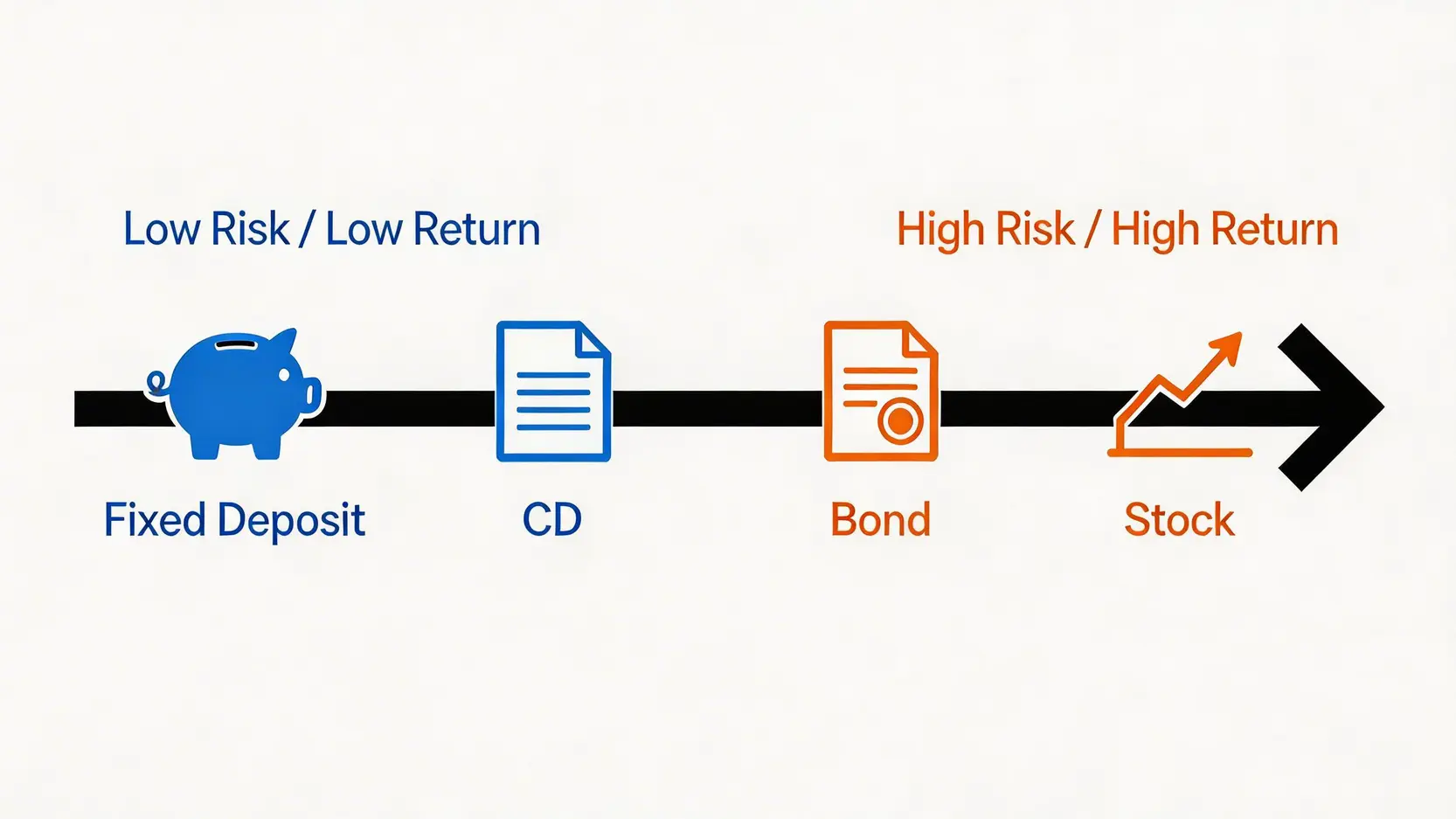

Figure 2: Positions of Four Tools on the Risk and Return Spectrum

Comparison of Return Potential: Stock Potential vs Bond Stability

As shown in the table above, return potential is generally proportional to risk. Stocks are undoubtedly the leader in potential returns, with a high-quality growth stock potentially delivering multiple times returns within a few years, but at the same time it may also result in significant capital loss. Bond returns are much more stable, mainly derived from coupon payments. Although they are less exciting than stocks, they can provide steady cash flow. Certificate of deposit and fixed deposit offer the lowest returns among the four, and their core value lies in “capital preservation” rather than “capital appreciation”.

Risk Assessment: From Capital Preservation to High Volatility, Which Risk Level Suits You

When assessing risk, it is not only about whether you will “lose money”, but also about the causes of potential losses.

- Fixed deposit / certificate of deposit: Extremely low risk, mainly concerned with the risk of bank failure, but in a sound financial system with deposit protection schemes, this risk is negligible.

- Bond: Risk is more complex. Even government bonds with the highest credit rating still carry “interest rate risk”, when market interest rates rise, the attractiveness of existing bonds declines and their prices fall. Corporate bonds carry additional “credit risk”, meaning the issuer may be unable to repay due to poor financial performance.

- Stock: Highest and most diverse risk profile, including “market risk” (overall market decline), “sector risk” (policy changes impacting specific industries), and “individual stock risk” (poor management or weak financial results). Stock price volatility is significantly higher than bonds.

To learn more about the characteristics of different investment tools, you may refer to professional information provided by the Investor and Financial Education Council, which can help you make more comprehensive decisions.

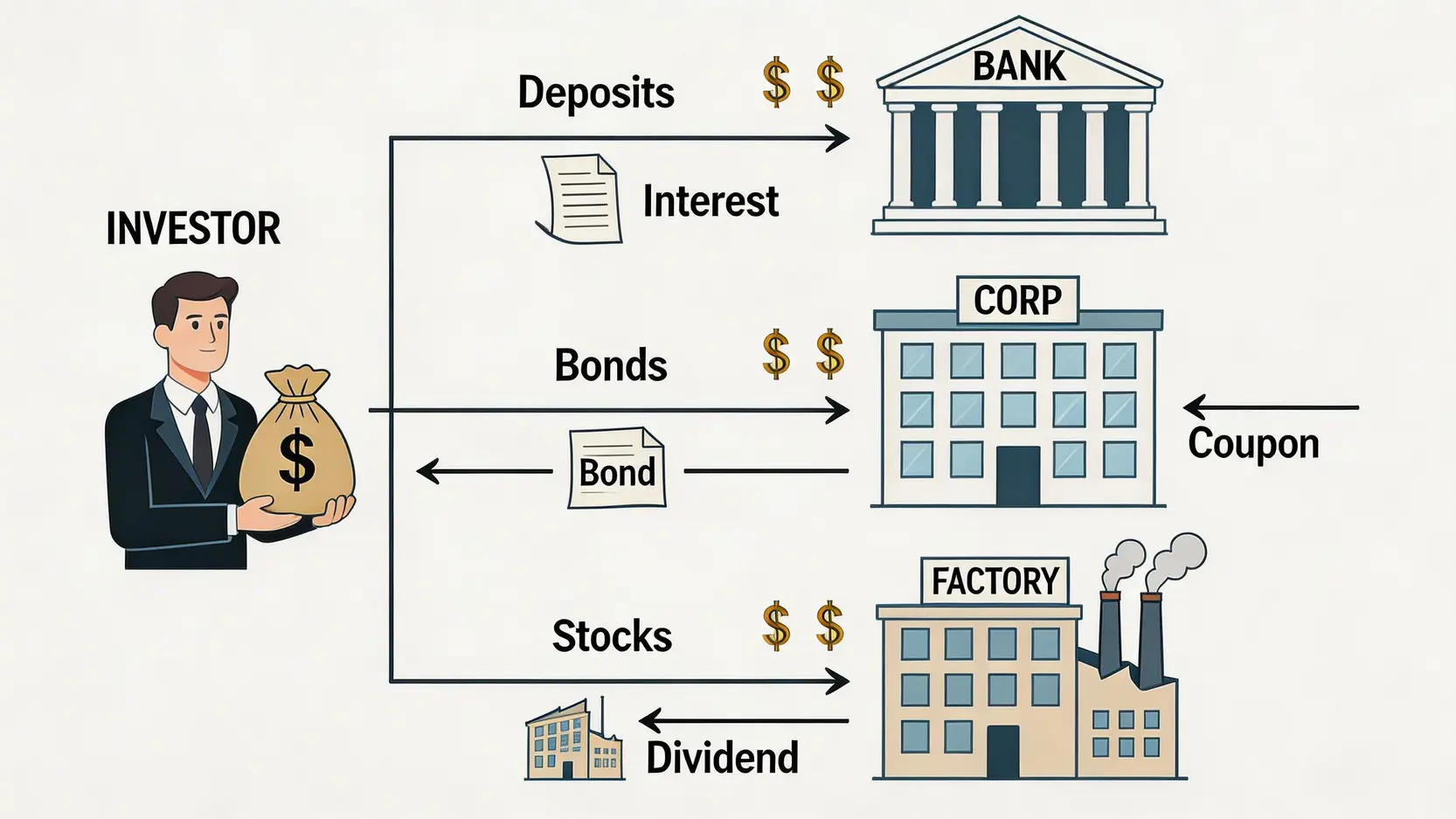

Capital Flexibility: If I Need Money Urgently, Which Tool Has the Highest Liquidity?

Liquidity refers to how quickly an asset can be converted into cash without significantly affecting its market price. In this regard, stocks perform best, as they can generally be sold at any time during trading hours, with funds becoming available within 1–2 trading days. Bonds and certain certificates of deposit can also be traded in secondary markets, but execution speed and pricing may not be as favorable as stocks. Fixed deposits have the worst liquidity, as early withdrawal usually incurs penalties or loss of part or all of the interest.

Scenario Analysis: Which Investment Tool Should I Choose

After understanding the theory, it ultimately comes down to real-world application. Different life stages, financial goals, and risk preferences determine your optimal choice.

Conservative Investors: Choosing Between Fixed Deposits and Certificates of Deposit

If your primary goal is 100% capital preservation and you cannot accept any losses, then fixed deposits and certificates of deposit are your safe havens. How to choose?

- When banks offer high-yield certificates of deposit with interest rates significantly higher than comparable fixed deposits, they are worth considering.

- Confirm whether the certificate of deposit is covered under local deposit protection schemes.

- If you are certain that you will not need the funds before maturity, then simply choose the one with the higher interest rate.

Balanced Growth Investors: Portfolio Allocation Between Bonds and Stocks

These investors aim for steady asset growth but are unwilling to accept excessive volatility. The classic “stock-bond balance” strategy is therefore commonly used. By holding both stocks and bonds, risk can be effectively diversified. In general, during economic downturns, stocks fall while capital flows into bonds as a safe haven, pushing bond prices up and partially offsetting stock losses.

- Starter allocation: Consider using stock ETFs tracking broad market indices and bond ETFs consisting of government or high-grade corporate bonds to achieve easy diversification.

- Asset allocation: Common ratios include 60% stocks / 40% bonds, or adjusting based on age, such as using “100 minus your age” as the percentage of stocks in your portfolio.

High Risk Tolerance Investors: Stocks as Core, Bonds as Supplement

Young investors with stable income and a long investment horizon can tolerate higher risk in exchange for long-term returns. For this type of investor, stocks should be the absolute core of the portfolio.

- Core holdings: 70%–90% of capital can be allocated to global or specific market equities, including growth and value stocks.

- Supplementary role: The remaining 10%–30% can be allocated to bonds. Bonds serve two purposes here: first, as reserve funds for “buying the dip” during market downturns; Second, to reduce overall portfolio volatility, helping investors stay more stable during market turbulence.

Conclusion

In summary, there is no absolute best among certificates of deposit, bonds, stocks, and fixed deposits, only what is suitable for you. Fixed deposits and certificates of deposit provide stable, capital-protected returns and act as a safe haven for funds, suitable for investors with zero risk tolerance. Bonds strike a balance between risk and return and serve as a cornerstone for stable cash flow. Stocks offer the highest return potential but also come with the greatest market volatility, acting as the engine for significant asset growth. Before making any investment decision, be sure to assess your financial situation, investment goals, and risk tolerance, and choose the tools that best help you achieve your objectives, or even combine them to build your own investment fleet.

Frequently Asked Questions (FAQ)

Q: What is the biggest difference between certificates of deposit and fixed deposits?

A: There are mainly two differences. First is “liquidity”. Some certificates of deposit can be transferred in the secondary market, while early withdrawal of fixed deposits usually incurs penalties. Second is “interest rate”. Certificates of deposit with the same tenor generally offer slightly higher interest rates than fixed deposits to attract funds. Third, in some regions, the deposit protection coverage for certificates of deposit may differ from fixed deposits, so it is necessary to confirm before investing.

Q: Can you lose money investing in bonds? What are the main risks?

A: Yes. Bond investment is not risk-free. The main risks include: 1. Interest rate risk: when market interest rates rise, the attractiveness of existing bonds with fixed coupons decreases, and their market price falls. 2. Credit risk (default risk): the issuing company or government may experience financial deterioration and fail to pay interest or repay principal on time. 3. Inflation risk: if inflation exceeds the bond’s coupon rate, your real purchasing power actually declines.

Q: Which is more suitable for beginners, stocks or bonds?

A: It depends on the beginner’s risk tolerance and investment goals. If a beginner is extremely risk-averse and seeks stable cash flow, high-grade bonds or bond funds are a good starting point. If a beginner can tolerate some price volatility and aims for long-term capital appreciation, starting with index stock funds (ETFs) is a more effective growth path. The best approach may be to allocate to both and experience their different levels of volatility firsthand.

Q: How much capital is needed to start investing in these tools?

A: The entry threshold varies significantly. Stocks can have a very low barrier, as in some markets you can buy as little as one share or even fractional shares, allowing you to start with just a few dozen dollars. Fixed deposits also have relatively accessible minimum requirements. However, certificates of deposit and direct purchase of individual bonds usually require higher capital, potentially starting from tens of thousands or even hundreds of thousands. Nowadays, bond funds or bond ETFs allow indirect investment in the bond market with much lower amounts.

Q: Do dividends and bond interest need to be taxed?

A: Taxation varies by country and region. In many places, dividend income and bond interest are treated as part of personal income and are taxable, but rates and exemptions differ. For example, some regions offer tax advantages on dividends from local companies, while income from overseas investments may be subject to different rules. Before investing, it is best to consult a local tax expert or refer to official tax regulations.