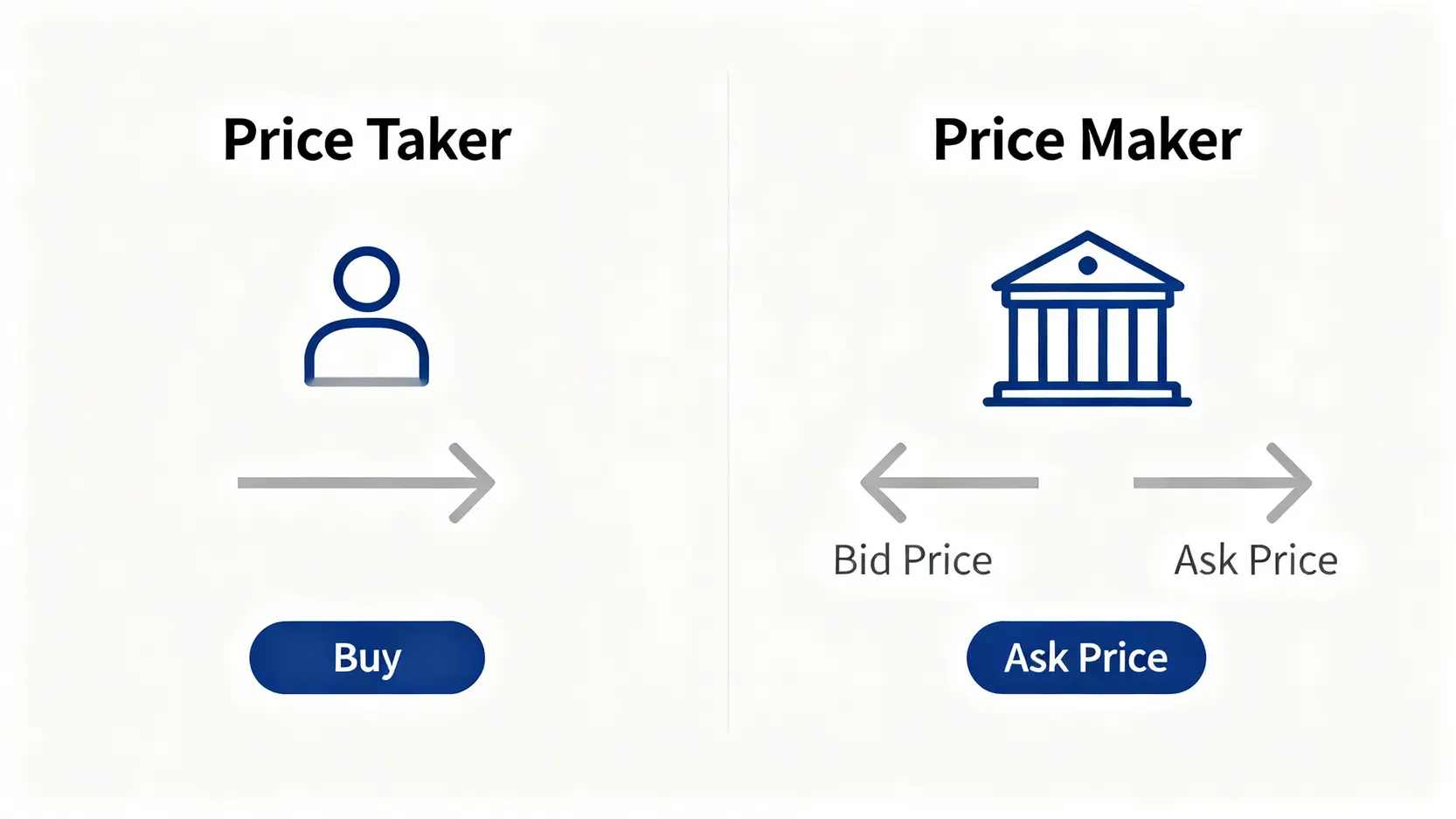

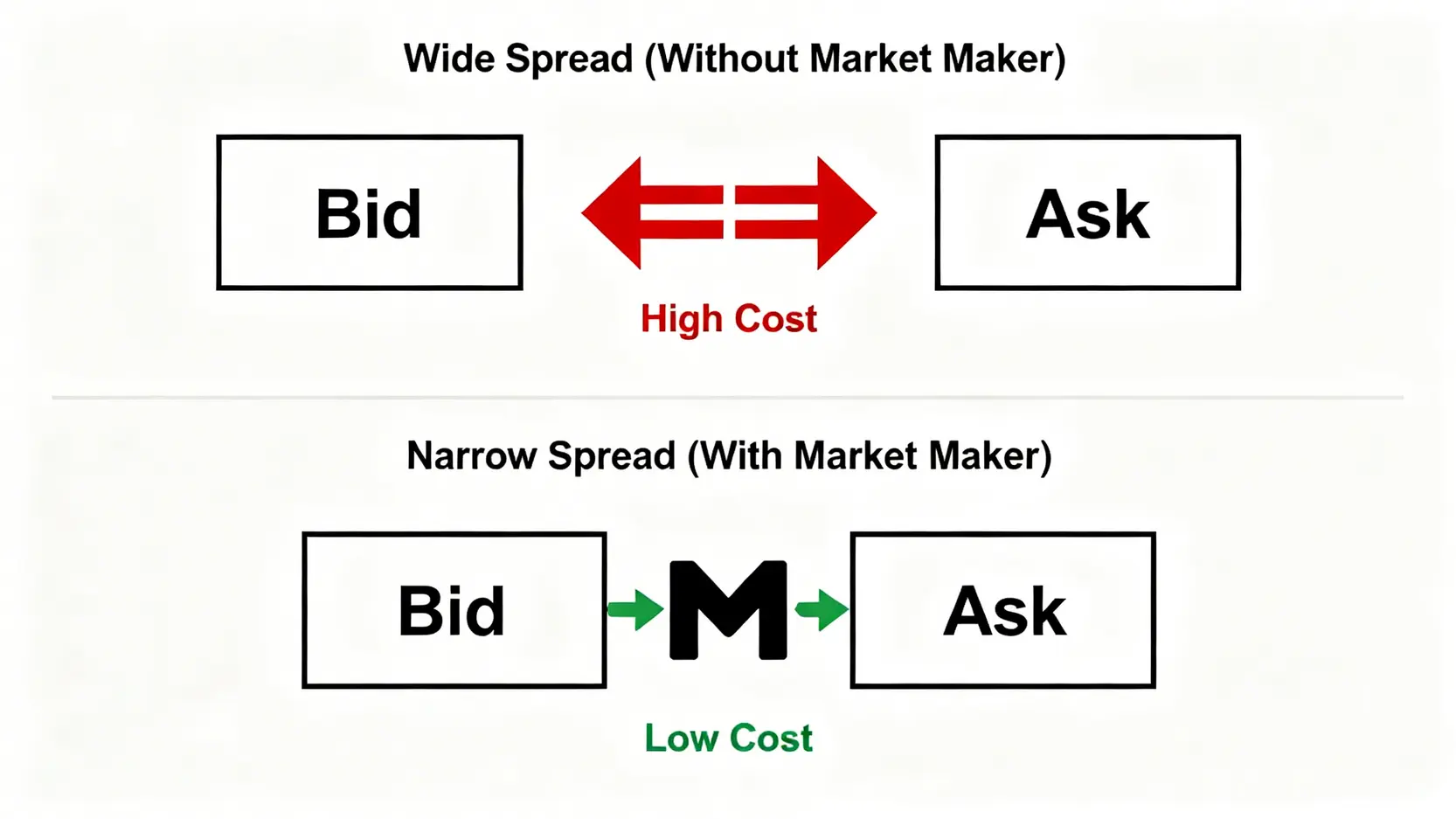

By providing continuous quotes, market makers effectively narrow the bid-ask spread and reduce investors’ trading costs.

Further Reading (Highly Recommended)

What Is the S&P500? Beginner Investment Guide: Understanding Components, ETFs, and How to Buy

US Stock Options Guide 2025: Understanding Options in One Article, From Opening a Firstrade Account to Four Major Trading Strategies

Core Responsibilities of HKEX Market Makers (Market Maker Obligation Hong Kong)

In Hong Kong, becoming an HKEX-approved market maker is not easy. Institutions must undertake a series of strict legal and contractual responsibilities collectively known as “Market Maker Obligation”. These responsibilities ensure that market makers truly contribute to the market rather than simply engaging in speculation.

Continuous Quoting Responsibility: Key “Dealer Quoting Hours” and Frequency Requirements

This is the most critical responsibility of a market maker. They cannot quote prices or leave the market at will. HKEX has clear rules regarding this.

- Quoting hours: Market makers must continuously provide two-sided quotes during the “dealer quoting hours” specified by the exchange. This period usually covers most of the trading session, for example from five minutes after market open until market close.

- Quoting frequency: During this period, market makers must maintain their quotes in the market for more than a certain percentage of time, such as 95 percent or higher. This means they cannot withdraw orders or remain offline for long periods.

- Quote size: Quotes must not only exist but must also reach a certain minimum quote size, ensuring that a certain level of trading demand can be met.

These strict time and frequency requirements ensure that the market always maintains basic liquidity and form the foundation of fulfilling “market maker responsibility”.

Maintaining a Reasonable Spread: Ensuring Fair Trading in the Market

If a market maker posts an excessively large bid-ask spread, for example if a stock priced at 10 dollars has a bid of 9 dollars and an ask of 11 dollars, such “liquidity” becomes meaningless to investors because the trading cost is extremely high. Therefore HKEX requires market maker quotes to remain within a “reasonable spread” range.

- Maximum spread limit: The exchange sets a maximum allowable spread for different products. Market maker quotes cannot exceed this limit.

- Price linkage: Market maker quotes must closely follow the actual market transaction price or the underlying asset price movement and cannot deviate from the market.

This obligation ensures that the liquidity provided by market makers is of “high quality”, truly reducing investors’ transaction costs and maintaining fairness in the market.

Differences in Responsibilities for Different Financial Products (such as ETFs, options, and derivatives)

For different types of financial products, HKEX market maker requirements also differ because their characteristics and complexity vary:

| Financial Product Type |

Core Market Maker Responsibility |

Challenges and Difficulties

|

| Equity Index ETF |

Ensure That the Market Trading Price of the ETF Closely Tracks Its Net Asset Value (NAV), Preventing Significant Discounts or Premiums. |

Need to Monitor the Price Movements of a Basket of Component Stocks in Real Time and Efficiently Conduct Creation and Redemption Operations to Manage Inventory.

|

| Stock Options |

Provide Continuous Two-Sided Quotes for Option Contracts With Different Expiry Dates and Different Strike Prices. |

Involves Complex Pricing Models (Such as the Black-Scholes Model) and Risk Hedging (Greeks), With Extremely High Requirements for Computing Capability and Risk Management. |

| Derivative Warrants / Callable Bull Bear Contracts |

Provide Liquidity and Ensure That Prices Reflect the Price Movements of the Underlying Assets and the Intrinsic Value of the Product. |

High Leverage Effects and Intense Price Volatility Pose Significant Challenges to the Reaction Speed and Risk Control of Market Makers.

|

How to Become an HKEX-Approved Market Maker? Qualification Requirements and Application Process

Becoming a dealer on HKEX has an extremely high threshold. This is not only a test of capital strength but also a comprehensive review of technology, risk control, and professional capability. This ensures that only the most reliable institutions can undertake this critical market responsibility.

Capital and Financial Requirements: The Basic Threshold to Become a Dealer

This is the most rigid indicator. Market makers must use their own capital to bear market risk and maintain inventory, therefore they must possess strong capital strength.

- Minimum capital requirement: HKEX requires applicant institutions to maintain a certain minimum level of paid-up capital and liquid funds to ensure sufficient risk resistance capability.

- Stable financial record: applicants must submit detailed financial reports to demonstrate sustainable profitability and a healthy financial structure.

Technology and System Requirements: Essential Trading Infrastructure

Modern market making operations rely heavily on technology. Manual quoting has long become history, replaced by complex algorithms and high-speed trading systems.

- Low-latency trading systems: Quoting speed is measured in milliseconds or even microseconds. Market makers must possess top-level technical infrastructure capable of rapidly receiving market data, executing algorithms, and sending orders to the exchange.

- Strict risk management systems: The system must be able to calculate position risk in real time, monitor risk exposure, and automatically trigger risk control measures when extreme market volatility occurs (such as widening the spread or reducing quote size).

- Reliable exchange connectivity: Institutions must maintain stable and high-speed dedicated connections to the HKEX trading system to ensure smooth execution of quotes and trading instructions.

Overview of the HKEX Application and Approval Process

The entire process is rigorous and lengthy and usually includes the following steps.