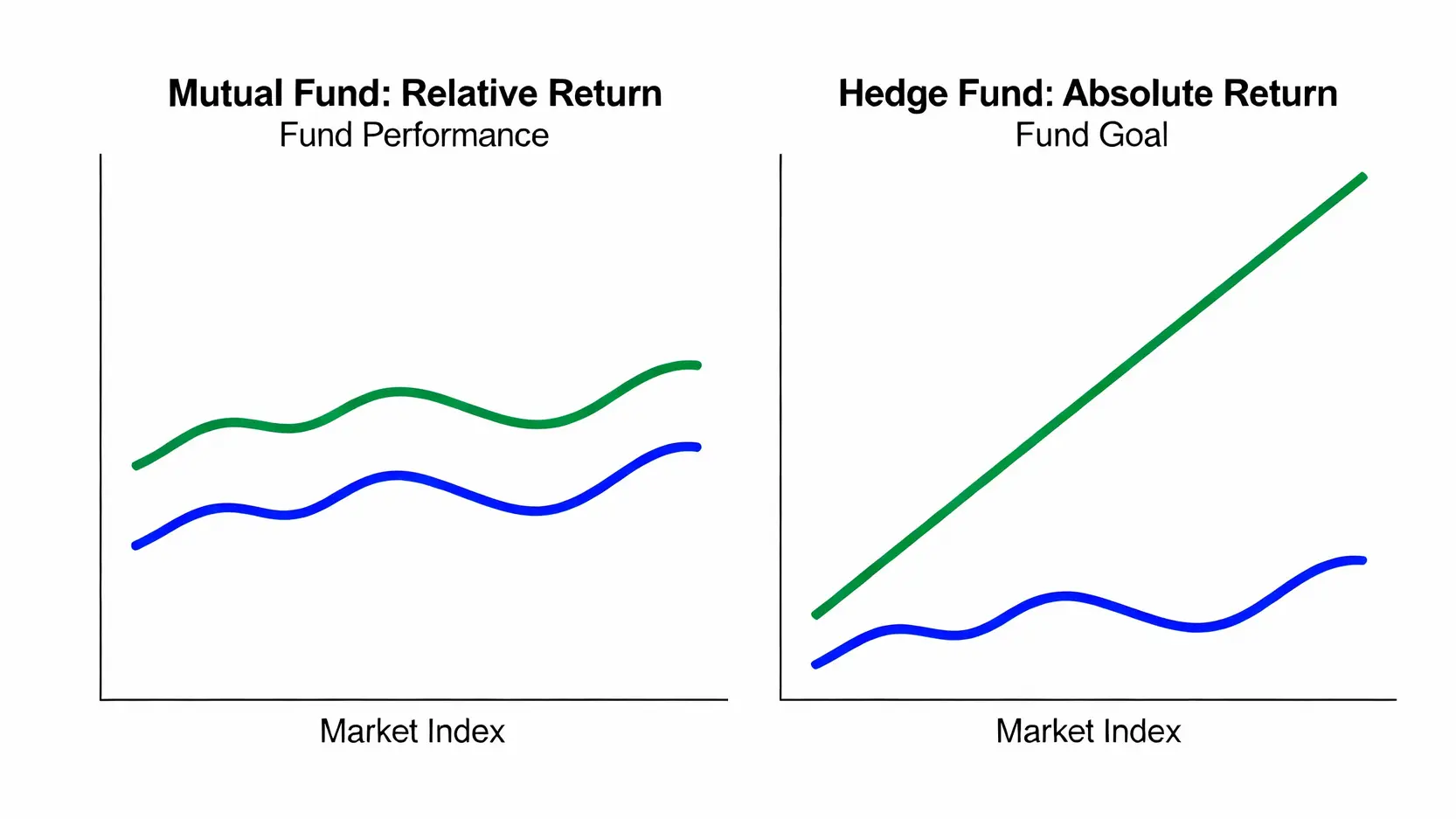

The core of the equity long short strategy is to buy stocks expected to rise (long) and sell stocks expected to fall (short) at the same time, hedging market risk while generating excess returns from stock selection.

- Long: Buy stocks believed to be undervalued with future upside potential.

- Short: Sell stocks believed to be overvalued with expected price declines.

The intelligence of this strategy lies in its dual profit potential. If the overall market rises, gains from long positions may exceed losses from short positions. If the overall market declines, profits from short positions can offset losses from long positions. Ideally, regardless of whether the broader market rises or falls, as long as stock selection is correct, the fund can achieve net gains. This represents the classic embodiment of the “hedging” concept.

Global Macro Strategy

Funds adopting this strategy focus on global macroeconomic trends. Based on forecasts of macroeconomic indicators such as interest rates, exchange rates, national policies, and international trade relations, managers take large scale leveraged positions across global markets. Investment targets include equities, bonds, currencies, and commodities across nearly all asset classes. For example, if a manager anticipates that a country’s central bank will raise interest rates, the fund may go long that country’s currency while shorting its bonds. The attack on the British pound in 1992 by Soros’s Quantum Fund is one of the most famous cases of a global macro strategy.

Event Driven Strategy

This strategy seeks profit opportunities arising from specific corporate events that may significantly impact stock prices, such as:

- Merger Arbitrage: When Company A announces the acquisition of Company B, the share price of Company B typically rises but remains slightly below the acquisition price. The fund buys shares of Company B and may simultaneously short shares of Company A to capture the price spread.

- Distressed Debt: The fund purchases bonds of financially troubled or near bankrupt companies at deep discounts and participates in restructuring negotiations, aiming for substantial value recovery if the company successfully reorganizes.

Quantitative Strategy

This strategy relies entirely on complex mathematical models and high speed computer algorithms to execute trades, with minimal human intervention. Models analyze vast amounts of historical data to identify price patterns and market anomalies and automatically execute trades when opportunities arise. High Frequency Trading is one extreme form of this approach. Renaissance Technologies’ “Medallion Fund” is a legendary representative of quantitative strategy.

Three Major Hedge Fund Risks That Must Be Confronted Before Investing

The high return potential of hedge funds is always accompanied by significant risks that cannot be ignored. Before considering this type of investment, it is essential to have a deep understanding of the following risks, which is why comprehensive risk management is crucial.

Leverage Risk: Potential Losses May Exceed Principal

Leverage is a double edged sword. Hedge funds commonly use high leverage (meaning borrowing to invest) to amplify potential returns. Five times leverage can turn a 20 percent gain into 100 percent, but it can equally turn a 20 percent loss into a 100 percent loss of principal. In extreme cases, losses may even exceed the initial capital invested. The collapse of Long Term Capital Management (LTCM) in 1998 was a catastrophic consequence triggered by excessive leverage, and its impact even threatened the stability of the global financial system.

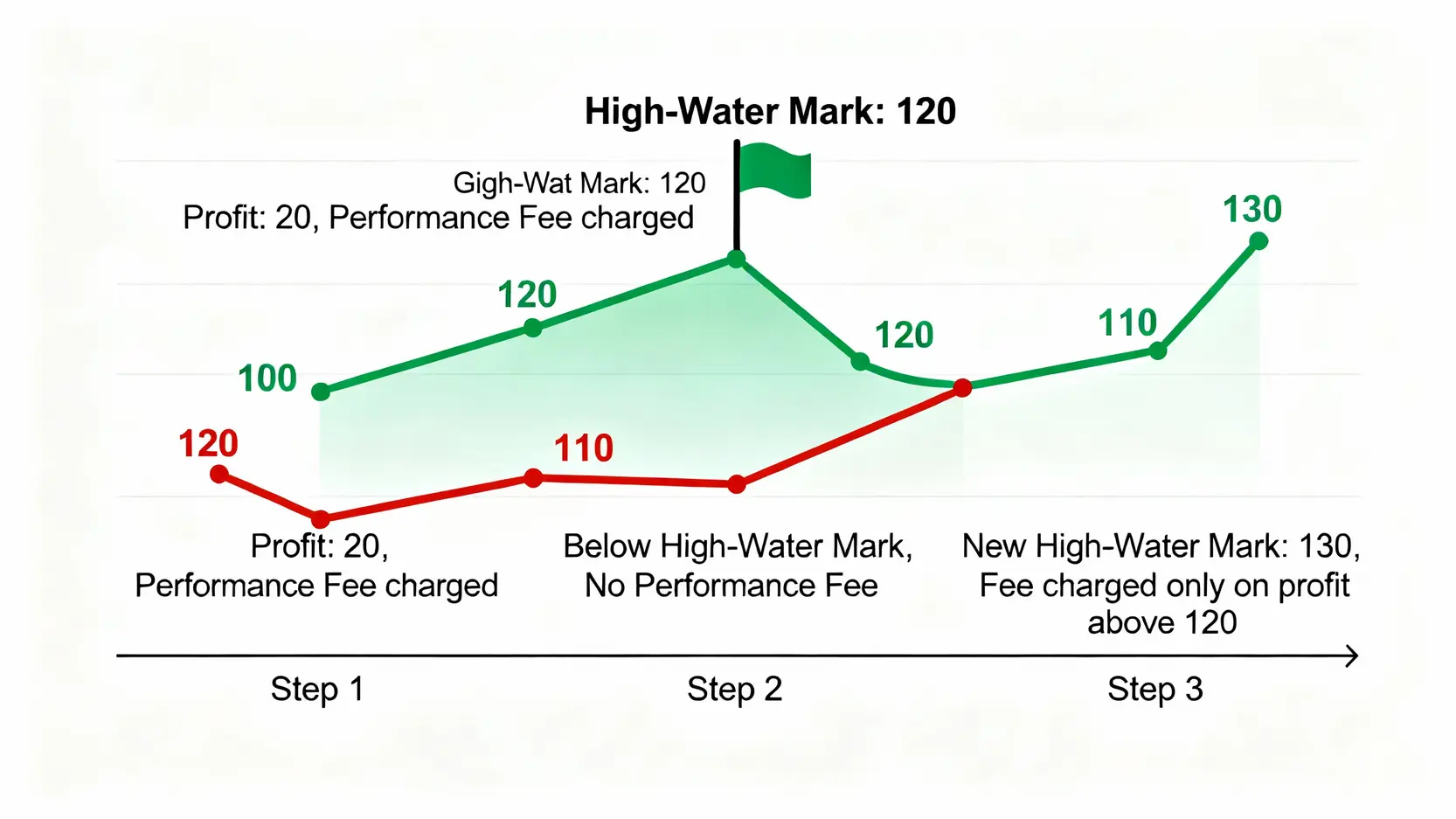

Liquidity Risk: Lock Up Periods Restrict Redemption

Unlike stocks or mutual funds, hedge funds offer very low liquidity. Investors’ capital is typically subject to a “lock up period”, which may last from one year to several years. During this lock up period, investors cannot redeem their funds at all. Even after the lock up period ends, redemption is usually subject to strict limitations, such as being permitted only quarterly or semi-annually, often requiring advance notice. This structure allows fund managers to focus on long term strategies without being forced to liquidate assets to meet short term investor demands, but it also means investors lose access to liquidity for extended periods.

Transparency and Regulatory Risk: Complex Operations with Lighter Regulation

Because hedge funds primarily serve professional investors, regulators generally assume these investors are capable of assessing risks independently, resulting in lighter regulation compared to public mutual funds. This leads to very low transparency. Investors often have limited visibility into the fund’s specific holdings and risk exposures. While such confidentiality helps protect proprietary trading strategies, it also conceals potential risks. To a large extent, investors must rely on the fund manager’s professional expertise and integrity. For more information about the definition of hedge funds, you may refer to Investopedia’s professional explanation.

Frequently Asked Questions About Hedge Funds

Q: Can ordinary retail investors invest in hedge funds?

A: Generally no. In most countries and regions, financial regulations stipulate that hedge funds are only open to “Qualified Investors” or “Professional Investors”. These investors must meet strict asset or income requirements, such as possessing net assets exceeding USD 1 million. This threshold is designed to protect ordinary investors who may lack sufficient risk tolerance and professional knowledge.

Q: Can hedge funds truly “hedge” all risks?

A: No. Although the term “hedge” is part of the name, modern hedge funds do not aim to eliminate all risks. Instead, they seek to manage and hedge “unwanted risks” (such as systemic market risk) in order to focus on generating “desired returns” (such as alpha derived from stock selection). Their strategies aim to produce positive returns under various market conditions, but they remain exposed to significant risks including strategy failure, high leverage, and liquidity constraints.

Q: What is the typical minimum investment threshold for hedge funds?

A: The threshold is very high and varies by fund. Generally, the minimum investment amount starts at USD 1 million. For certain top tier or well known hedge funds, the threshold may reach USD 5 million or even USD 10 million or more. This further highlights their nature as investment vehicles reserved for affluent individuals.

Q: What is the difference between hedge funds and private equity funds?

A: Both are alternative investments targeted at high net worth individuals, but their core businesses differ. Hedge funds primarily invest in liquid public market securities (such as equities, bonds, and currencies), employing flexible and diverse strategies with relatively shorter investment horizons. Private equity funds focus on acquiring equity in private companies, improving operations over the long term, and eventually exiting through an initial public offering or sale, with very long investment cycles lasting (typically five to ten years).

Conclusion

In summary, hedge funds are complex investment vehicles designed for high net worth individuals and institutional investors. Their flexible strategies and persistent pursuit of absolute return give them a unique and important position in the investment world. By utilizing strategies that traditional investment tools cannot easily access (such as short selling and high leverage), they attempt to create value in any market environment. However, behind this high return potential lies equally significant or even greater risk. Before considering an investment, it is essential to fully understand their distinctive operating model, diversified investment strategies, and substantial potential risks. Any qualified investor should seek advice from a professional financial adviser and carefully assess whether their own risk tolerance aligns with this type of high risk, high return investment before making a decision.