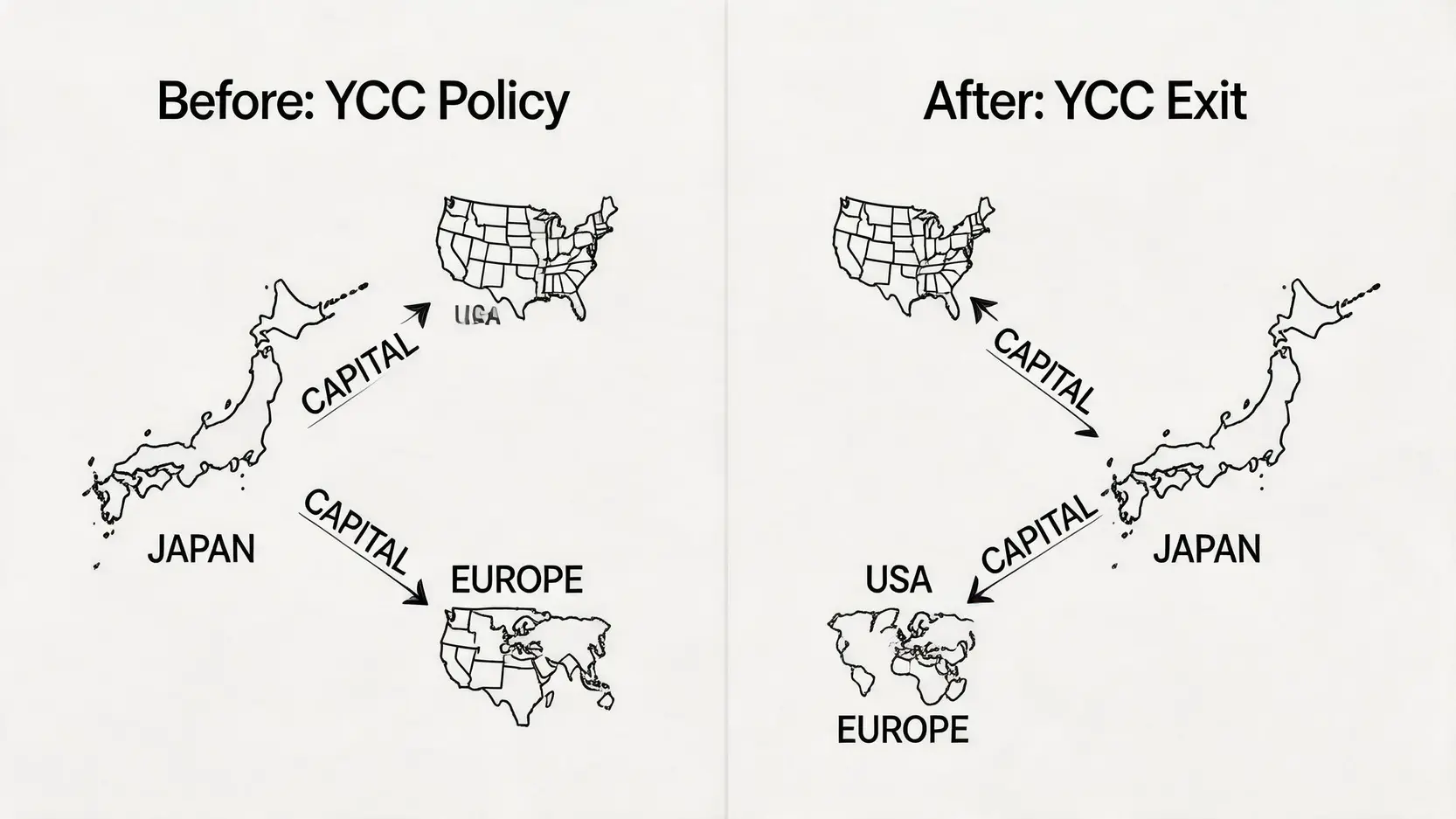

Global Ripple Effects of YCC Exit: Yen Capital May “Return Home” From Overseas

- Global liquidity tightening: Large-scale capital may be withdrawn from US and European markets, potentially pushing up borrowing costs in those economies.

- Pressure on high-risk assets: Global risk appetite may decline, putting pressure on high-valuation assets such as technology stocks.

- “Carry trade” unwinding: The widely used strategy of borrowing low-interest yen to invest in higher-yielding currencies “carry trade” may reverse, triggering significant volatility in related currency pairs.

Bank of Japan Interest Rate Timeline and Future Path Forecast

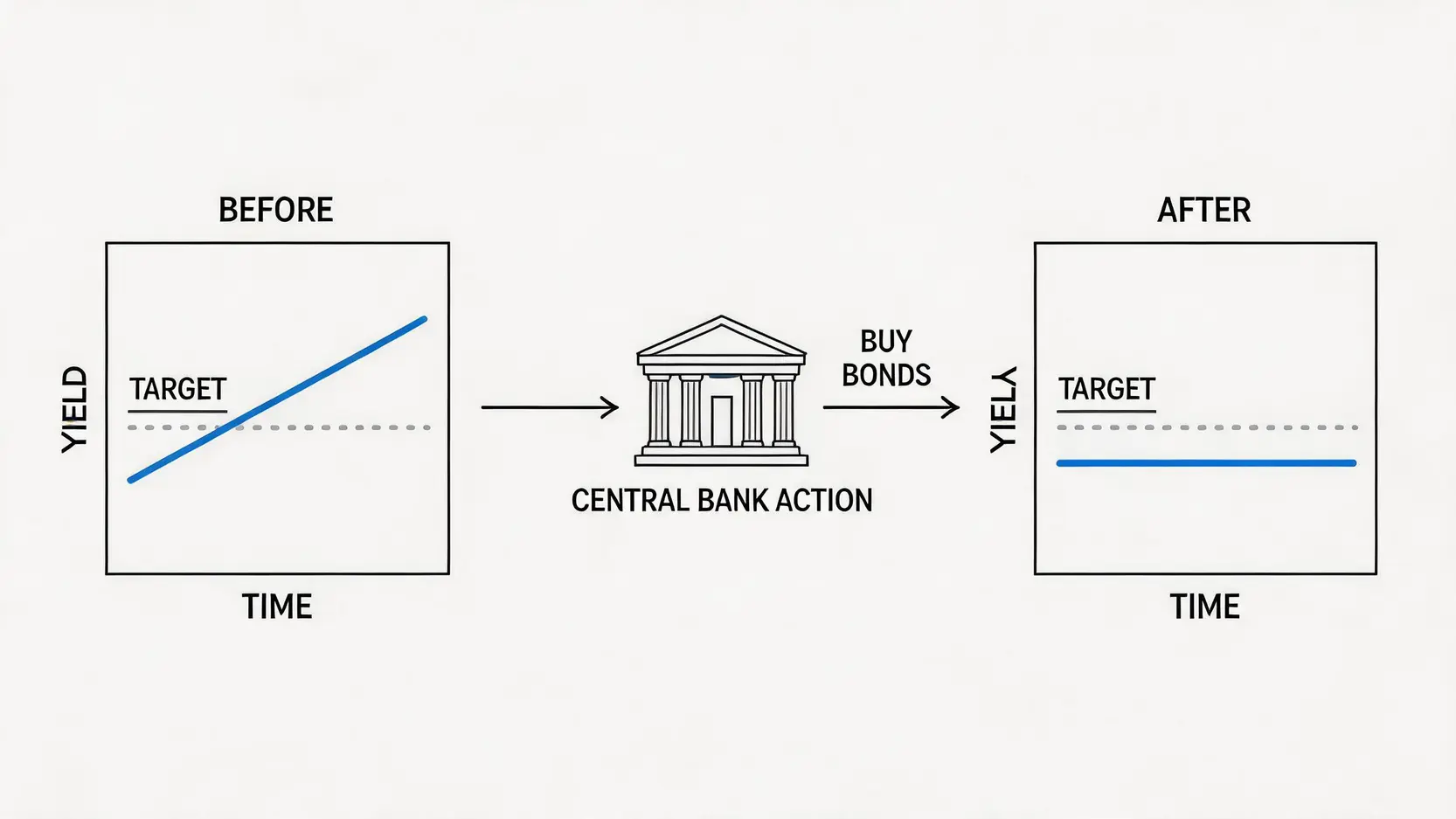

Ending YCC is only the first step toward monetary policy normalization. The market’s focus has now shifted to the next question: When will the Bank of Japan raise interest rates again, and how fast will the pace be?

Further reading (Highly recommended)

Overseas Stock Investment Guide: From Asset Stocks and Gold Concept Stocks to Japan Tesla Analysis…

USD to TWD Exchange Rate Explained: A Complete Guide to Yen Trends and RMB Conversion

2026 Bank of Japan Monetary Policy Meeting Schedule Overview

To help investors track key timing points, below is the expected 2026 Bank of Japan monetary policy meeting schedule. Statements and the governor’s press conferences following each meeting remain key focus events for the market.

| Meeting Month |

Expected Date |

Key Focus

|

| January |

20–21 |

Early-year economic outlook and inflation assessment |

| March |

17–18 |

Evaluation of spring wage negotiations results |

| April |

27–28 |

Quarterly economic and price outlook report |

| June |

12–13 |

Mid-year policy review |

| July |

28–29 |

Quarterly economic and price outlook report |

| September |

21–22 |

Assessment of summer economic data |

| October |

27–28 |

Quarterly economic and price outlook report |

| December |

18–19 |

Year-end policy assessment and outlook for the coming year |

Market Expectations: When Will the Next Rate Hike Be, and How Large Will It Be?

The current mainstream view in the market is that the Bank of Japan will adopt an extremely cautious “small steps, slow pace” strategy. After the first rate hike, the central bank is expected to spend several months observing economic data to confirm the stability of wage growth and inflation before considering the next move.

- Timing forecast: If economic data remains stable, the market generally expects the next rate hike to occur in the third or fourth quarter of 2026.

- Magnitude forecast: Each rate hike is expected to be 25 basis points (0.25%), raising the policy rate from the current 0–0.1% range to 0.25%, and then gradually moving toward 0.5%.

Everything depends on data. Any signs of economic slowdown or easing inflation could lead the Bank of Japan to delay its rate hike timeline.

Long-Term Interest Rate Normalization Challenges and Investment Outlook

The Bank of Japan is walking a tightrope. On one hand, it must control inflation and return interest rates to normal levels. On the other hand, it must avoid tightening too quickly, which could burst asset bubbles or severely damage the heavily indebted government’s fiscal position.

For investors, this means market volatility will become the new normal. The simple strategy of betting on yen depreciation and Japanese stock gains is over. In the future, investors who can adapt to interest rate changes and deeply analyze structural shifts in Japan’s domestic economy will be the ones who find opportunities in this new era.

Frequently Asked Questions (FAQ)

Q: Will traveling to Japan become more expensive after YCC ends?

A: In the medium to long term, if the yen strengthens due to rate hike expectations, you will be able to exchange fewer yen for the same amount of foreign currency, which means travel costs such as transportation, accommodation, and shopping in Japan may become more expensive. However, exchange rates fluctuate significantly in the short term, so immediate increases are not guaranteed. It is advisable to monitor exchange rates before traveling.

Q: Is now a good time to buy Japanese yen?

A: It depends on your objective. If you are buying for travel or practical needs, you may consider accumulating yen in batches at relatively favorable exchange rates. If it is for investment purposes, although there is long-term appreciation potential, short-term movements are still highly influenced by the Bank of Japan’s tightening pace and global economic conditions, so risks remain elevated and caution is required.

Q: Should I sell my Japanese stock funds now?

A: Not necessarily. The impact of YCC adjustment on Japanese equities is “short-term negative, long-term positive”. In the short term, yen appreciation may pressure export companies, but in the long term, monetary normalization supports overall economic fundamentals. It is recommended to review your fund holdings. If exposure is mainly in domestic demand sectors such as financials and retail, the outlook remains positive. If heavily weighted toward export-oriented companies, their ability to manage currency risk should be assessed.

Q: How will Bank of Japan rate hikes affect mortgage rates?

A: The policy rate set by the Bank of Japan serves as a benchmark for short-term interest rates, while mortgage rates (especially fixed-rate mortgages) are more closely tied to long-term yields such as the 10-year government bond yield. As YCC ends and rates gradually rise, long-term yields are expected to increase moderately, which will gradually push up domestic mortgage rates in Japan.

Conclusion

In summary, the Bank of Japan’s exit from the YCC policy and the start of an interest rate hike cycle mark a major step toward monetary policy normalization and the end of an era. The impact of this YCC policy adjustment is profound, reshaping everything from the yen exchange rate to global capital flows. Whether in forex, equities, or bond markets, investors should closely monitor the Bank of Japan’s interest rate timeline and continuously reassess their asset allocation strategies to navigate volatility and capture emerging opportunities in this new environment.