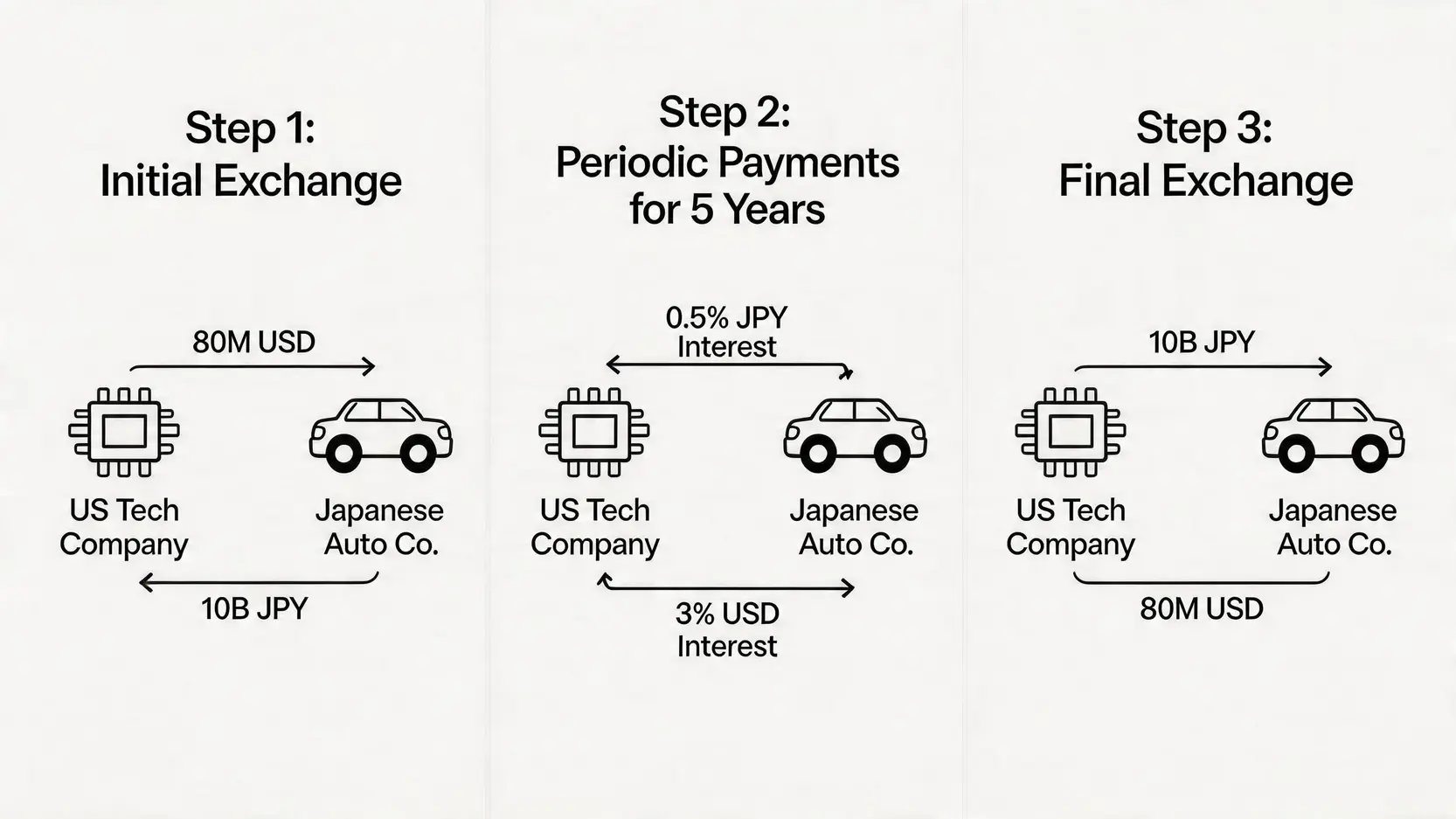

Cross-Currency Swap Process: Reducing Financing Costs Through Comparative Advantage

Result: Company B successfully obtains JPY funding at 0.5%, significantly lower than the 1.5% it would pay by borrowing directly in Japan; Company C obtains USD funding at 3%, also significantly lower than the 5% cost of borrowing directly in the US. Both parties leverage their home market financing advantages to reduce funding costs, perfectly demonstrating the powerful function of cross-currency swaps.

Must-Read! 4 Major Swap Trading Risks and Management Strategies

Although swap transactions are powerful, they are not without risks. Before enjoying their benefits, it is essential to fully understand the potential risks of swap trading and establish corresponding management strategies. The following are the four main types of risk.

Counterparty Risk: What if the Counterparty Defaults?

This is one of the most critical risks. Since swap contracts are privately negotiated between two parties (over-the-counter), if one party is unable to fulfill its contractual obligations due to financial difficulties or other reasons (for example, failing to pay interest or return principal), the other party will incur losses. The longer the contract tenor, the greater this risk.

- Management strategies:

- Transact with reputable large financial institutions.

- Sign an ISDA Master Agreement to clearly define default handling terms.

- Require the counterparty to provide collateral or margin.

- Clear transactions through a central counterparty (CCP) to reduce bilateral credit risk.

Interest Rate and Exchange Rate Risk (Market Risk): The Direct Impact of Market Fluctuations

Market risk refers to situations where movements in interest rates or exchange rates go against expectations, causing the value of the swap contract to move unfavorably. For example, in a cross-currency swap, if you are the party paying a fixed rate and receiving a floating rate, a sharp decline in market interest rates will reduce the interest you receive while the interest you pay remains unchanged, resulting in a loss.

- Management strategies:

- Conduct thorough market analysis and stress testing before entering into contracts.

- Treat swap transactions as hedging tools rather than speculative instruments, ensuring alignment with actual business risks.

- Consider incorporating option structures into swap contracts to increase flexibility.

Liquidity Risk: Difficulty in Exiting the Contract

Swap contracts are usually customized for specific needs and are not highly standardized. This means that if you want to terminate or transfer the contract before maturity, it may be difficult to find a willing third party in the market, or it may require paying a high termination cost.

- Management strategies:

- Use more standardized contract structures whenever possible.

- Clearly define early termination terms and calculation methods with the counterparty before signing.

- Ensure sufficient internal cash flow so that positions do not need to be closed under unfavorable market conditions.

Basis Risk

Basis risk exists in floating-for-floating cross-currency swaps. It refers to the risk that two different floating rate benchmarks (for example, SOFR for USD and ESTR for EUR) do not move in perfect alignment, leading to deviations in hedging effectiveness. Even though both are floating rates, differences in reference benchmarks may result in slight discrepancies in movement pace and magnitude, which can accumulate into significant losses over time.

- Management strategies:

- When designing hedging strategies, choose swap rate benchmarks that are as closely aligned as possible with the interest rate benchmarks of the hedged assets or liabilities.

- Regularly monitor basis movements, assess hedging effectiveness, and make adjustments when necessary.

Frequently Asked Questions (FAQ)

Q: Is principal exchange always required in swap transactions?

A: Not necessarily. In an FX swap, principal is exchanged at both the beginning and the end. Standard cross-currency swaps also involve principal exchange. However, there are also “interest-only currency swaps” where principal is not exchanged and only interest payments based on a notional principal are exchanged. This can be useful in certain hedging scenarios. In addition, the most common interest rate swaps typically do not involve principal exchange.

Q: Can individual investors participate in FX swap transactions?

A: Generally, it is very difficult. Both FX swaps and currency swaps are over-the-counter (OTC) products with large contract sizes, and the counterparties are mainly banks, large multinational corporations, and institutional investors. Individual investors are more likely to encounter “rollover” or “swap” in margin forex trading, where the calculation is related to swap points, but this is not an actual swap contract.

Q: How are swap points calculated?

A: Swap points represent the difference between the forward exchange rate and the spot exchange rate in an FX swap, mainly reflecting the interest rate differential between the two currencies over the contract period. A simplified formula is: swap points ≈ spot exchange rate × (quote currency interest rate – base currency interest rate) × (days/360). If one currency has a higher interest rate than the other, its forward rate is typically at a discount (lower rate), and vice versa at a premium (higher rate), to offset the interest advantage of holding the higher-yielding currency.

Q: What is the difference between a cross-currency swap and an interest rate swap?

A: The main difference lies in the currencies involved. An interest rate swap involves only a “single currency”, where both parties exchange interest cash flows of the same currency but with different rate structures (such as fixed vs floating). A cross-currency swap involves “two different currencies”, where both principal and interest cash flows are exchanged in different currencies. Therefore, cross-currency swaps are exposed to both interest rate risk and exchange rate risk.

Conclusion

In summary, FX swaps and currency swaps (also known as cross-currency swaps) are key tools for managing exchange rate and interest rate risks, but they serve fundamentally different purposes. An FX swap is a short-term liquidity management tool, while a currency swap is a long-term strategic financial arrangement. Clearly understanding the differences between FX swaps and currency swaps allows you to choose the most suitable financial instrument based on your company’s cash flow needs, hedging horizon, and risk tolerance. Although swap trading risks do exist, through prudent counterparty assessment, well-structured contract design, and continuous market monitoring, their powerful functions in stabilizing corporate finances and optimizing financing structures can be effectively realized.