Semiconductor Export Tailwinds vs. Headwinds Under a Hawkish Shift: The Two-Column Comparison Investors Need Most

How the AI-Led Export Boom Drives Business Activity

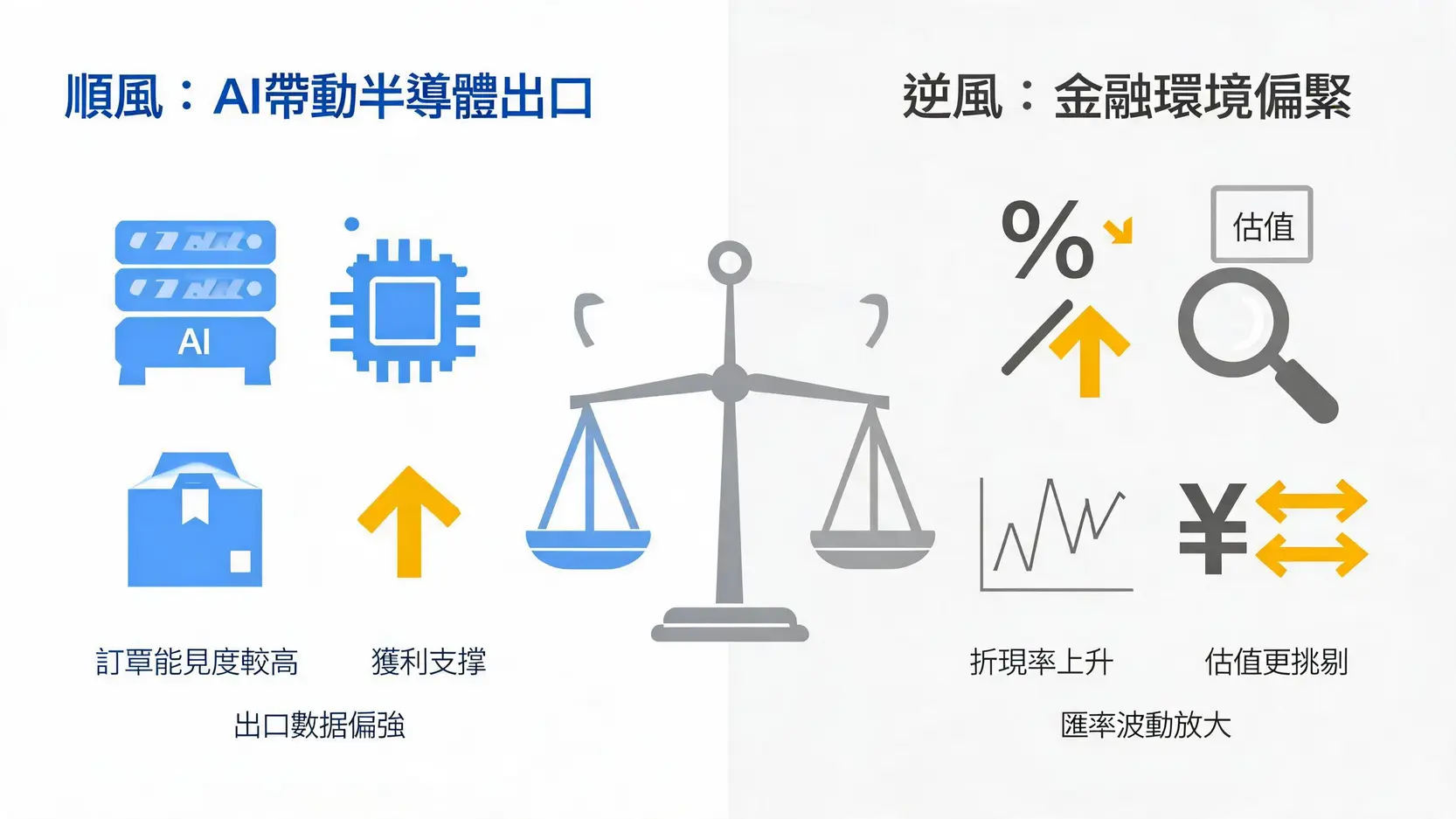

AI servers, memory, advanced packaging, and high-bandwidth demand have made supply chain order visibility relatively strong. The practical significance for investors is that even if interest rates stay high, as long as export momentum remains strong, corporate earnings may be able to offset part of the valuation pressure.

However, it is important to note that the semiconductor cycle has always had two major challenges: “price volatility” and “inventory adjustments”. When the Bank of Korea turns hawkish and the financial environment tightens, any slight disturbance may magnify stock price volatility. So rather than only watching news headlines, the more practical approach is to track monthly export value, unit price trends, and major customers’ capital expenditure, using data to judge how far the boom can go.

Containing Household Debt and High-Leverage Vulnerability

When discussing “Asian central banks”, financial stability cannot be ignored: in an environment of high housing prices and high leverage, what central banks fear most is “inflation has not yet been suppressed, but the financial system runs into trouble first”. Therefore, hawkish language is often accompanied by warnings about household debt and housing market risks. This point can be directly referenced from the Bank of Korea’s official explanations and decision texts on monetary policy and financial stability: Monetary Policy Decision & Opening Remarks to the Press (Bank of Korea).

For investors, this message represents two things:

- High interest rates may last longer: the “ceiling” for stock valuations can easily be capped.

- The gap between financial stocks and domestic demand stocks will widen: asset quality and benefits from interest rate spreads do not necessarily move in the same direction, so investors should select companies rather than sectors.

Keyword variations here can naturally include: South Korea household debt risk, financial stability, and a high-interest-rate environment, avoiding repetitive keyword stuffing.

The Chain Effect of the Bank of Korea’s Hawkish Turn on Other Asian Central Banks: The Triangle of Oil Prices, the US Dollar, and Capital Flows

Many people only look at South Korea, but the bigger story lies in the “demonstration effect”: once the Bank of Korea’s tone turns hawkish, other Asian central banks usually become more cautious when facing exchange rates and inflation. The reason is not complicated: capital is mobile, and interest rate differentials and exchange rate expectations affect foreign capital allocation.

Oil Prices and a Strong US Dollar Force Asian Central Banks to Pause Rate Cuts

When oil prices rise and the US dollar stays strong, most Asian economies face “imported inflation” and “currency depreciation pressure”. Even if domestic demand is not very hot, central banks do not dare to cut rates rashly, because rate cuts may weaken exchange rates further and make imported inflation harder to control. This is why you see the market expecting rate cuts, while central bank language continues to emphasize “observation and maintaining flexibility”.

For investors in Taiwan and Malaysia, the practical reading of this environment is: funding costs may not fall quickly, and stock market valuations are unlikely to move upward smoothly all the way. At this stage, positioning is more suitable for screening targets based on “cash flow, gross margin, and defensiveness”, rather than chasing high-leverage themes.

Foreign Capital Rebalancing across Asian Emerging Markets

When the Bank of Korea turns hawkish and US interest rates remain relatively high, foreign capital usually does two things: shift holdings from “higher volatility” to “greater certainty”, and reassess exchange rate risks. This also explains why, even within the same semiconductor theme, South Korea’s stock market can sometimes be more sensitive than other markets: foreign positioning, exchange rate volatility, and policy signals are intertwined.

To summarize the chain effect in one sentence: the Bank of Korea’s hawkish turn raises the discount rate for Asian risk assets, while capital becomes more inclined toward companies with “visible earnings”. This is also one common background behind the “cooling of South Korea’s stock market”.

Investor Playbook: A 3-Step Checklist for South Korea’s Stock Market and Semiconductor ETFs Under the Bank of Korea’s Hawkish Turn

What the market fears most is not “hawkishness”, but not knowing where that hawkishness will have an impact. The following breaks down the risks in three steps, applicable to common cross-market allocations among investors in Taiwan and Malaysia (including US stocks, Asian technology, and ETFs).

- Step 1: Watch exchange rates and funding conditions: If the Korean won fluctuates sharply, foreign capital is more likely to reduce exposure in the short term, making South Korea’s stock market more prone to volatility.

- Step 2: Watch semiconductor exports and earnings visibility: Strong export data means fundamentals can withstand part of the interest rate headwind. Otherwise, be careful of a “double hit” (valuation + earnings).

- Step 3: Watch the speed of change in interest rate expectations: It is not that high interest rates necessarily cause declines, but that the gap between “the market originally expected rate cuts, but they failed to materialize” is most likely to trigger a correction.

Keyword variations can be naturally inserted here: the Bank of Korea’s hawkish stance, risks of South Korean semiconductor ETFs, and foreign capital flows.

FAQ

Will the Bank of Korea’s hawkish turn cause South Korea’s stock market to crash?

A: Not necessarily. A hawkish turn usually means higher funding costs and more difficulty for valuations to rise, which can easily cause pullbacks in high-valuation sectors and index volatility. However, whether it becomes a “crash” still depends on whether corporate earnings weaken at the same time, whether foreign capital withdraws significantly, and whether global risk events intensify.

What is the forecast for the Korean won over the next few months?

A: The Korean won is often driven by “US dollar strength, oil prices, and foreign risk appetite”. The Bank of Korea’s hawkish turn may provide short-term support, but if the US dollar continues to strengthen or geopolitical risks intensify, the Korean won may still see greater volatility. In practice, it is more worthwhile to watch “volatility” than to guess a single direction.

Is there risk in investing in South Korean semiconductor ETFs now?

A: Yes. The main risks are valuation volatility and exchange rates, not just the industry cycle. Although AI demand provides medium-term support, when the Bank of Korea turns hawkish and interest rates remain elevated, the market discounts “growth expectations” more strictly, which may amplify ETF drawdowns.

Why does the Bank of Korea’s hawkish turn affect Asian central bank policies?

A: Because the common constraint facing Asian central banks is “exchange rates and capital flows”. When the Bank of Korea turns hawkish, it signals rising awareness of interest rate differentials and exchange rate defense, making other central banks more cautious about rate cuts to avoid pressure on their currencies and worsening imported inflation.

How can retail investors track Bank of Korea policy signals without being swayed by news narratives?

A: Prioritize “official policy decision statements and key points from press conferences” before looking at secondhand interpretations. First-hand information, such as the Bank of Korea’s policy decisions and opening remarks, can be found in full on its public pages: Bank of Korea Policy Decision Explanation.

Conclusion

The core of the Bank of Korea’s hawkish turn is not “talking down the economy”, but shifting the policy focus back to inflation control and financial stability: imported inflation caused by oil prices and a strong US dollar, together with household debt and housing market leverage, makes it harder for the central bank to pivot easily toward easing. This will put pressure on South Korea’s stock market valuations and increase volatility. At the same time, if semiconductor exports remain strong under AI demand, fundamentals may still support the market’s downside.

The three indicators most worth watching next are clear: South Korea’s AI and semiconductor export data, the relative strength of the Korean won and the US dollar, and foreign capital flows. Once you understand these three lines, no matter how the market turns, you will be less likely to be shaken out.