Dynamic Risk Scoring Mechanisms: Millisecond-Level Real-Time Detection and Defense

Further Reading (Highly Recommended)

A New Era of Cryptocurrency Exchange Regulation in Hong Kong: Compliance Strategies and In-Depth Analysis of the Market Ecosystem

AI Predicting Foreign Exchange Turning Points: A Practical Guide to Neural Network Trading Models

Strong Regulatory Promotion and Practical Applications of Cloud-Based AML Solutions

For many small and medium-sized financial institutions and emerging Virtual Asset Service Providers (VASPs), developing a complete AML system internally is prohibitively expensive. As a result, numerous high-quality cloud-based AML solutions (such as platforms like ZOLOZ, have emerged in the market). These solutions not only align with regulatory authorities’ push for AML automation within banks and financial institutions, but also provide cost-effective alternatives for the industry.

Behavioral Profiling for High-Frequency Anonymous Transactions Beyond Traditional Banking

The money laundering risks faced by virtual asset exchanges are far more complex than those encountered by traditional banks. The anonymity of cryptocurrencies and the high-frequency nature of cross-chain transactions make fund tracing significantly more challenging. Advanced cloud-based AML solutions integrate blockchain analytics technology to perform in-depth “behavioral labeling” of wallet addresses.

Whether the funds are linked to dark web transactions, mixers, or ransomware-related activities, these systems can rapidly identify high-risk on-chain behavior through large-scale data analysis and matching. This enables exchanges to effectively block suspicious transactions the moment funds are deposited or withdrawn, preventing their platforms from becoming channels for illicit money laundering activities. This is also one of the most compelling applications of regulatory technology (RegTech) in the virtual asset sector.

Seamless Integration With KYC and KYB Systems for Full Lifecycle Monitoring

Compliance reviews should not operate in isolated silos. High-quality big data monitoring systems can integrate seamlessly with existing Know Your Customer (KYC) and Know Your Business (KYB) frameworks.

From customer onboarding and identity verification to every subsequent financial transaction, the system provides comprehensive lifecycle monitoring. If the beneficial ownership of a corporate client changes, the system can automatically initiate Enhanced Due Diligence (EDD) procedures, ensuring compliance with the most stringent regulatory standards at every stage.

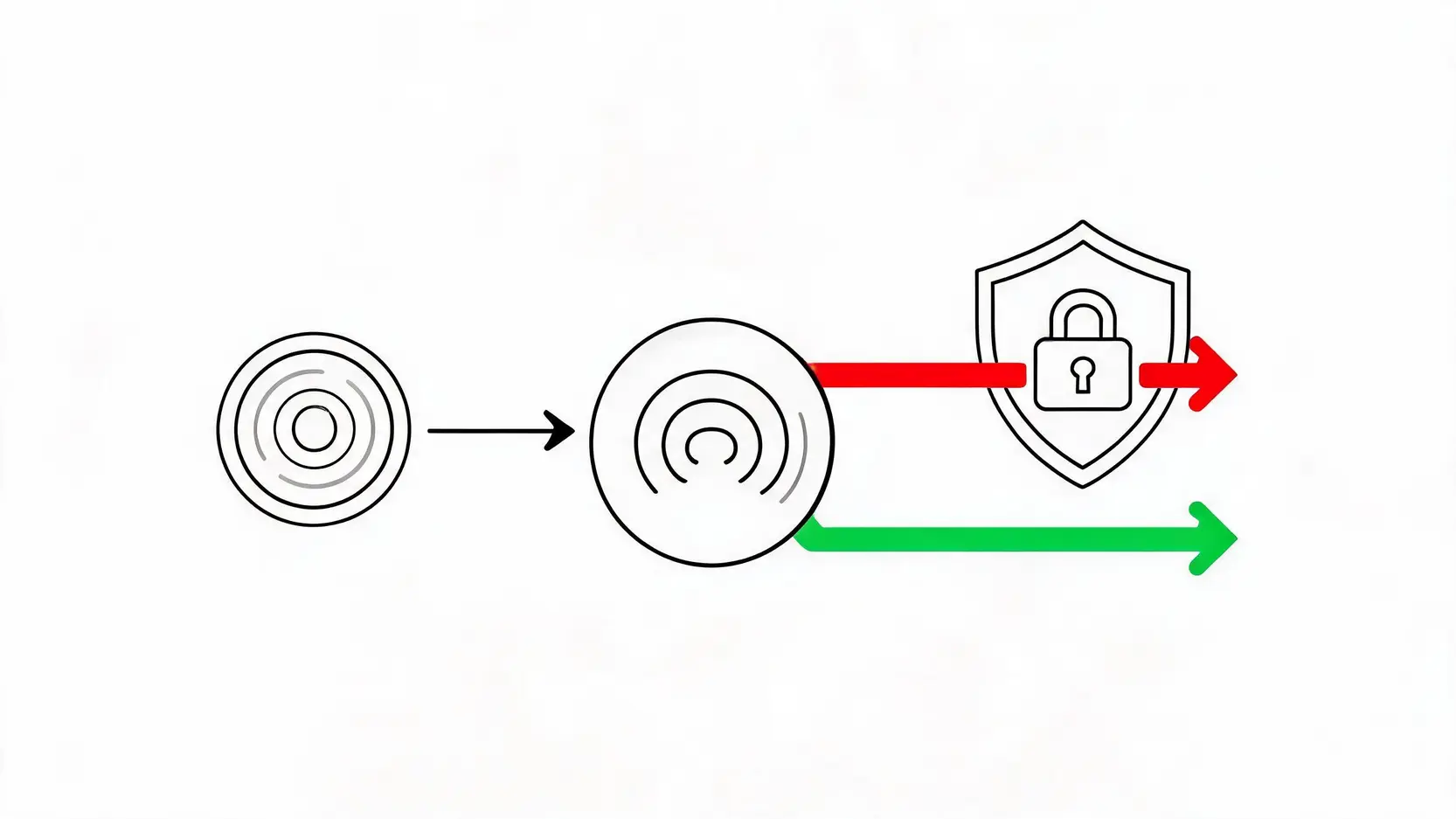

Automated STR Generation to Meet Global Regulatory Reporting Requirements

When compliance personnel determine that a transaction presents a high likelihood of money laundering activity, they are legally required to submit a Suspicious Transaction Report (STR) to the relevant financial intelligence unit.

Traditional reporting procedures are often cumbersome and vulnerable to human error. Modern AML big data monitoring systems incorporate automated STR generation capabilities. The system automatically compiles suspicious transaction data, fund flow visualizations, and customer background information into reports that conform to the required formats of regulatory authorities worldwide. This significantly reduces administrative burdens for compliance teams while ensuring both timeliness and complete accuracy in regulatory reporting.

The Latest FATF AML Guidelines and Global Regulatory Trends in 2026

Any discussion of compliance requires close attention to the latest developments from the Financial Action Task Force (FATF). By 2026, global anti-money laundering standards have reached unprecedented levels of sophistication. FATF no longer focuses solely on whether institutions maintain well-written compliance policies; instead, it evaluates actual effectiveness based on a “risk-based approach”.

In its latest guidance, regulators have explicitly emphasized that financial institutions should actively adopt systems built on big data and artificial intelligence to address increasingly concealed illicit financial flows. You may refer to the FATF International Standards on Combating Money Laundering and Terrorist Financing, which introduce stricter automated monitoring requirements relating to virtual assets, cross-border payment networks, and beneficial ownership transparency. This means that institutions that have not yet completed their digital transformation face substantial compliance risks and the possibility of significant regulatory penalties.

Frequently Asked Questions About AML Big Data Monitoring

Q: How much time is required to implement an AML big data monitoring system?

A: This largely depends on the size of the institution and the complexity of its existing systems. For cloud-based SaaS solutions, which do not require extensive on-premises server infrastructure, system integration, historical data cleansing, and model optimization can typically be completed within three to six months. For large multinational banks undertaking a comprehensive overhaul of their underlying architecture, the transition period may take one to two years.

Q: Does big data monitoring infringe upon customer privacy rights?

A: This is a widely discussed issue. In reality, compliance and privacy are not mutually exclusive. Properly designed AML systems strictly adhere to international data protection regulations such as the GDPR. During big data processing, sensitive personal information is anonymized and encrypted. Algorithms focus solely on identifying “abnormal transaction patterns” rather than examining personal lives. Compliance personnel may only access and decrypt specific information when the system generates an alert and there is a legitimate investigative basis for doing so.

Q: How can organizations with limited resources choose a cost-effective AML compliance solution?

A: For small and medium-sized enterprises or startup FinTech companies with limited resources, “cloud-based subscription” compliance technology services should be prioritized. These solutions are typically priced based on transaction volume or API usage, resulting in very low initial implementation costs while allowing flexible expansion as the business grows. When evaluating providers, particular attention should be paid to system stability, local language support, and whether the AI models possess continuous self-learning and updating capabilities.

Q: Can AI completely replace human review of suspicious transactions?

A: At the current stage and for the foreseeable future, AI serves as a “super assistant” rather than a “complete replacement”. AI and big data technologies excel at rapidly and accurately identifying high-risk abnormal transactions from massive datasets, significantly reducing false positive rates. However, the final determination of whether a transaction constitutes actual money laundering activity still requires the judgment and decision-making of experienced compliance professionals. Human-machine collaboration remains the golden standard of modern anti-money laundering practices.

Conclusion: Building a Compliance Defense Through AML Big Data Monitoring

Looking back, traditional static rule-based systems can no longer adequately protect organizations operating in today’s increasingly complex financial environment. Faced with constantly evolving financial crime techniques, AML big data monitoring is not merely a tool for satisfying routine examinations by monetary authorities and regulators. It has become a powerful shield for protecting corporate reputation and preventing exploitation by illicit actors.

By implementing advanced compliance technologies and leveraging cutting-edge AI applications such as machine learning and graph analytics, financial institutions and virtual asset service providers can significantly improve risk detection accuracy while reducing substantial compliance operating costs. This represents far more than a simple information technology upgrade. It is a critical component of the financial industry’s broader digital transformation strategy. In the increasingly stringent regulatory environment of 2026, only organizations that proactively embrace big data and AI technologies and establish intelligent, dynamic anti-money laundering frameworks will be able to navigate the complexities of global markets with confidence and maintain a lasting competitive advantage.