Straddle (Long Straddle) vs Strangle (Long Strangle) Core Structural Differences

1. Premium Cost: Which Strategy Is Cheaper?

Conclusion: Long Strangle is cheaper.

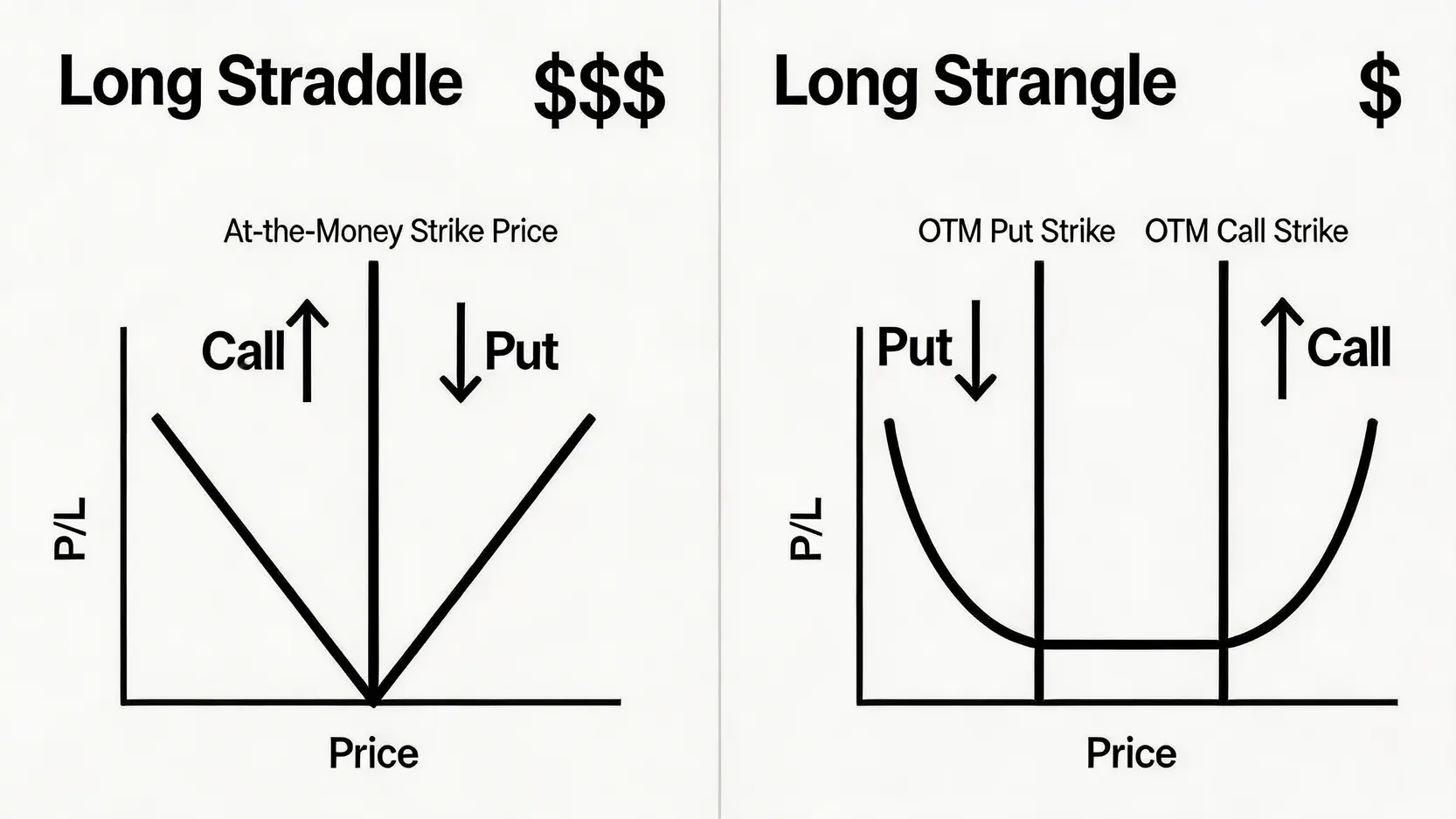

This is the most significant difference between the two strategies. A Long Straddle uses at-the-money (ATM) options, which have higher intrinsic and time value, making them more expensive. In contrast, a Long Strangle uses out-of-the-money (OTM) options, whose value consists almost entirely of time value, making them significantly cheaper. For investors with limited capital or those seeking to reduce maximum risk, the Strangle is clearly more advantageous.

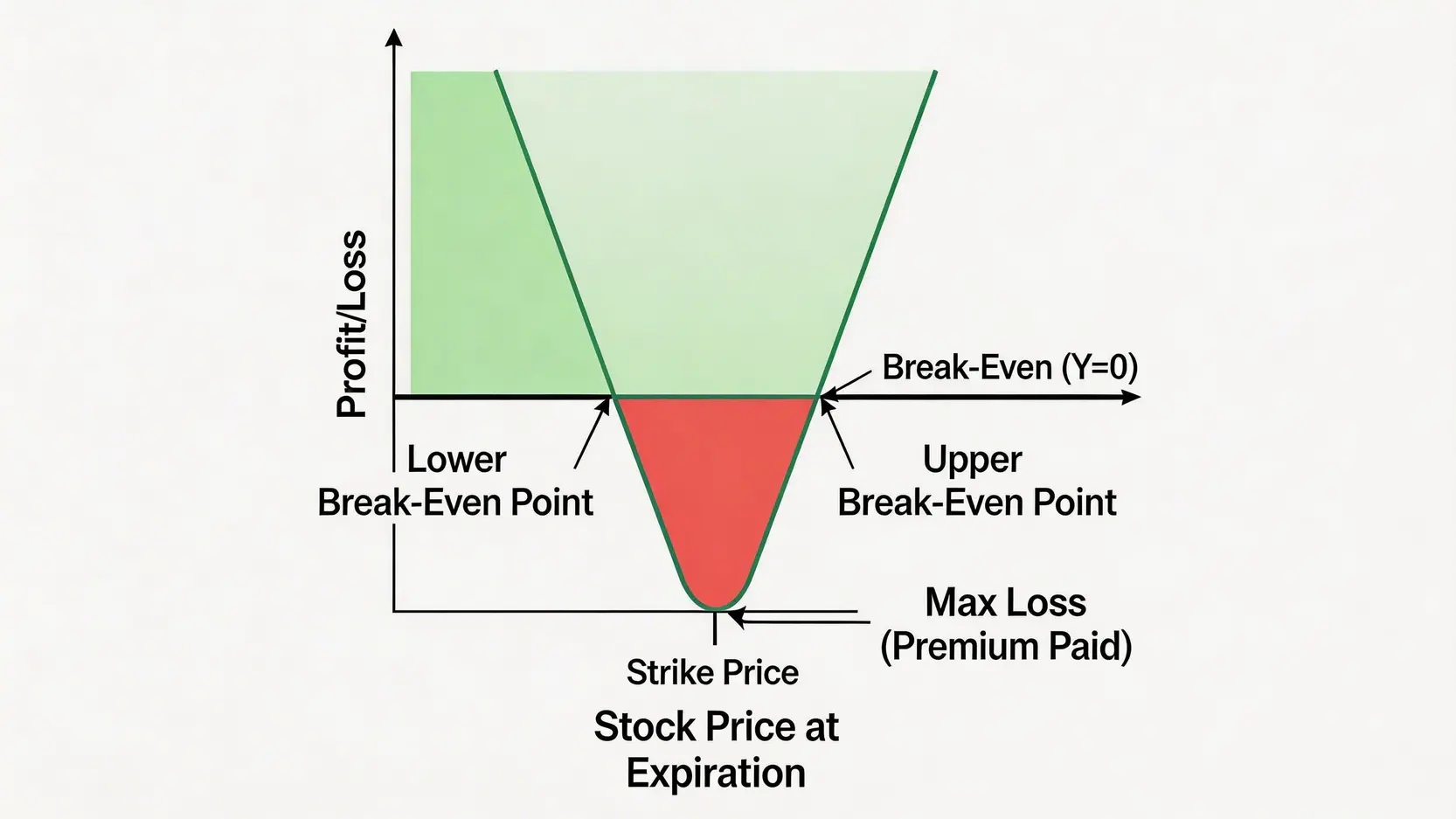

2. Break-Even Points: Which Strategy Is Easier to Profit From?

Conclusion: Long Straddle has a lower profit threshold.

Because the Straddle concentrates both strikes at the same point (current stock price), its break-even range (strike price ± total premium) is relatively narrow. The Strangle, however, uses two different strike prices, creating a wider distance between break-even points. This means that under a Straddle strategy, the stock does not need to move as much to start generating profit.

3. Profit Potential: Differences in Payoff Curves

Conclusion: Both have theoretically unlimited profit potential, but different starting points.

Although both strategies have theoretically unlimited maximum profit, their payoff curves differ. The Straddle has a sharper “V” shape, meaning profits accelerate rapidly once the break-even point is crossed. The Strangle has a flatter “U” shape, meaning losses remain steady before the price breaks the strikes, and only after crossing the break-even points does profit begin.

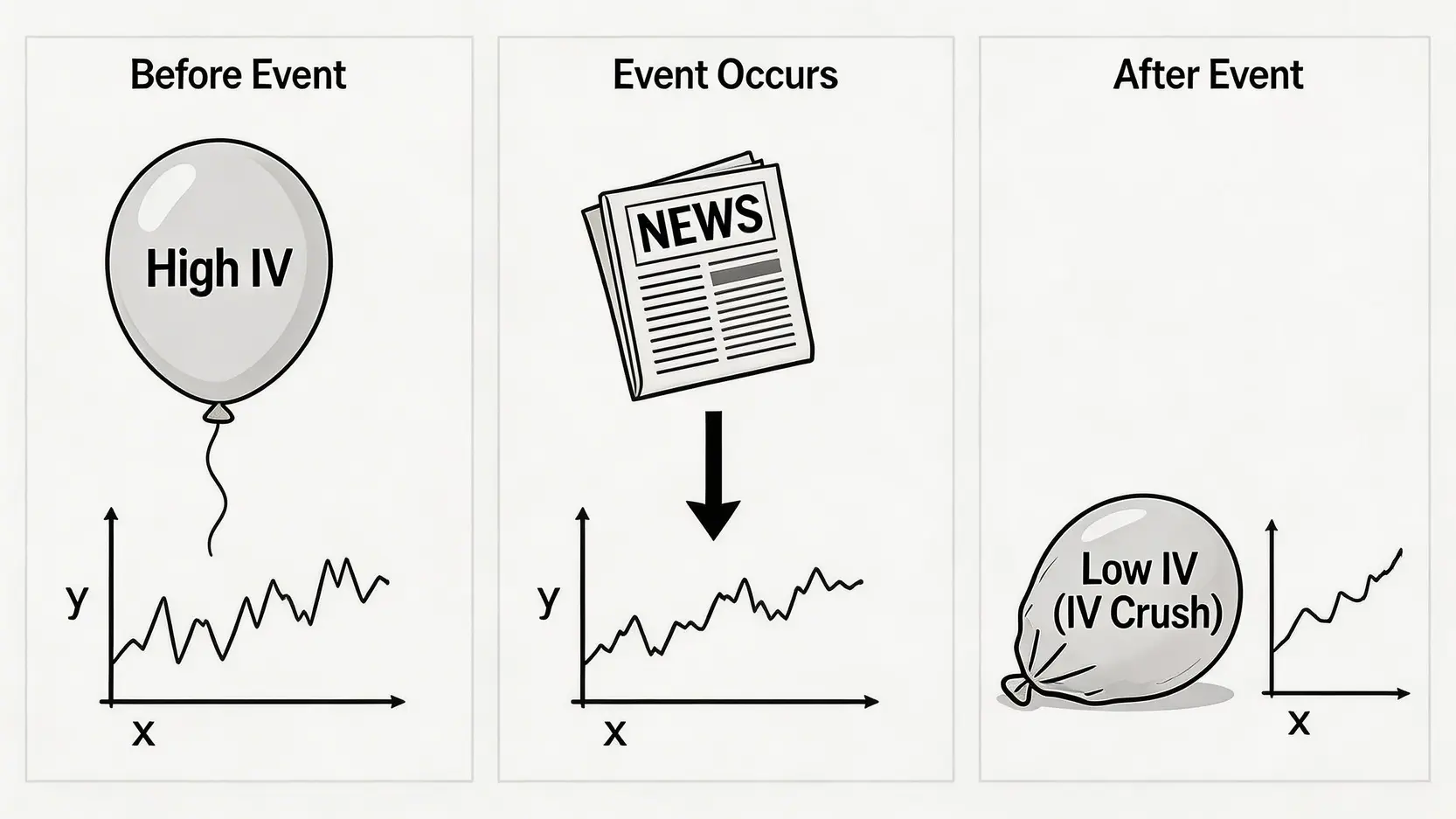

4. Volatility Sensitivity: Impact of IV on the Strategy

Conclusion: Both are extremely sensitive to implied volatility (IV).

Long Straddle and Long Strangle are both “long volatility” strategies, and their value is highly dependent on market expectations of future volatility, namely implied volatility (IV).

- IV increase: Beneficial for both strategies. Even if the stock price does not move, an increase in expected volatility can raise option prices and potentially generate profit.

- IV crush: Extremely unfavorable for both strategies. This is the biggest trap in earnings trades and will be discussed in detail later.

5. Summary Comparison Table: A Quick Way to Understand Which Strategy to Use

| Comparison Dimension |

Long Straddle |

Long Strangle

|

| Structure |

Buy ATM Call + Buy ATM Put (same strike price) |

Buy OTM Call + Buy OTM Put (different strike prices) |

| Cost |

Higher |

Lower |

| Profit Threshold |

Lower (break-even points are closer) |

Higher (break-even points are further apart) |

| Maximum Risk |

Total premium paid (higher amount) |

Total premium paid (lower amount) |

| Suitable Scenario |

Expecting large volatility but uncertain direction |

Expecting extremely large volatility and wanting to control cost |

| Sensitivity to IV Crush |

Very high |

Very high |

【Practical Guide】How to Apply It in Earnings Options Strategies?

Earnings season is the ideal time to apply these two strategies. When a company’s results or guidance significantly exceed or fall short of expectations, the stock often experiences intraday gaps of 10%, 20%, or even more. This kind of sharp but uncertain volatility is exactly where Straddle and Strangle strategies come into play.

Why Is Earnings Season Suitable for Volatility Strategies?

Before earnings are released, the market is filled with uncertainty, causing implied volatility (IV) in options to rise significantly. Investors are willing to pay higher premiums to hedge risk or speculate. This creates an ideal environment for volatility strategies. When you buy a Straddle or Strangle, you are essentially buying this “uncertainty”. As long as the actual post-earnings move exceeds market expectations, you have the opportunity to profit. For more basic options knowledge, you can refer to this Options Beginner Guide.

Practical Steps: How to Choose the Right Strike Price and Expiration Date

- Choosing the expiration date: Select the expiration date immediately after the earnings announcement. For example, if a company reports earnings after market close on Wednesday, you may choose options expiring on Friday of the same week. This allows you to capture the earnings impact while minimizing time decay (Theta).

- Choosing the strike price:

- Long Straddle: Choose the strike price closest to the current stock price (ATM).

- Long Strangle: Choose out-of-the-money (OTM) strike prices. A common approach is to reference the expected move implied by the options chain (usually provided by brokers), and set the call and put strikes at the edges of that expected range.

- Calculate cost and break-even points: Before entering the trade, always calculate your total cost (maximum risk) and both break-even points. Ask yourself: “Do I really expect the stock to move beyond this range?”

The Biggest Trap: How to Manage the Risk of Post-Earnings IV Crush (Implied Volatility Collapse)

IV Crush is the biggest enemy of all earnings strategies. Once earnings are released and uncertainty is removed, implied volatility (IV) collapses rapidly like a deflating balloon, regardless of whether the result is good or bad. This causes both call and put option prices to drop sharply.