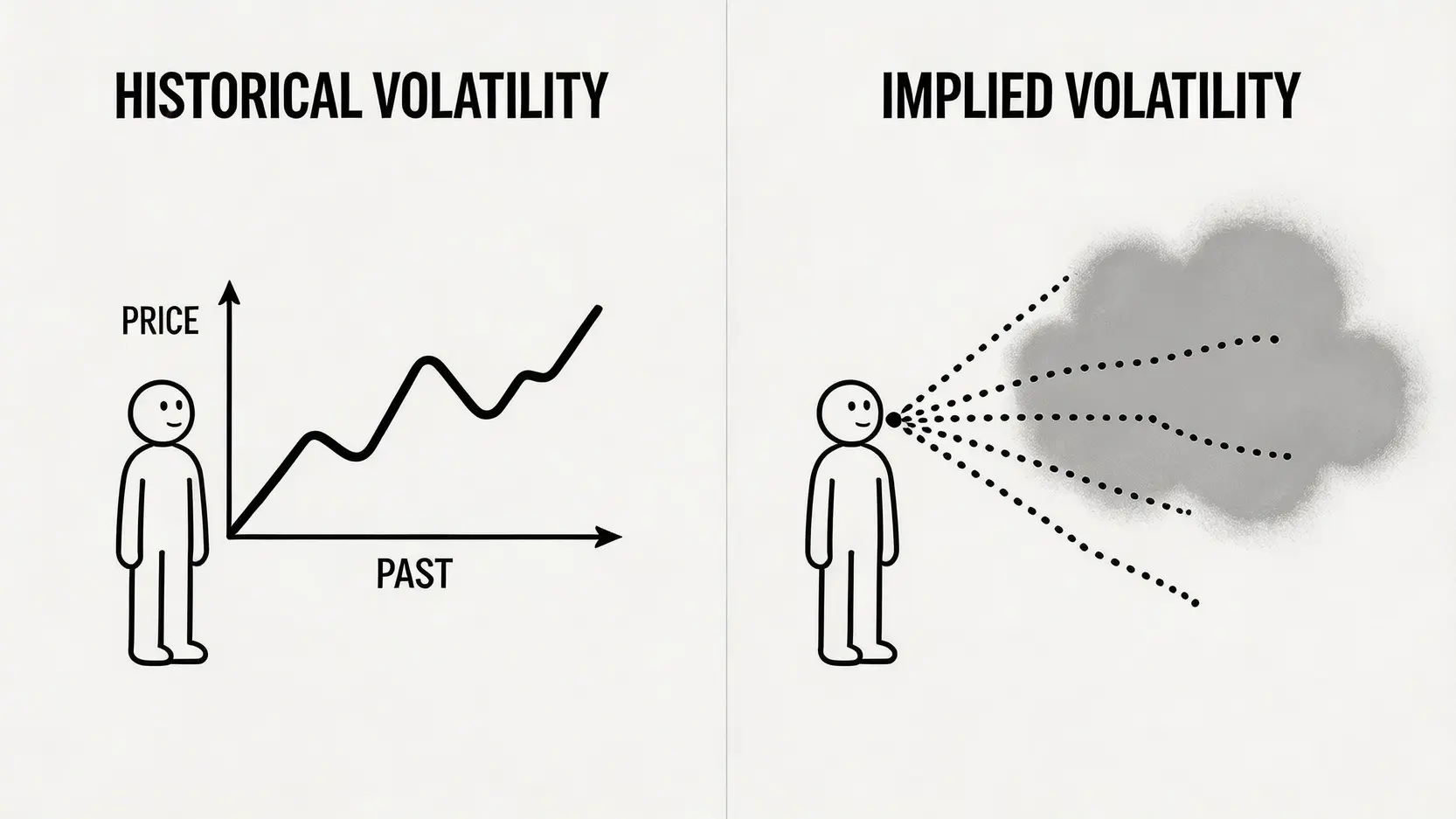

HV looks at the past and is objective data; IV looks at the future and reflects market expectations.

[Comparison Summary] A Table to Clearly Understand the Key Differences Between IV and HV

To help you understand more clearly, we have summarized the key differences between IV and HV in the table below:

| Characteristic |

Implied Volatility (IV) |

Historical Volatility (HV) |

| Data Source |

Current options market price (premium) |

Historical price of the underlying asset |

| Time Dimension |

Forward-looking (expectation of the future) |

Backward-looking (summary of the past) |

| Nature |

Subjective, influenced by market sentiment and news events |

Objective, based on historical statistical data |

| Primary Use |

Evaluate whether options are expensive or cheap, and develop trading strategies |

Measure historical risk and build quantitative models |

Understanding and Applying the Concept of Implied Volatility Calculation

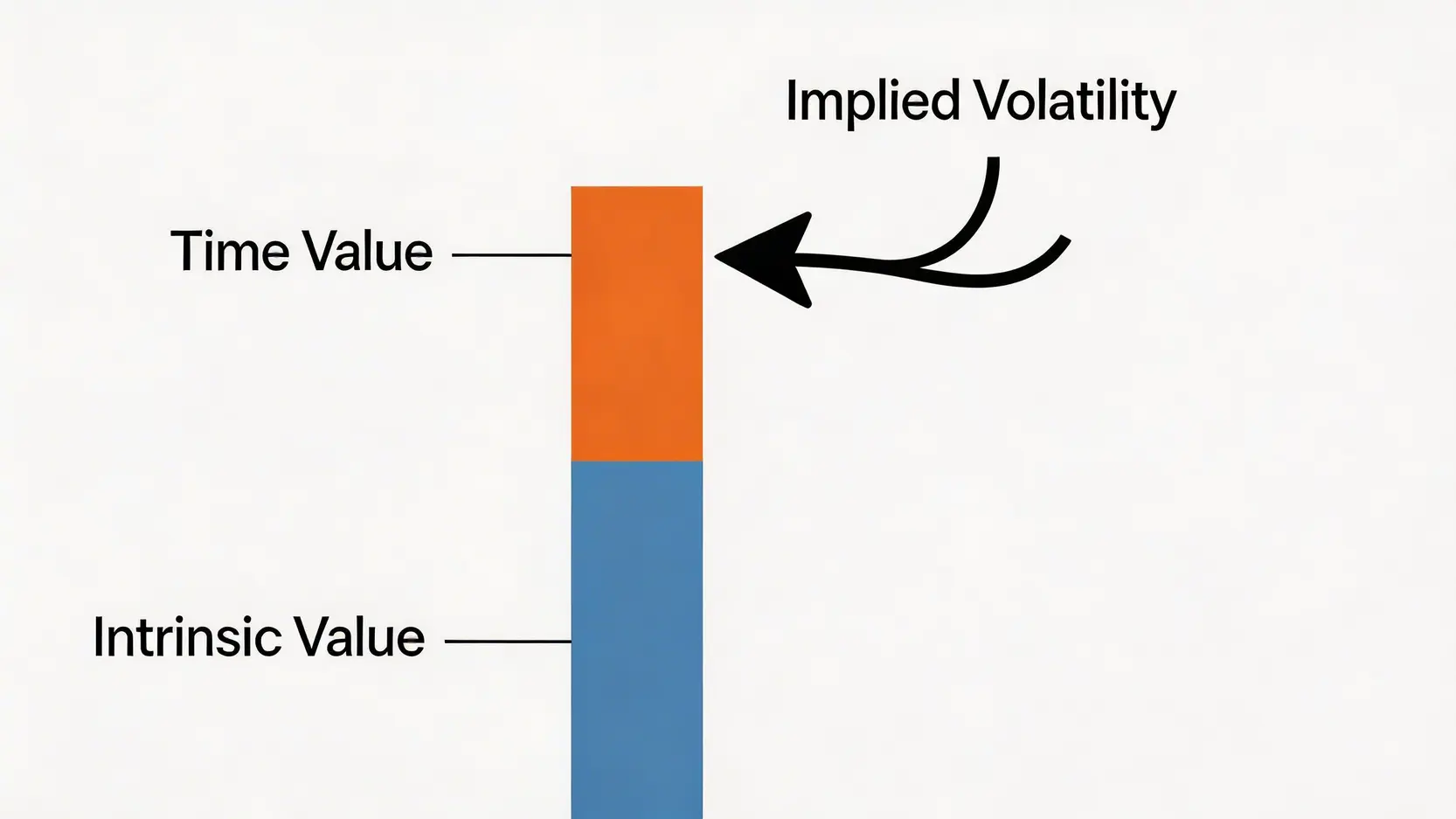

After understanding the basic concept of implied volatility calculation, the next key step is how to interpret and apply it in practice. IV itself has no absolute good or bad value. High or low levels both contain different trading opportunities and risks.

What Does High IV Represent: An Opportunity for Huge Profits or a Price Trap?

When IV surges, it usually means that a major market event is about to occur, such as:

- Earnings releases from companies

- Announcement of new drug clinical trial results

- Federal Reserve interest rate decision meetings

- Major geopolitical events

At this point, option premiums become very expensive. For option “sellers” (Sell Call / Sell Put), this is an excellent opportunity, because they can collect higher premiums. As long as the post-event price movement is not as extreme as expected, they can steadily earn time value. However, for “buyers”, high IV is a trap because the entry cost is extremely high. Once the event passes and IV drops sharply, even if the direction is correct, losses may still occur due to the subsequent “IV Crush”.

Insights From Low IV: When Is It a Good Time to Deploy Buyer Strategies?

When the market is calm and IV is at relatively low levels, option premiums are comparatively cheap. This is a more favorable environment for option “buyers” (Buy Call / Buy Put). You can establish positions at lower cost to speculate on potential large price movements in the future. If market volatility increases afterward and IV rises, you may have the opportunity to profit from both “directional gains (Delta profit)” and “IV expansion gains (Vega profit)”, achieving dual returns.

Introduction to Implied Volatility Calculation: A Brief Look at How the Black-Scholes Model Derives IV

Most traders do not need to manually calculate IV, as trading software provides it directly. However, understanding the underlying principle helps deepen your comprehension. The most classic option pricing model in the industry is the Black-Scholes Model, which considers five variables to calculate the theoretical option price:

- Underlying asset price

- Strike price

- Risk-free interest rate

- Time to expiration

- Volatility

In practical application, the first four variables are known, and the market price of the option is also known. Therefore, we can substitute the market price into the formula and reverse-solve for the only unknown variable, “volatility”. This volatility implied by the market price is what we call IV.

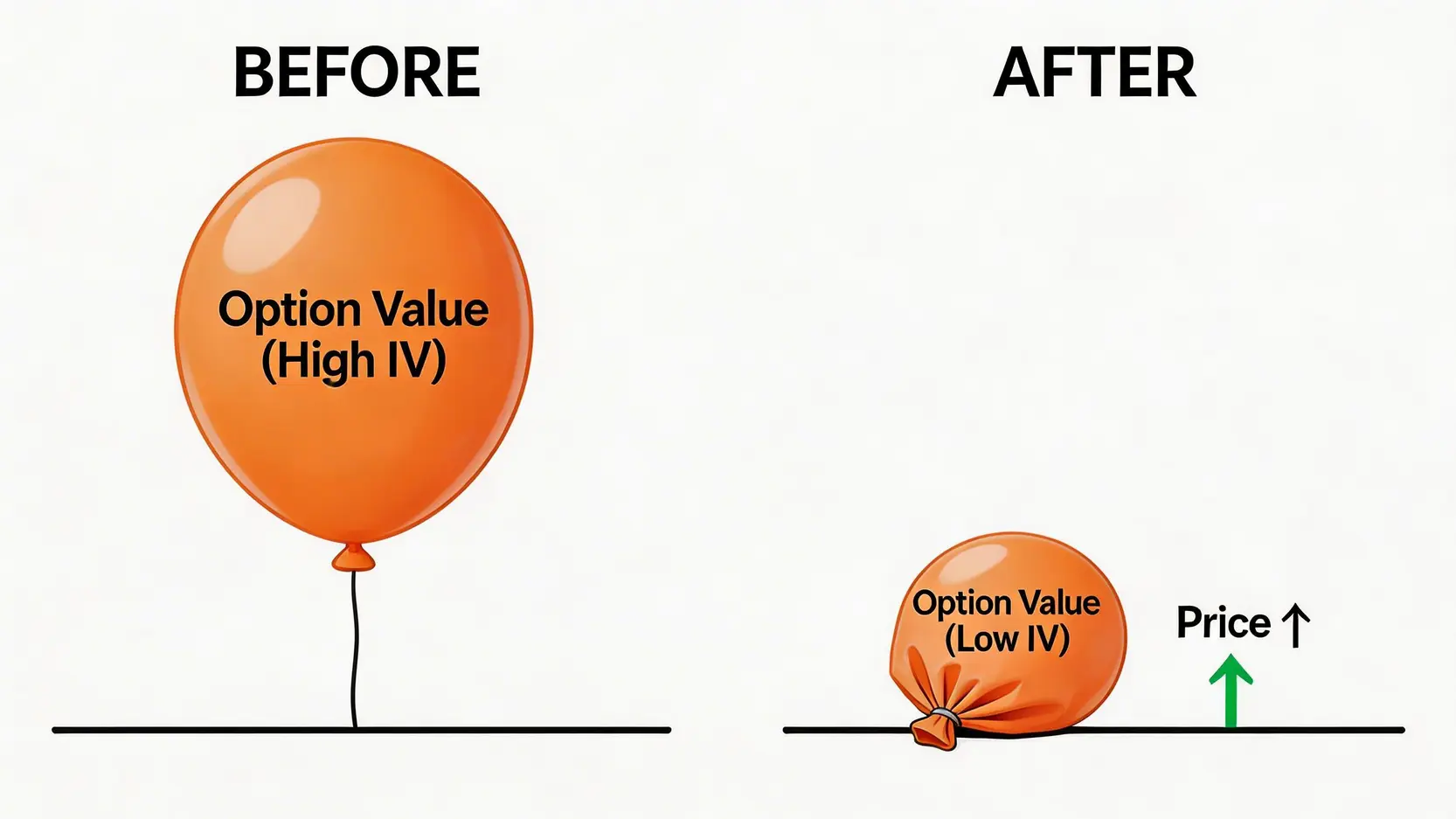

The Terrifying Value Killer: What Is IV Crush (Implied Volatility Collapse)?

Once you understand IV, you must also understand its most dangerous aspect, IV Crush. This is the biggest nightmare for many beginner options traders and the main reason behind the situation of “getting direction right but still losing money”.

What IV Crush Means: Why Does It Vanish After Earnings and Other Major Events?

IV Crush refers to the sudden and significant drop in implied volatility after a major uncertainty event is resolved. Imagine that before an earnings announcement, the market is full of speculation and uncertainty. No one knows whether the result will be good or bad. This “unknown” pushes IV higher, making option prices expensive.

However, once the earnings are released, all uncertainty disappears instantly. Whether the result is better or worse than expected, the “fog” covering the market is lifted. At this point, IV quickly falls back to normal levels, causing option time value to evaporate instantly. This is IV Crush.