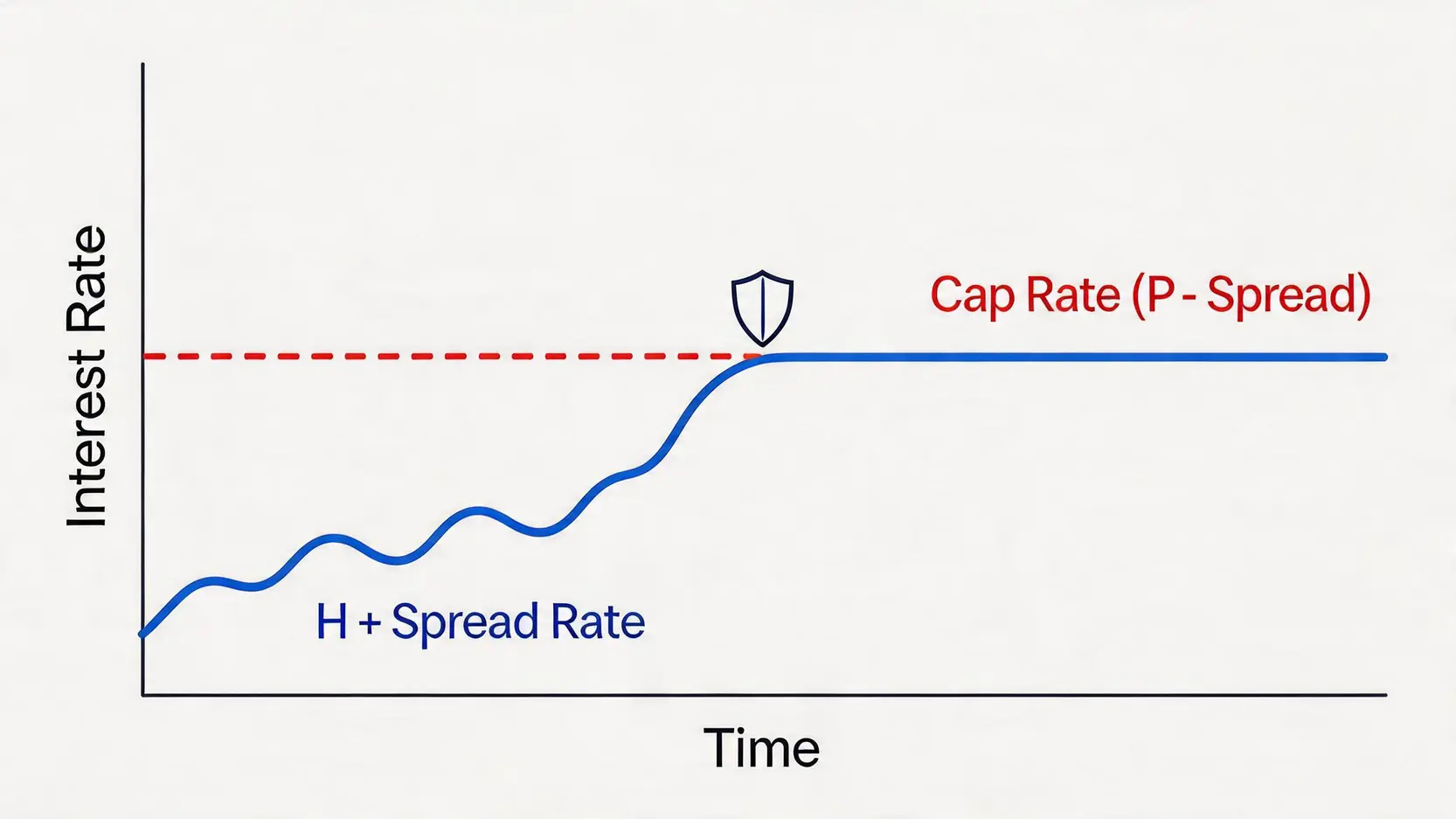

How the H-Plan “capped interest rate” mechanism provides a safety net for your mortgage repayments.

H-Plan vs. P-Plan: Which Should You Choose in a Rising Interest Rate Cycle?

The H-Plan and P-Plan each have their pros and cons. The choice depends on your expectations of interest rate trends and your risk tolerance. We can compare them in a simple table:

| Characteristics |

H-Plan (HIBOR-based mortgage) |

P-Plan (Prime-based mortgage) |

| Interest rate basis |

HIBOR + fixed spread |

Prime Rate (P) − fixed spread |

| Volatility |

High, closely follows the market with daily fluctuations |

Low volatility, as changes in P are relatively lagging and stable |

| Advantages |

Can benefit from lower interest rates in a declining rate cycle or low interest environment |

Interest rate movements are more predictable, resulting in stable repayments |

| Disadvantages |

In a rising interest rate cycle, rates increase quickly, leading to higher repayment pressure (but protected by a cap rate) |

Usually unable to benefit from ultra-low market interest rates |

| Suitable users |

Suitable for homeowners who can tolerate interest rate volatility and are seeking lower potential interest costs |

Suitable for homeowners who prefer stability and do not want frequent changes in repayment amounts |

In the current rising interest rate environment, although H-Plan mortgages have already reached their capped interest rates, the cap is usually similar to or slightly lower than P-Plan mortgage rates. Combined with expectations that interest rates may decline in the future, more than 90% of homeowners still choose the H-Plan mortgage scheme.

Frequently Asked Questions (FAQ)

Q: Which HIBOR tenor is usually used, one-month or three-month?

A: Currently, the vast majority of H-Plan mortgages in Hong Kong use the “one-month HIBOR” as the benchmark. This is because the one-month rate best reflects changes in market funding costs in a timely manner and has the highest transparency. Although other tenors of HIBOR exist in the market, for mortgages, you only need to focus on movements in the one-month HIBOR.

Q: What happens to my H-Plan mortgage payments if HIBOR remains high?

A: There is no need to worry. As mentioned earlier, H-Plan mortgages include a “capped interest rate” mechanism. Once HIBOR plus the bank’s spread exceeds the capped level, your mortgage interest will be locked at the cap and will not rise further indefinitely. In the current high-interest environment, the vast majority of H-Plan borrowers are effectively paying their capped rate.

Q: Where can I check the latest daily HIBOR rates?

A: The Hong Kong Association of Banks (HKAB) is the official institution that publishes HIBOR data. You can visit the official website of the Hong Kong Association of Banks after 11:30 a.m. on each business day to view the latest HIBOR rates across all tenors. Many major financial news websites and banking apps also update this data simultaneously.

Q: What is the difference between HIBOR and HONIA? Will HONIA replace HIBOR in the future?

A: HONIA (Hong Kong Dollar Overnight Index Average) is a risk-free benchmark rate based on actual transactions, while HIBOR is based on quoted rates. As the global trend moves toward risk-free rates, HONIA may become more widely used in the long term and could even replace HIBOR in certain financial products. However, in the foreseeable future, especially in the residential mortgage market, HIBOR remains the dominant benchmark.

Conclusion

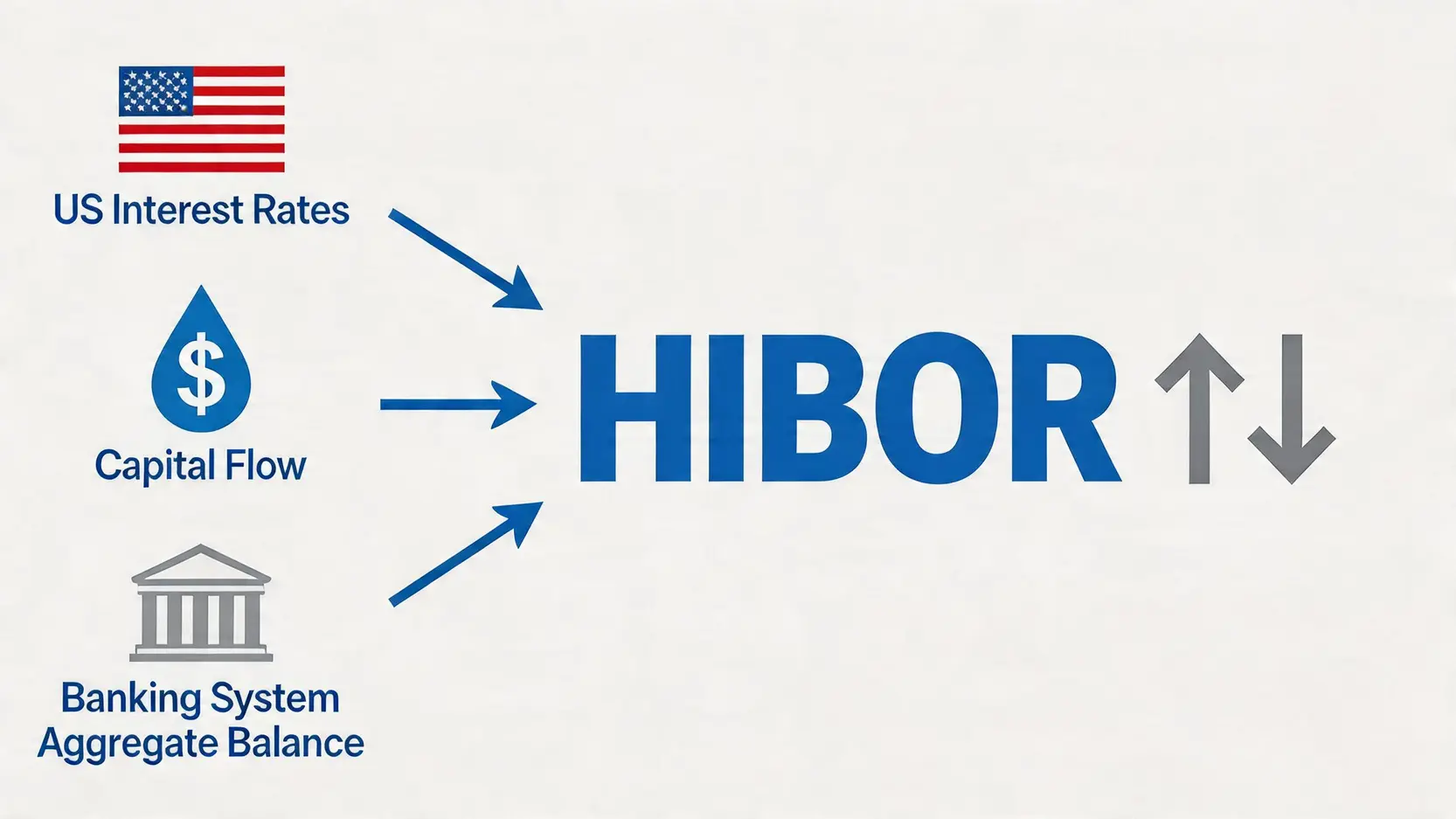

In summary, the Hong Kong Interbank Offered Rate (HIBOR) is not just a financial term, but a core factor that directly affects your monthly mortgage repayments. By understanding its definition, recognizing the three key drivers of HIBOR trends (US interest rates, capital flows, and banking system balances), and making good use of the capped interest rate mechanism in H-Plan mortgages, homeowners can better plan their personal finances and make more informed decisions in a changing market. Staying informed about market developments is the key to managing mortgage costs and navigating interest rate cycles smoothly.