【2026 Hong Kong US Bond Quick Guide】Comparison of 3 Major Methods and Complete Guide to US Bond Yields

In the current environment of global economic volatility, many Hong Kong investors are seeking assets that are more stable than stocks. Considered one of the safest assets globally, “US Bonds”have become a popular choice, especially when their yields are attractive. However, for beginners, questions such as “What are the methods tobuy US bonds in Hong Kong?” and “What exactly is bond yield?” can often be discouraging. This article provides a one-stop guide, explaining US bond concepts from scratch and comparing various purchase channels in Hong Kong in detail, helping you take your first step into investing in US Treasury bonds with ease.

What Are US Bonds and Why Are They Worth Investing In?

US Bonds, also known as US Treasury bonds, are essentially “debt instruments” issued by the US government to raise funds from investors. When investors purchase US bonds, they are effectively lending money to the US government, which in return promises to repay the principal at a specified future date and pay interest regularly during the holding period. As the US government holds one of the highest credit ratings globally, US bonds are widely regarded as a “risk-free asset” or one of the lowest-risk investment instruments.

Definition and Common Types of US Bonds (Short-Term, Medium-Term, Long-Term)

US bonds are categorized based on their maturity and can generally be divided into three types:

Short-Term Treasury Bills (Treasury Bills, T-Bills): Typically mature within one year or less (e.g., 4 weeks, 8 weeks, 13 weeks, 26 weeks, 52 weeks). T-Bills do not pay fixed interest but are issued at a discount to face value, and investors receive the full face value at maturity, with the difference being the return.

Medium-Term Treasury Notes (Treasury Notes, T-Notes): Maturities range from 2 to 10 years. T-Notes pay interest every six months (known as coupon payments) and repay the principal at maturity.

Long-Term Treasury Bonds (Treasury Bonds, T-Bonds): Have the longest maturities, typically 20 or 30 years. Like T-Notes, T-Bonds pay interest every six months and return the principal at maturity.

Three Core Advantages of Investing in US Bonds: High Safety, Stable Cash Flow, Risk Diversification

Among various investment instruments, US bonds are highly favored, especially during uncertain market conditions, mainly due to the following three advantages:

High Safety: Backed by the credit of the US federal government, with extremely low default risk, widely recognized as a global safe haven for capital.

Stable Cash Flow: For medium- and long-term bonds, investors receive regular (usually semi-annual) interest income, providing predictable cash flow to the portfolio.

Risk Diversification: US bond prices often have a negative or low correlation with stock markets. When equities decline, capital tends to flow into bonds as a safe haven, potentially pushing bond prices higher and helping balance portfolio volatility.

Understanding the Key Indicator: What Is US Bond Yield?

When discussing US bond investments, the most commonly heard term is “bond yield”. Understanding it is crucial for evaluating whether a bond investment is attractive. Many beginners confuse yield with coupon rate, but the two are fundamentally different concepts.

Yield vs. Coupon Rate: What Is the Difference?

To understand the difference, consider a simple scenario:

Coupon Rate: This is the fixed annual interest rate printed on the “debt instrument” at issuance. For example, a 10-year US Treasury bond with a face value of $1,000 and a coupon rate of 2% means the US government pays $20 annually until maturity. This rate remains unchanged throughout the bond’s life.

Yield: This refers to the “actual annualized return” an investor earns if the bond is held to maturity. Yield is dynamic and depends on the price at which the bond is purchased.

For example, for the same bond with a face value of $1,000 and annual interest of $20:

If you buy it at $1,000, the yield is 2% ($20 / $1,000).

If market conditions change and the bond price drops to $950, you still receive $20 annually, but your yield rises to about 2.1% ($20 / $950).

Conversely, if the bond price rises to $1,050, your yield decreases to about 1.9% ($20 / $1,050).

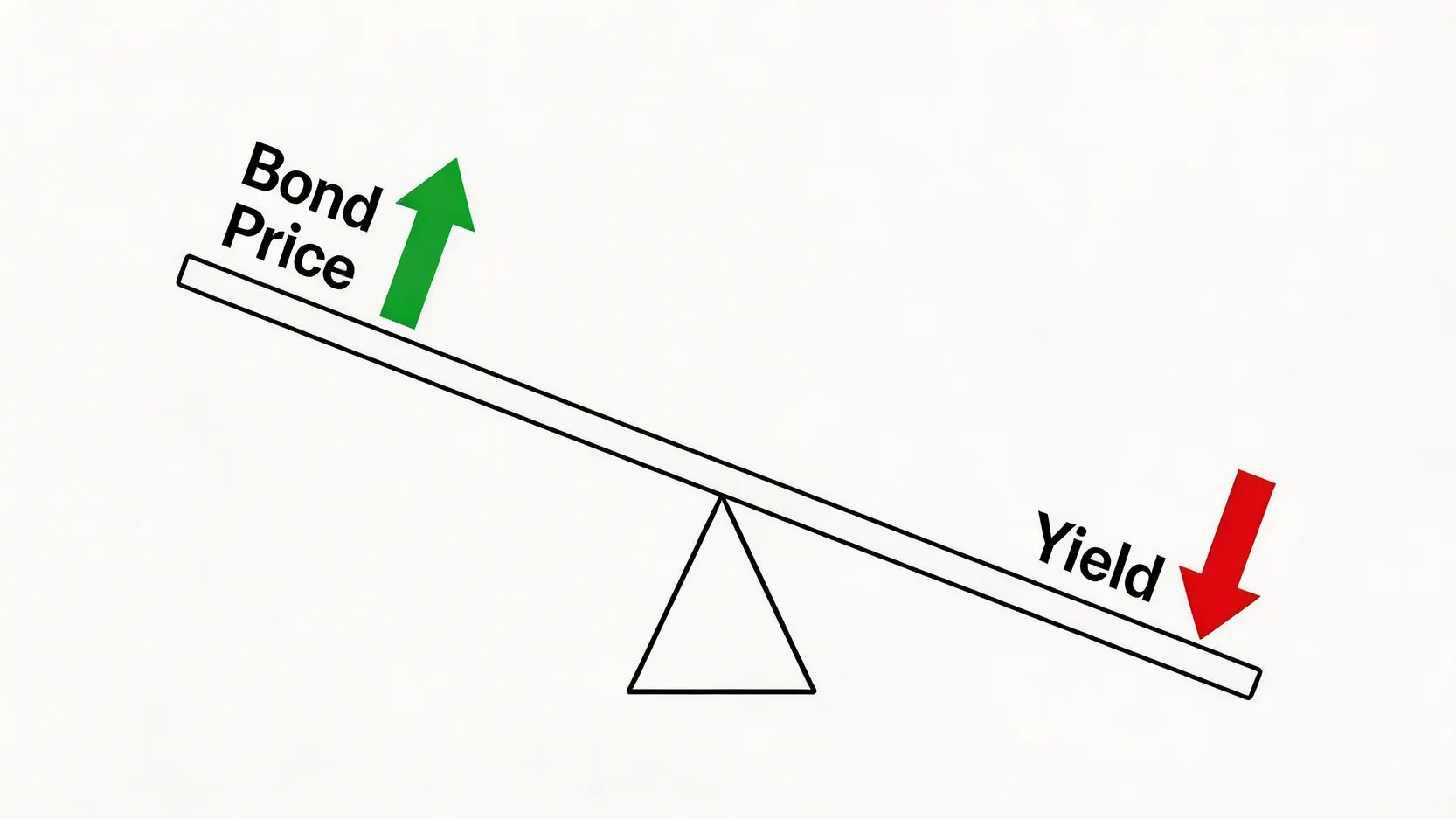

Inverse Relationship Between Yield and Bond Price: Why Do Rates Rise While Prices Fall?

This is a core concept: bond prices and yields always move in opposite directions. The reason lies in market interest rates.

Imagine you hold an old bond issued last year with a coupon rate of 2%. This year, due to interest rate hikes by the Federal Reserve, newly issued bonds offer a 4% coupon. At that point, who would be willing to buy your 2% bond at its original price?

To sell your old bond, your only option is to “lower the price and sell”. When the bond price falls, a new buyer obtains the same interest income at a lower cost, increasing the actual return (yield), making it competitive with newly issued bonds offering 4%. This explains why “when interest rates rise, bond prices fall”.

Bond prices and yields move inversely, like two ends of a seesaw.

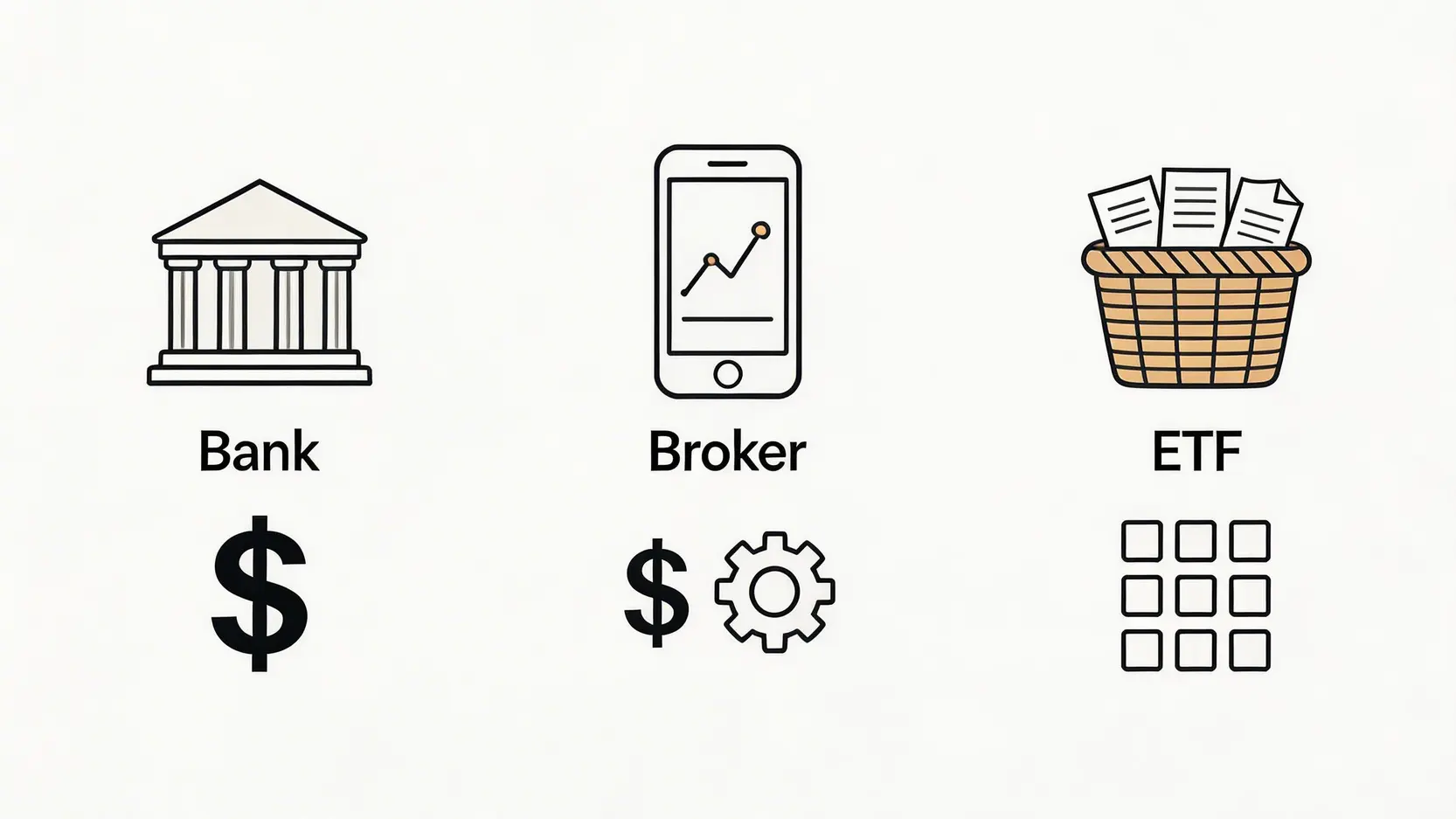

【Methods of Buying US Bonds in Hong Kong】Comprehensive Comparison of 3 Major Channels

After understanding the basics, it is time for practical application. In Hong Kong, investors can mainly purchase US bonds through the following three channels. Each method has its advantages and disadvantages, suitable for different investment needs.

Three Main Channels for Buying US Bonds in Hong Kong: Banks, Brokers, and Bond ETFs

Method 1: Buying Through Local Banks (Advantages and Disadvantages)

Most major banks in Hong Kong, such as HSBC, Bank of China (Hong Kong), and Citibank, provide US Treasury trading services. This is usually the most traditional and direct method.

Advantages: – Familiar operation: For clients with existing bank accounts, there is no need to open a new account, and the process is relatively straightforward. – Perceived stability: Trading through large banks provides a stronger sense of security.

Disadvantages: – High entry threshold: Banks typically require a relatively large minimum investment per transaction, often starting from tens of thousands or even hundreds of thousands of US dollars. – High fees:Various charges may apply, including custody fees, interest collection fees, and redemption fees at maturity, which can erode returns. – Limited selection:The range of bond types and maturities may be more limited compared to professional brokers.

Method 2: Trading Directly Through Broker Apps (Fees and Convenience Comparison)

In recent years, more investors have chosen to trade US bonds through securities brokers (or brokers) especially those offering convenient mobile apps.

Advantages: – Low entry threshold: Many brokers require a minimum investment of only $1,000 or even less, suitable for small investors. – Lower costs: Trading commissions and custody fees are generally much lower than banks, helping improve net returns. – Wide selection: Provides a broader range of US Treasury types and maturities, facilitating diversified bond portfolios. – High convenience: Transactions can be conducted anytime through mobile apps, with easy access to real-time quotes.

Disadvantages: – Account opening required: New users must complete the account setup process. – Requires self-research: Investors need a certain level of knowledge to select suitable bonds independently.

Method 3: Investing in US Bond ETFs (Best Option for Beginners)

For investors who do not want to analyze individual bonds but wish to participate in the US bond market with a very low entry barrier, US bond ETFs (exchange-traded funds) are an excellent choice.

A bond ETF is like a “basket of bonds” where fund managers pre-purchase a diversified portfolio of US bonds with different maturities and package them into tradable units listed on stock exchanges. Investors can trade these ETF units like stocks.

Advantages: – Extremely low entry cost: The lowest barrier, sometimes requiring only tens of US dollars to purchase one ETF unit. – High diversification: Buying one ETF unit means investing in dozens or even hundreds of bonds, significantly reducing risk. – High liquidity: Can be traded anytime during market hours, offering strong liquidity.

Disadvantages: – No maturity date: ETFs continuously buy and sell bonds to maintain investment objectives, so there is no principal repayment at maturity, and prices fluctuate continuously. – Management fees: Fund managers charge an annual expense ratio. – Price volatility: ETF prices fluctuate based on interest rates and market demand, and returns are not fixed.

Comprehensive Comparison Table of Entry Thresholds, Fees, and Convenience Across Channels

Comparison Item

Local Banks

Securities Brokers (Brokerage Firms)

US Bond ETFs

Entry Threshold

High (usually > USD 10,000)

Low (usually starting from USD 1,000)

Extremely low (one share typically costs several tens to a little over a hundred USD)

Fees

Relatively high (custody fees, interest collection fees, etc.)

Medium (can purchase multiple bonds independently)

High (diversified basket of bonds)

Suitable Investors

Investors with large capital seeking a more traditional and stable approach

Self-directed investors seeking low costs and flexible trading

Beginners, small investors, and those seeking maximum diversification

Three Major Risks You Must Know Before Investing in US Treasuries

Although US Treasuries are considered safe assets, “low risk” does not equal “no risk”. Before committing funds, you must clearly understand the following potential risks:

Interest Rate Risk: How Does Fed Policy Affect Your Returns?

This is the primary risk in bond investing. As mentioned earlier, market interest rates move inversely with bond prices. If the US Federal Reserve (Fed) enters a rate-hiking cycle, newly issued bonds will offer higher yields, causing the market price of existing bonds to fall. If you need to sell a bond before maturity, you may incur a loss. Generally, the longer the bond’s term, the more sensitive it is to interest rate changes, and the greater its price volatility.

Currency Risk: The Impact of HKD to USD Exchange

Although the Hong Kong dollar is pegged to the US dollar, maintaining relative stability between 7.75 and 7.85, fluctuations still exist. If you buy when the USD is strong and sell when it is weaker, converting back to HKD could result in a foreign exchange loss. While this risk is relatively minor for HKD investors, it remains a factor to consider.

Inflation Risk: Long-Term Returns May Be Eroded

Inflation risk refers to the scenario where rising prices outpace your bond interest returns, resulting in a “nominal gain but real loss”. For example, if your bond yields 3% annually but the year’s inflation rate is 4%, your real return is actually negative 1%. For long-term bond investors, this is a risk that must be taken seriously.

Common Questions About Buying US Treasuries in Hong Kong (FAQ)

Q: What is the minimum amount to invest in US Treasuries?

A: It depends entirely on your investment channel. Through bond ETFs, the entry threshold is lowest, possibly requiring only a few hundred HKD per share. If buying individual bonds directly through a brokerage, the minimum is usually 1,000 USD. Banks have the highest thresholds, which may require tens of thousands of US dollars or more.

Q: Do I need to pay taxes on US Treasury interest income in Hong Kong?

A: Hong Kong follows a territorial source principle and does not levy capital gains tax or interest tax. Therefore, interest or capital gains from overseas assets (including US Treasuries) are generally not taxable in Hong Kong. However, the US government withholds 30% tax on interest income for non-US persons, though Treasury interest is usually exempt. It is recommended to consult your broker or tax advisor for specific situations.

Q: What is the difference between a US Treasury ETF and buying US Treasuries directly?

A: The main difference lies in “maturity” and “return certainty”. When you buy US Treasuries directly, holding them to maturity guarantees the return of principal plus fixed coupon interest, locking in returns. A US Treasury ETF has no maturity; it continuously buys and sells bonds, and its price fluctuates like a stock with no principal guarantee. Its advantages are extremely low entry barriers and high diversification.

Q: What Is a “Yield Curve Inversion”?

Comparison between a normal yield curve (left) and an inverted yield curve (right).

A: A “yield curve inversion” occurs when short-term government bond yields are higher than long-term yields. Normally, long-term bonds offer higher yields to compensate for longer exposure and interest rate risk. An inversion typically reflects market expectations of an economic slowdown or even recession, prompting the Fed to cut rates, causing long-term yields to fall in advance. Historically, yield curve inversions are often considered a leading indicator of economic recession.

Conclusion

In summary, US bonds are an ideal tool for Hong Kong investors seeking stable returns and asset protection. Through the methods introduced in this article, including banks, brokerages, and ETFs, you can choose the approach to buying US Treasuries in Hong Kong that best suits your capital size, risk tolerance, and investment preferences. Before taking action, be sure to fully understand the dynamics of US Treasury yields and carefully assess potential risks such as interest rates, currency exchange, and inflation. This will allow you to use US Treasuries prudently to grow your wealth. Start planning your US Treasury investment today!

[Second Half of 2026] Complete Japanese Yen Outlook Forecast: The Ultimate Currency Exchange Strategy for Investors and Travelers Following record-breaking market interventions, the future outlook for the Japanese yen is filled with both uncertainty and opportunity. Will the yen regain its strength, or will it fall to new lows? This...

How Significant Is the Impact of the Geopolitical Risk Premium on Taiwan Stocks? Understanding the Risks, Opportunities, and Investment Strategies In an increasingly globalized world, Taiwan's stock market is influenced not only by economic fundamentals but is also constantly exposed to complex geopolitical risks. From tensions in cross-strait relations to...

The Fourth Largest Net Buy in History! Foreign Investors Snap Up NT$62.7 Billion of Taiwan Stocks, Revealing Three Key Signals Behind Stocks and the Currency Rising in Tandem Taiwan's stock market staged a stunning rally, surging more than 900 points in a single day with trading volume reaching extraordinary levels....