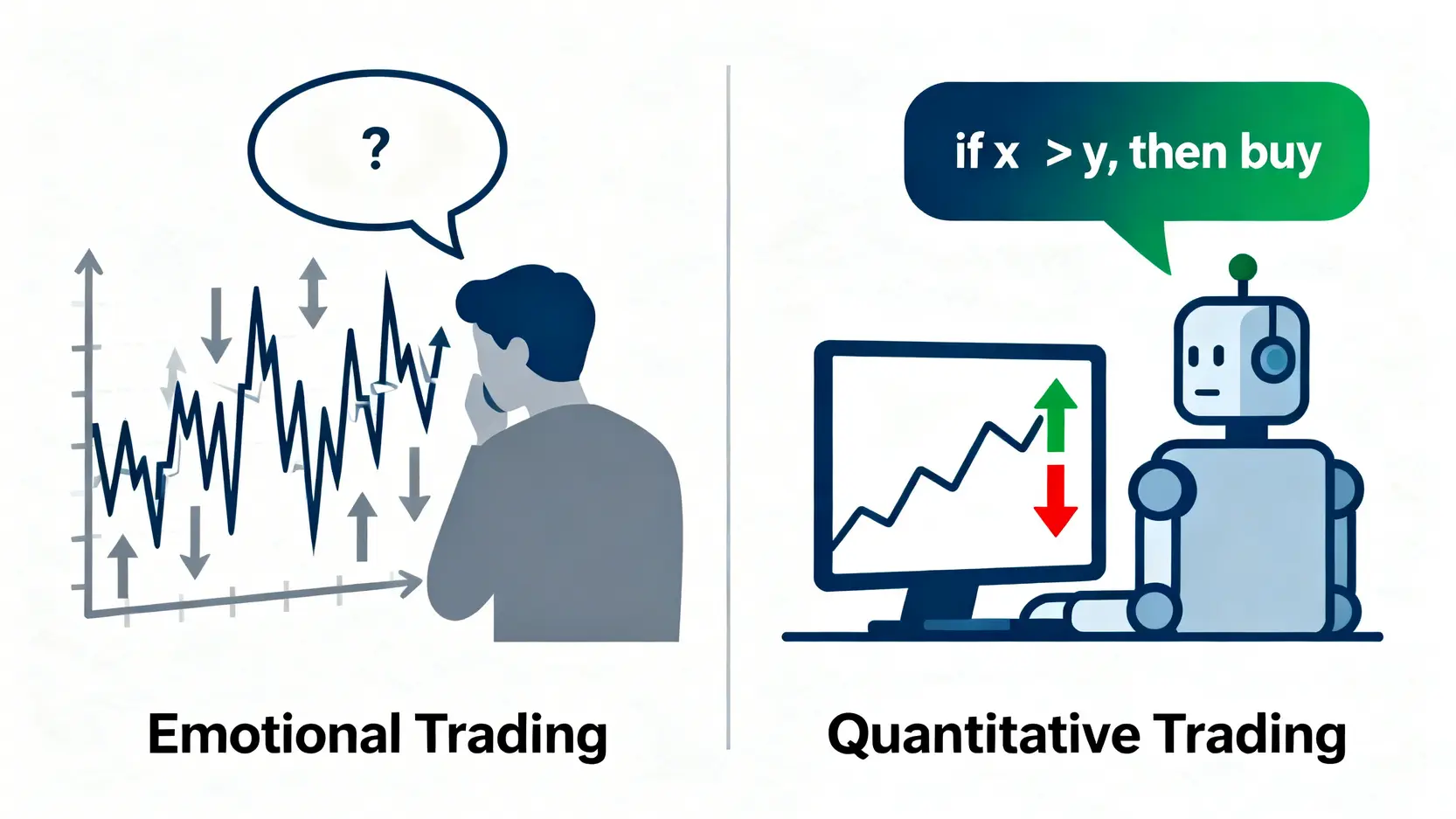

Conclusion

Congratulations! By following this Python quantitative trading tutorial, you have mastered the complete beginner workflow, from concepts and environment setup to strategy backtesting. Quantitative trading is not an unreachable technology, but a powerful methodology that helps you conduct scientific and disciplined investing. Its greatest value lies in forcing you to transform vague market “feelings” into clear and verifiable “rules”. Now is the time to put it into practice, begin your journey into quantitative trading programs, and take the first step toward rational investing!