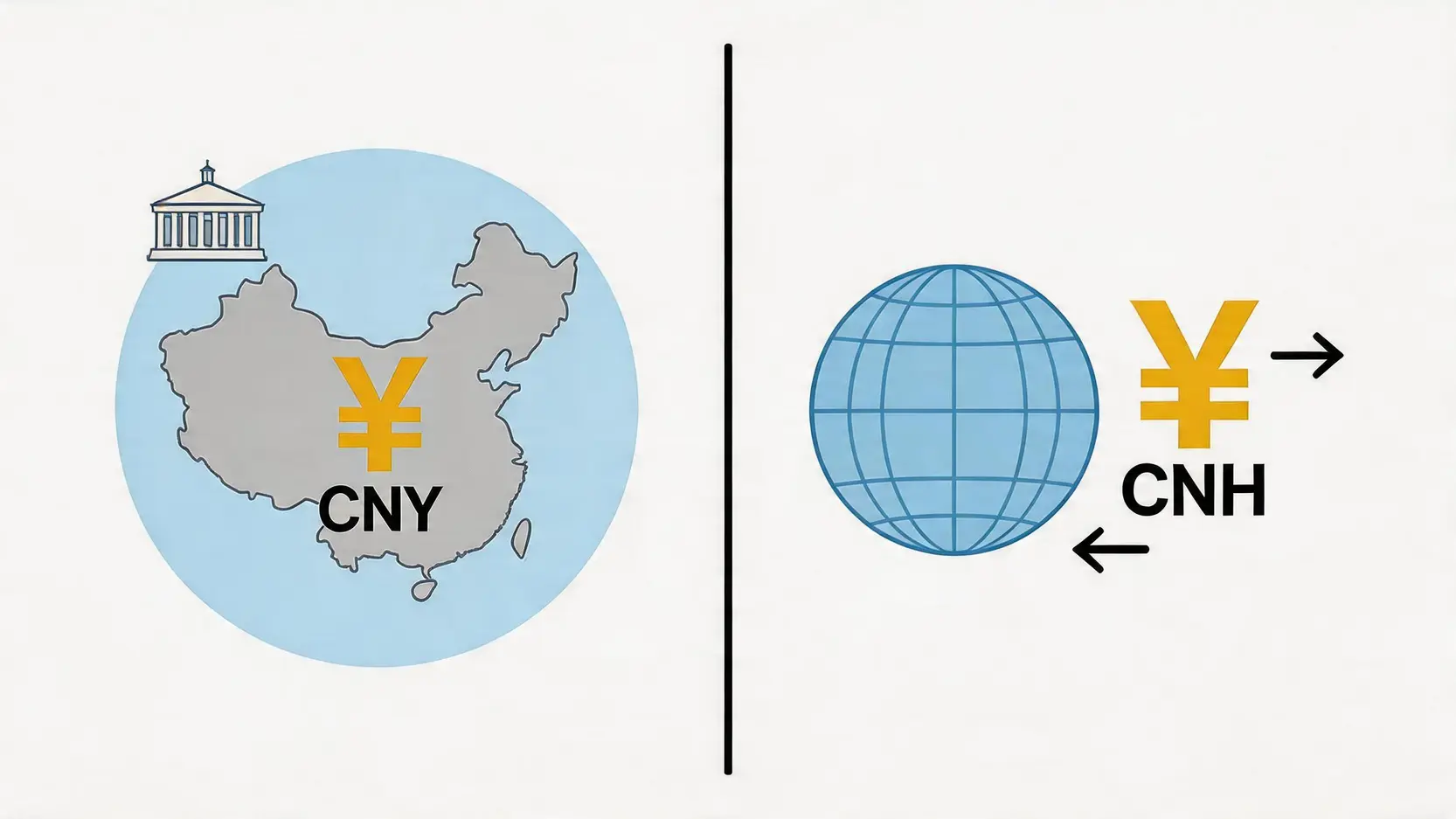

Core Difference Between Onshore (CNY) and Offshore (CNH) Markets: Control vs. Freedom

Onshore RMB (CNY): Definition, Market and Regulatory Features

Onshore RMB, with the code CNY (Chinese Yuan), refers to RMB circulating and traded within mainland China. Its characteristics can be summarized as follows:

- Main market: China mainland interbank foreign exchange market.

- Price formation: Strictly regulated by the People’s Bank of China (PBoC). Before each trading day opens, the central bank announces a “RMB central parity rate”, and the spot exchange rate is only allowed to fluctuate within a 2% band above or below this midpoint.

- Trading restrictions: Transactions must be backed by real trade or investment purposes, and both individuals and companies are subject to strict annual foreign exchange quotas. Capital account conversions are heavily controlled to prevent large-scale capital inflows or outflows.

- Liquidity: Primarily reflects China’s domestic economic conditions and policy direction.

Offshore RMB (CNH): Definition, Main Trading Markets (e.g., Hong Kong), and Pricing Mechanism

Offshore RMB, with the code CNH (Chinese Yuan Offshore), refers to RMB traded outside mainland China. It was initially introduced in Hong Kong to promote RMB internationalization and has since expanded to financial centers such as Singapore, London, and Taiwan.

- Main market: Hong Kong is the largest and most important offshore RMB trading center, with other markets also becoming increasingly active.

- Price formation: The CNH exchange rate is primarily driven by free market supply and demand, with limited direct intervention from the People’s Bank of China. Therefore, its price more accurately reflects global expectations of China’s economy, international risk sentiment, and offshore RMB supply and demand.

- Trading restrictions: Trading is relatively free, not subject to mainland China’s capital controls, allowing investors greater flexibility in conversion, investment, and trading.

- Liquidity: Mainly influenced by international investor sentiment and global macroeconomic events.

Visual Comparison: CNY vs CNH Core Differences Table

To help you better understand the differences between the two, we have compiled the following comparison table:

| Comparison Item |

Onshore RMB (CNY) |

Offshore RMB (CNH) |

| Trading Location |

Mainland China |

Outside mainland China (e.g. Hong Kong, Singapore, London) |

| Regulatory Authority |

People’s Bank of China (PBoC), State Administration of Foreign Exchange (SAFE) |

Primarily regulated by local financial regulators (e.g. Hong Kong Monetary Authority) |

| Exchange Rate Formation Mechanism |

Managed floating exchange rate system (based on central parity rate with fluctuation band limits) |

Free-floating exchange rate determined by market supply and demand |

| Main Influencing Factors |

China’s macroeconomic policies, central bank intervention |

International investor sentiment, global capital flows, offshore RMB supply and demand

|

| Degree of Trading Freedom |

Relatively low, subject to capital account controls |

Relatively high, no capital controls |

Core Question: Why Does a Spread Exist Between Onshore and Offshore RMB?

After understanding the basic differences between the two, the reason for the exchange rate spread becomes clear. The onshore–offshore RMB price gap mainly arises from fundamental differences in regulatory policies and market participants between the two markets, which can be summarized into the following two key factors:

Policy Factors: The People’s Bank of China’s Central Parity Rate and Foreign Exchange Controls

The price of CNY is firmly “anchored” within a controlled range by the central bank. The daily RMB central parity rate announced by the People’s Bank of China sets a benchmark for the market, preventing extreme exchange rate volatility. This policy intervention makes the movement of CNY relatively stable and predictable. At the same time, strict foreign exchange controls restrict the free flow of capital, effectively creating a “firewall” between the onshore and offshore markets, preventing funds from freely moving across markets to eliminate price discrepancies.

Market Factors: Offshore Supply and Demand Dynamics and Investor Sentiment

The price of CNH, on the other hand, acts as a more accurate reflection of international market sentiment. When overseas investors are optimistic about China’s economic outlook, they tend to buy RMB assets, pushing CNH higher. Conversely, when negative news emerges or global risk aversion rises, investors may sell RMB assets, causing CNH to depreciate. These sentiment-driven fluctuations are often more volatile than in the onshore market. As a result, when domestic and overseas sentiment diverge, the spread between CNH and CNY can widen significantly.

For example, if international markets broadly expect the RMB to depreciate, offshore investors may heavily sell CNH, causing CNH (against USD) to decline. However, due to central bank intervention and capital controls in the onshore market, the depreciation of CNY may be more moderate or even stable. In this case, CNH becomes “cheaper” than CNY, resulting in a negative spread (CNY > CNH).

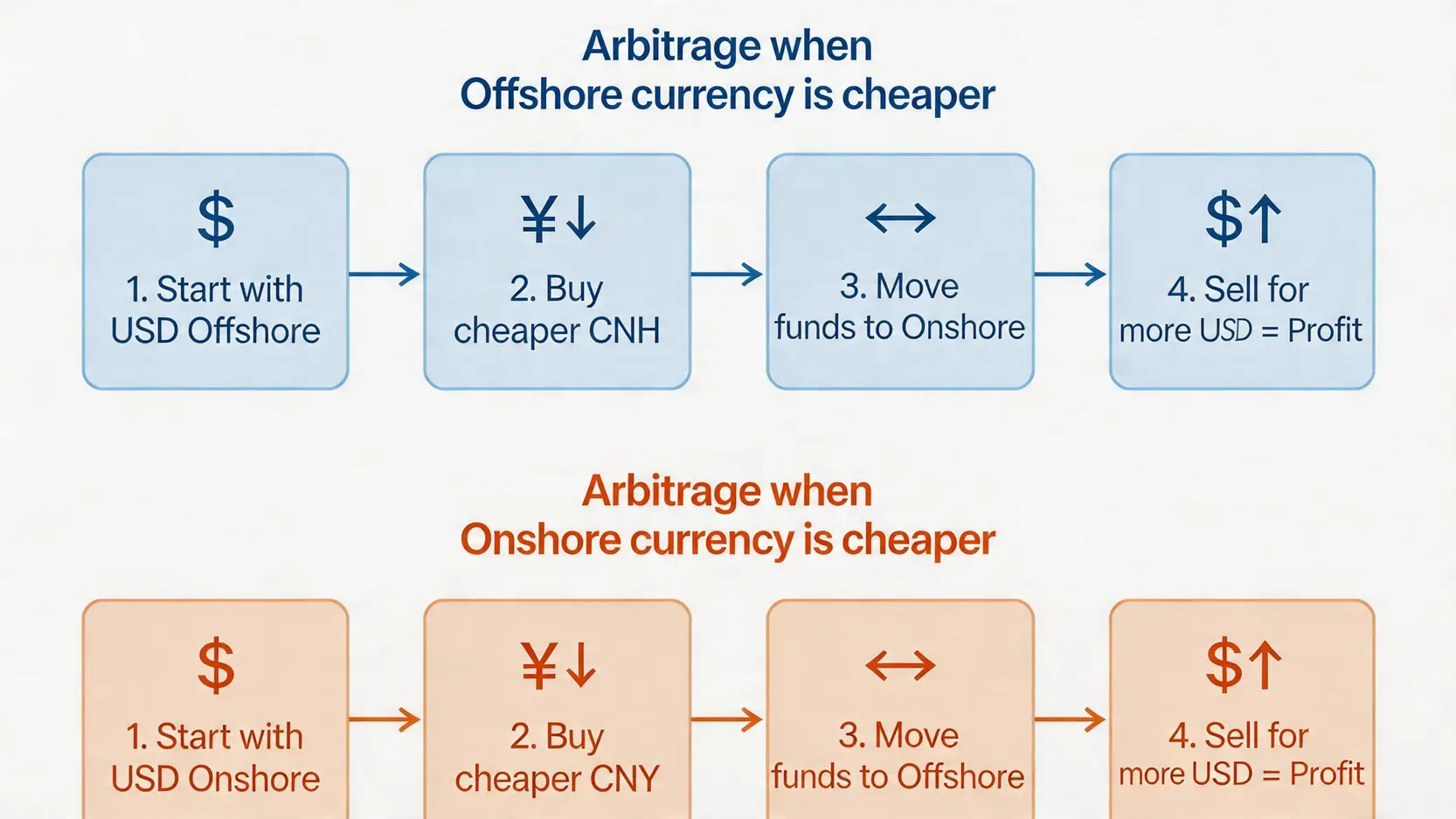

Profit Core: Full Analysis of CNY–CNH Arbitrage Opportunities

Where there is a spread, there is arbitrage potential. The so-called CNY–CNH arbitrage opportunity refers to exploiting exchange rate differences between the onshore and offshore RMB markets by buying low and selling high to earn profits. This requires traders to operate across two segmented markets.

Basic Principle of Arbitrage and Common Models

The core principle of arbitrage is simple: Buy in the lower-priced market and sell in the higher-priced market.