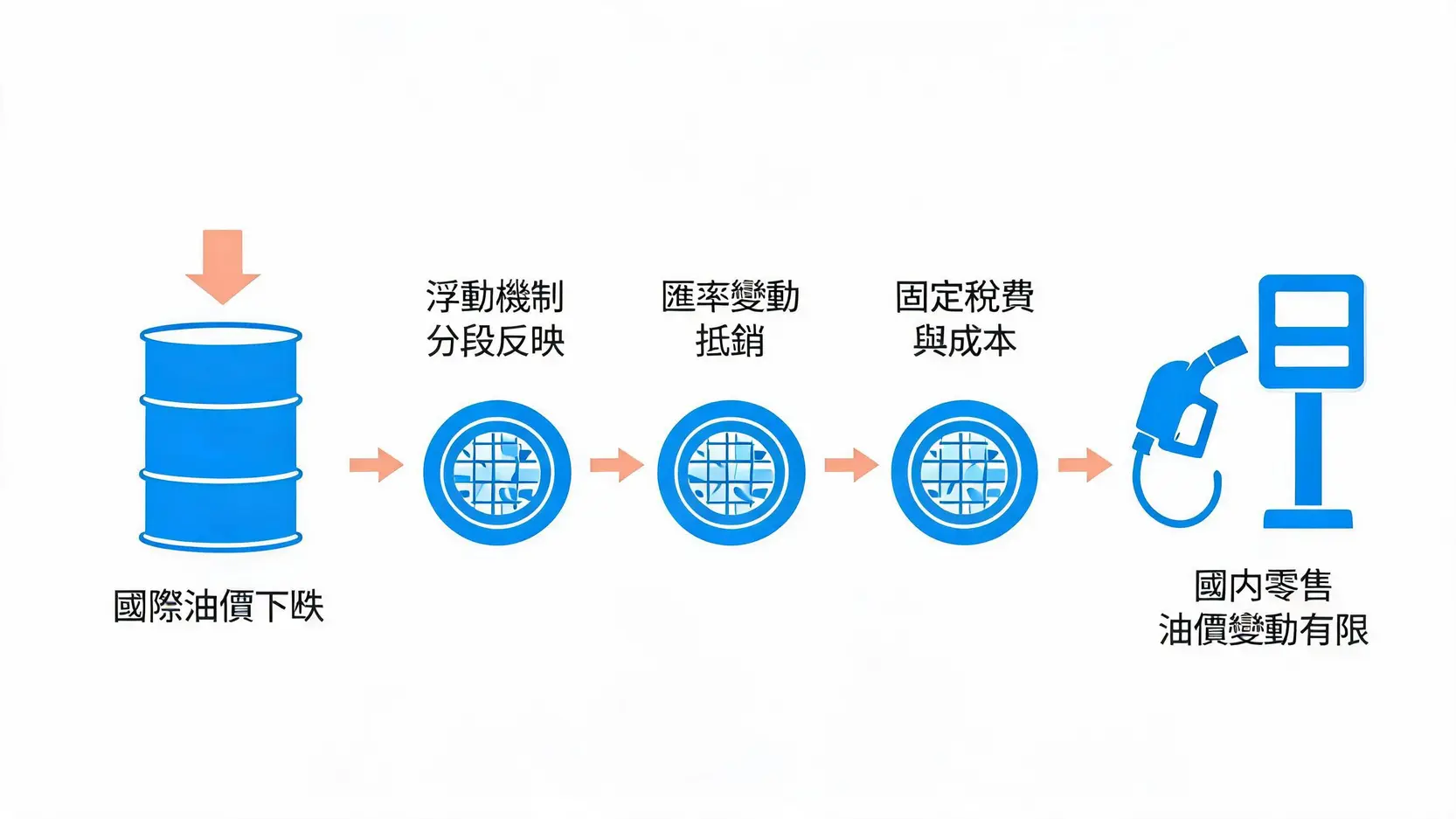

Between international oil prices and petrol station prices, there are still three barriers: mechanisms, exchange rates, and taxes and fees.

Uncovering the Operating Logic of the Domestic Floating Oil Price Mechanism and Stabilization Fund

Taking Taiwan as an example, domestic oil prices refer to the floating oil price mechanism and use stabilization measures to reduce short-term volatility. Simply put: if international oil prices fall very quickly, domestic prices may reflect it in stages; if international oil prices rise very quickly, domestic prices may also absorb it in stages, but not necessarily symmetrically.

In addition, oil products also involve inventory costs (previous high-priced inventory), transportation insurance, refining costs, and other factors, so they may not fully keep up with international quotations in the short term.

How Exchange Rate Fluctuations and Fixed Tax and Fee Structures Eat Into Oil Price Declines

Another key factor is exchange rates and taxes and fees. International crude oil is mostly priced in US dollars, so if the local currency depreciates, part of the benefit of falling oil prices will be offset by exchange losses. In addition, oil product retail prices in many regions include fixed taxes and fees, so even if crude oil itself falls by 30%, the “room for decline” at the retail end will be smaller than you might think.

Therefore, when making investment judgments, do not infer international oil price trends solely from “whether petrol has become cheaper”. They are two separate systems.

FAQ

Will International Oil Prices Continue to Fall in the Future? Which Indicators Should Be Watched for Oil Price Forecasts

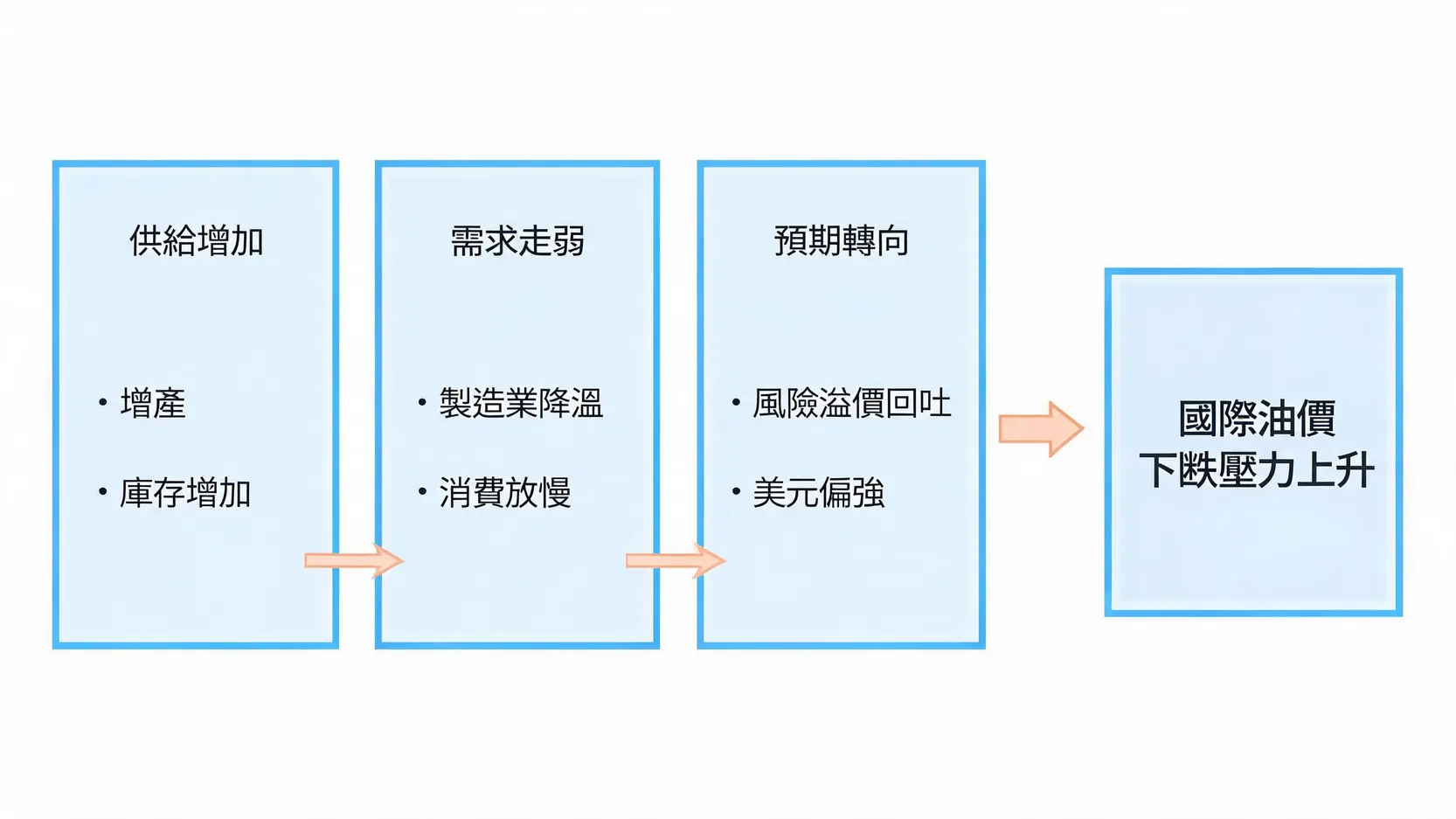

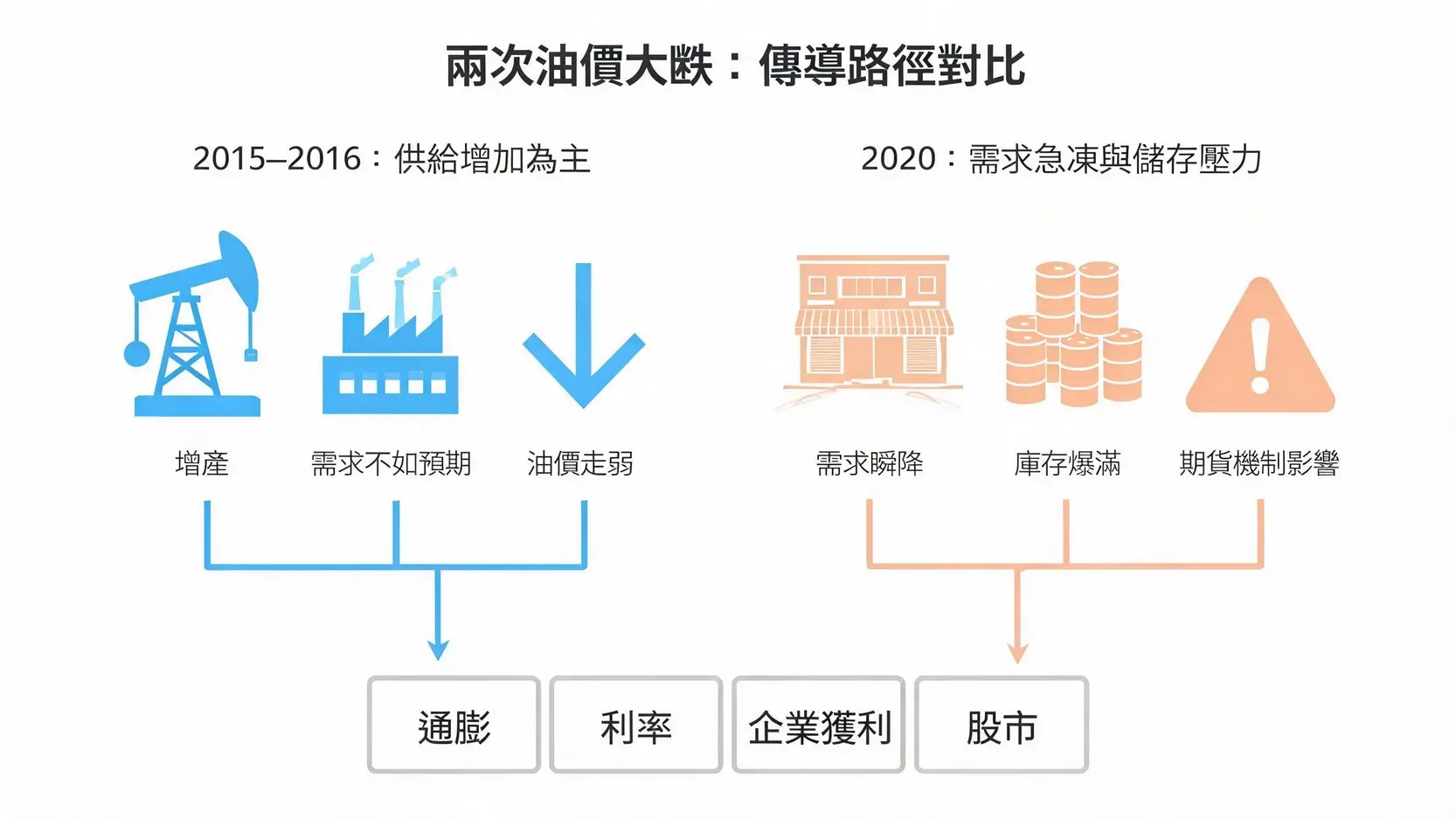

The most effective way to forecast oil prices is to break them down into “supply, demand, inventories, and financial conditions”. On the supply side, OPEC+ policy and non-OPEC production can be tracked; on the demand side, monthly reports from authoritative institutions such as the IEA and economic indicators of major economies can be monitored; on the inventory side, commercial inventories and floating storage changes should be watched; for financial conditions, the US dollar and interest rates should be observed. When demand is revised downward, inventories rise, and the US dollar strengthens at the same time, the probability of a sharp decline in international oil prices increases.

Does War Always Lead to Higher Oil Prices? Why Do Prices Sometimes Fall Instead?

Not necessarily. What the market trades is the “possibility of actual supply disruption” and the “risk premium”. If the conflict does not affect major production areas or key shipping routes, or if the market expects the situation to remain controllable, the risk premium may be priced out, causing oil prices to fall instead. In addition, if the war triggers concerns over global growth and lowers demand expectations, this may also outweigh supply risks and become one of the reasons oil prices fall.

Should Ordinary Investors Buy Crude Oil ETFs When Oil Prices Fall?

You must first confirm what type of crude oil ETF you are buying: whether it tracks spot prices, front-month futures, or uses a different futures rollover strategy can lead to significant performance differences. If the market is in a futures “contango” structure (where longer-dated contracts are more expensive than near-month contracts), holding a front-month futures ETF over the long term may be eroded by rollover costs. When oil prices halve, violent volatility is more likely to occur. Without an understanding of the instrument structure and risk control, investors should not enter the market simply because prices have “fallen deeply”.

Which Groups in Taiwan Stocks and Malaysian Stocks Are More Sensitive to a Halving in Oil Prices?

Generally speaking, the impact of falling oil prices will first be reflected in cost-side groups such as transportation, aviation, and some chemical and petrochemical sectors. In contrast, if the market is worried about weakening demand, energy and resource-related stocks, as well as targets with higher correlation to the economic conditions of oil-producing countries, will face more pressure. For Taiwan stocks, the New Taiwan dollar exchange rate and export cycle should also be observed; for Malaysian stocks, attention should be paid to energy weighting and exchange rate changes.

Is a Sharp Drop in Oil Prices a Tonic for Cooling Inflation or a Poison for Economic Recession?

Both scenarios are possible. If oil prices fall due to increased supply, it cools inflation and supports consumption, making it more of a “tonic”; however, if a collapse in demand causes international oil prices to fall sharply, inflation may decline, but corporate revenue and employment may also come under pressure, making it more of a “poison”. The key judgment lies in whether demand data and corporate earnings expectations are weakening at the same time.

Conclusion

A halving in oil prices is not simply commodity price news, but a “macro switch” that affects inflation, interest rates, exchange rates, and industry profits. When breaking down the reasons oil prices fall, the three most common main lines are: supply-demand imbalance, changes in geopolitical risk premiums, and long-term demand pressure under the energy transition. When facing a sharp decline in international oil prices, instead of rushing to guess the bottom, it is better to first place your holdings into the beneficiary/victim list for stress testing, then use instrument structure (whether the ETF has rollover losses) and risk control (scaling in, stop-losses, and position limits) to keep the uncertainty of oil price forecasts contained.