Latest OTC Derivatives Capital Threshold and Margin Framework

Additional Margin Requirements for Non-Centrally Cleared OTC Derivatives

Within the complex OTC marketplace, bilateral contracts that are not cleared through a Central Counterparty (CCP) often carry significant counterparty credit risk. Consequently, the new margin requirements for non-centrally cleared OTC derivatives have become a central pillar of the regulatory reform. Under the latest margin guidelines, counterparties engaging in such higher-risk OTC transactions must not only exchange variation margin daily, as was previously required, but must also post sufficient Initial Margin (IM) at the outset of the transaction.

Initial Margin must be calculated using internationally recognized standardized quantitative models. More importantly, these substantial margin amounts must be held in fully segregated third-party custody accounts to achieve complete bankruptcy remoteness. This transformative requirement significantly increases the funding costs associated with bilateral OTC transactions, encouraging market participants to migrate standardized contracts toward central clearing platforms when selecting investment tools and designing hedging strategies.

Using RegTech to Automate Capital Adequacy Assessment

Given the exponential increase in the complexity of derivatives capital threshold calculations and the frequent margin calls resulting from daily mark-to-market requirements, traditional manual processes are no longer sufficient. Forward-looking financial institutions must embrace digital transformation and actively invest in advanced Regulatory Technology (RegTech) solutions.

Through automated systems, firms can capture cross-asset transaction data in real time and continuously calculate capital adequacy ratios and margin shortfalls with precision. These intelligent platforms incorporate sophisticated risk-trigger mechanisms that can alert management before capital ratios approach regulatory thresholds and can even automatically generate regulatory reports in formats prescribed by the SFC. Institutions that establish efficient compliance data processing capabilities early will not only avoid substantial regulatory penalties but also gain opportunities to optimize capital allocation and expand market share.

Frequently Asked Questions About Hong Kong’s OTC Derivatives Regulatory Reforms

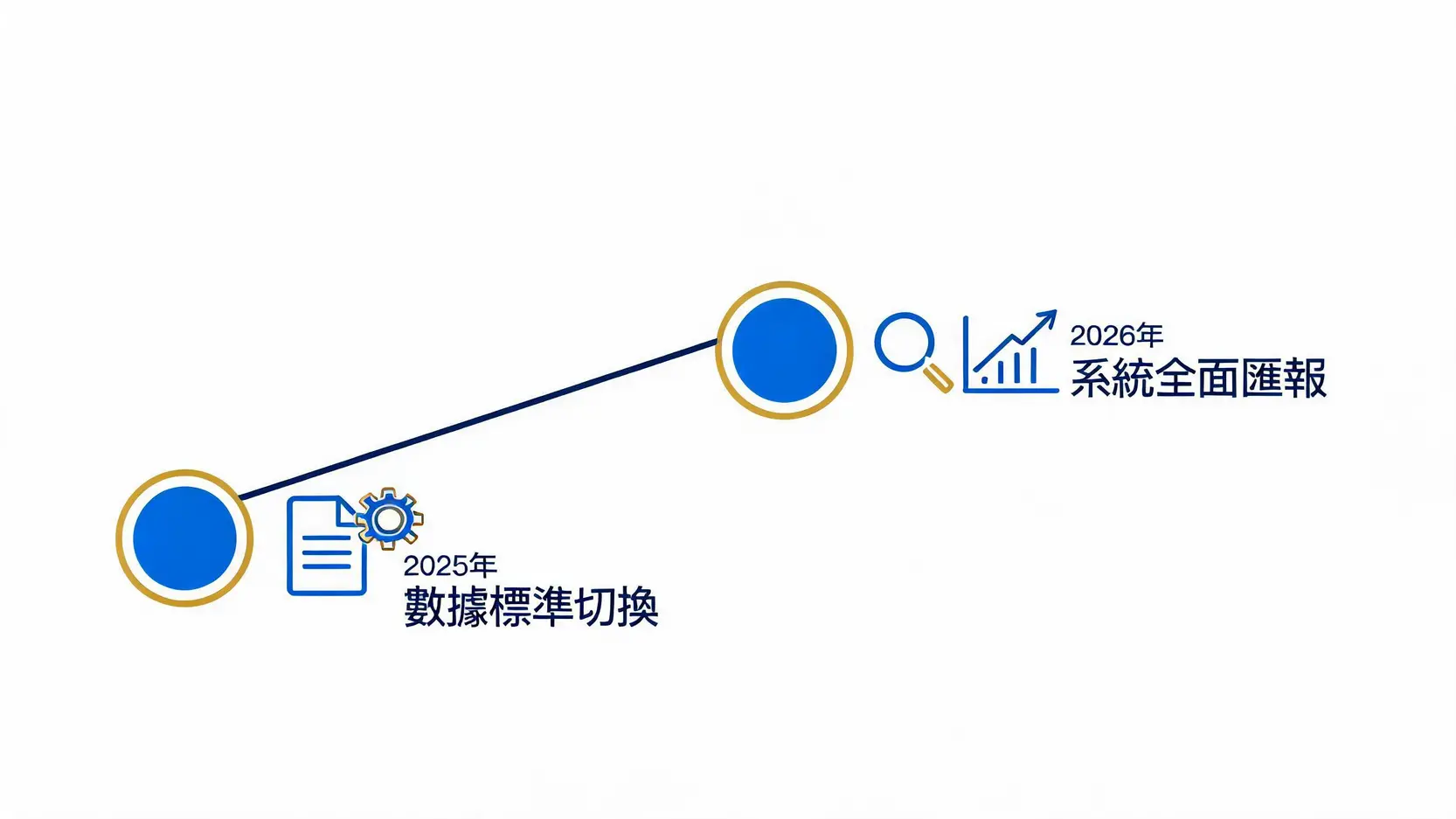

When Do the Hong Kong OTC Derivatives Regulatory Reforms Officially Take Effect?

The requirements are being implemented in phases. The “ISO 20022” system migration has already been completed, while further enhancements relating to historical transaction reporting, valuation reporting, and margin reporting became effective progressively from March 16, 2026. Institutions are advised to closely monitor announcements issued by the SFC and HKMA throughout the transition period.

What Types of OTC Derivatives Are Covered by the New Rules?

The scope is extensive and includes, but is not limited to, interest rate swaps, Non-Deliverable Forwards (NDFs), Credit Default Swaps (CDSs), and various non-standardized equity and commodity derivatives. Most transactions involving Hong Kong legal entities or booked within Hong Kong will fall within the regulatory perimeter.

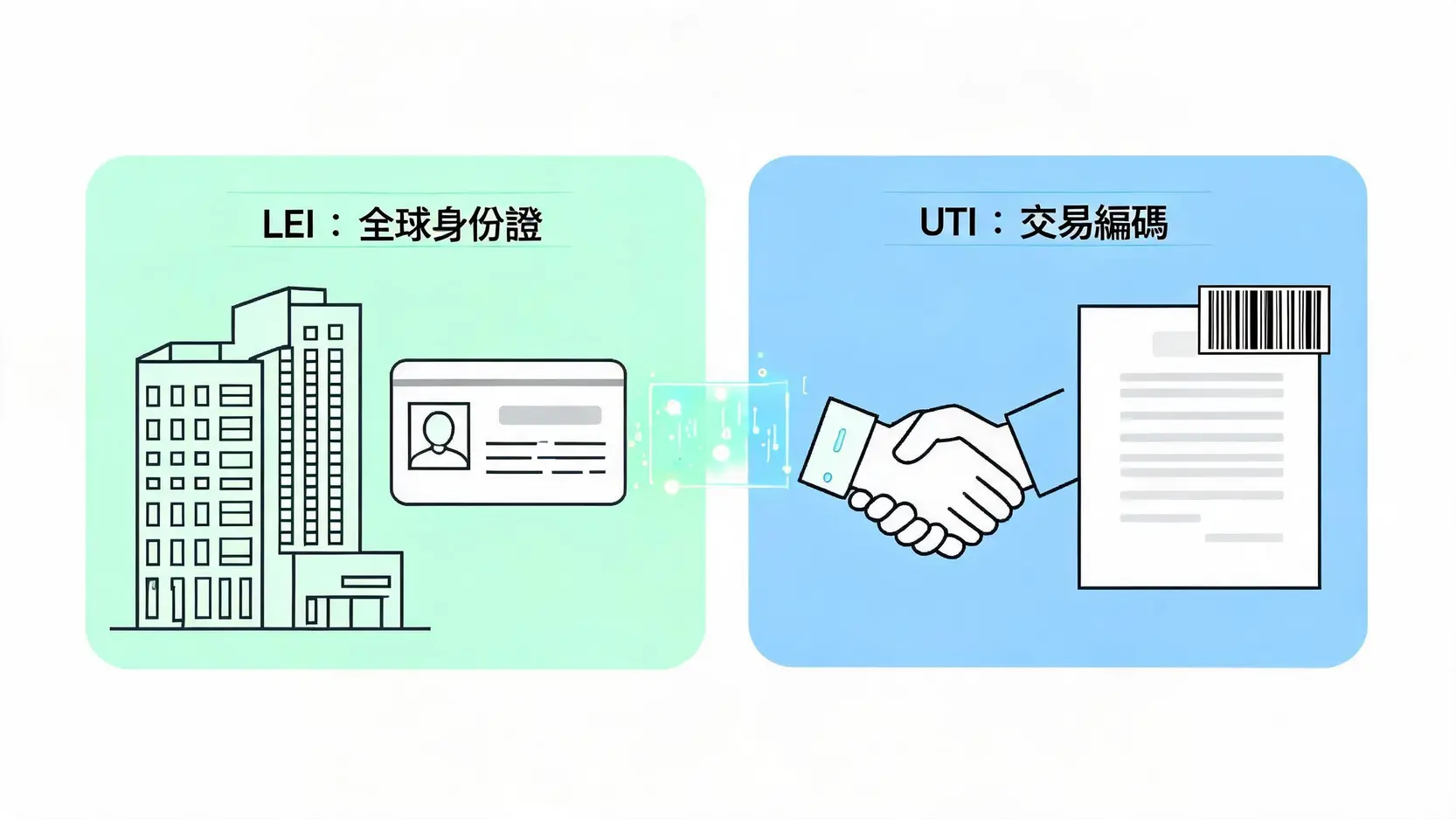

What Are the Consequences of Failing to Obtain a UTI or LEI Within the Required Timeframe?

The absence of a valid Legal Entity Identifier (LEI) or Unique Transaction Identifier (UTI) will result in transaction reports being rejected by the Hong Kong Trade Repository system. This constitutes a compliance breach and may lead to substantial financial penalties, public reprimands, or even restrictions on conducting new OTC derivatives business.

How Should Institutions Address the Funding Pressures Created by the New Margin Requirements?

To manage the bilateral margin requirements applicable to non-centrally cleared OTC derivatives, institutions should optimize collateral management systems, improve the utilization of high-quality liquid assets (such as government bonds) and consider using RegTech solutions to monitor exposures dynamically. In addition, migrating portions of their business toward centrally cleared standardized contracts may help reduce funding costs.

Conclusion

The comprehensive implementation and continued enhancement of Hong Kong’s OTC derivatives regulatory reforms marks a historic milestone in the market’s pursuit of greater transparency and stronger resilience against systemic risk. From the far-reaching mandatory LEI and UTI reporting framework to the stringent tangible capital and margin requirements specifically designed to mitigate liquidity crises, every aspect of the reform presents a profound test of financial institutions’ operational flexibility and risk management capabilities.

As 2026 represents a pivotal year for compliance implementation and system modernization, institutions must recognize that early adoption of advanced RegTech solutions, comprehensive restructuring of internal data governance frameworks, and proactive adaptation to new capital requirements are not merely defensive measures designed to avoid substantial regulatory fines. Rather, these initiatives form the foundation for optimizing capital efficiency and maintaining long-term competitiveness in an increasingly complex global financial marketplace. Now is the time to review your organization’s transaction workflows and underlying data infrastructure to ensure a smooth transition into this new era of OTC market compliance!