In the context of globalized investment and trade allocation, exchange rate fluctuations of emerging market currencies (such as RMB and New Taiwan Dollar) present both a major challenge and an opportunity. Are you considering how to effectively hedge positions held in non-internationally commonly used currencies, or to identify trading opportunities from them? The financial derivative designed specifically to address such needs, “NDF Non-Deliverable Forward (Non-Deliverable Forward)”, is the key solution. This article will guide you through a clear and in-depth analysis of the NDF trading operational model, the unique NDF pricing mechanism, and focus on the world’s most active offshore RMB NDF market, helping you fully master this advanced tool for exchange rate risk management and investment.

What is NDF Non-Deliverable Forward?

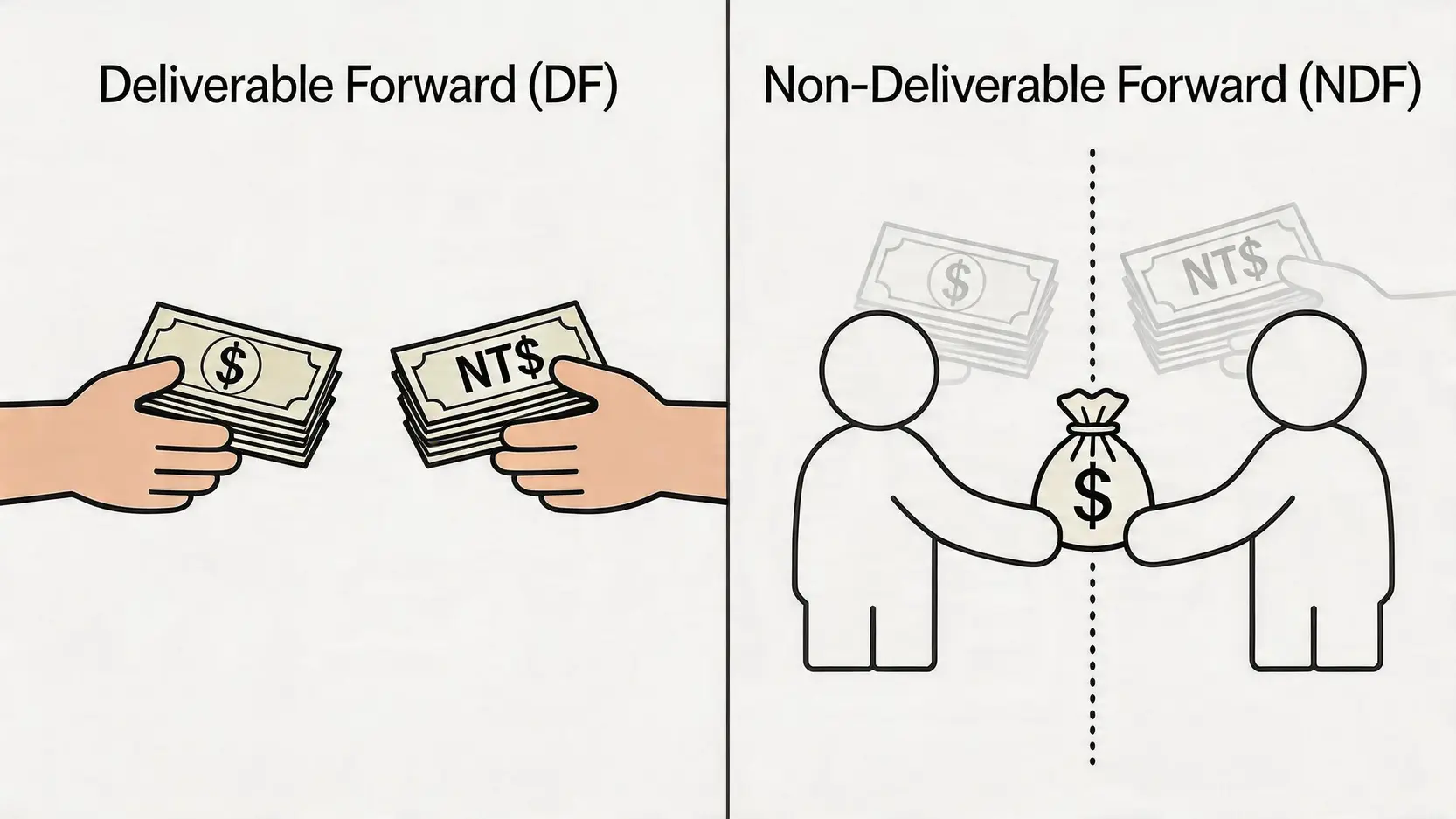

NDF, short for “Non-Deliverable Forward foreign exchange contract”, is a financial derivative designed for hedging or speculation in countries with capital controls or restricted currency convertibility. It allows two parties to settle the difference between the “agreed exchange rate” and the “spot exchange rate at maturity” in a specified future date, using a designated major currency (usually USD), without physically exchanging the notional principal of the contract.

The Core Definition of NDF: Why Is There No Principal Delivery?

“Non-deliverable” is the most core feature of NDF. A traditional Deliverable Forward (DF) contract requires both parties to physically exchange the principal amounts of the two currencies at maturity according to the agreed exchange rate. For example, in a USD to TWD DF contract, one party must deliver USD while the other delivers TWD at maturity.

However, in many emerging markets, their currencies are not internationally widely used and are subject to strict capital controls, making it difficult for foreign investors to freely transfer large amounts of local currency out of the country. NDF was created precisely to solve this issue:

Avoid regulatory restrictions: Since the entire transaction does not involve actual principal exchange and only settles the exchange rate difference, it effectively bypasses capital control restrictions in the target country.

Simplified process: Trading parties do not need to open bank accounts in the target country to hold local currency, significantly simplifying transaction procedures and costs.

Cash settlement: All profits and losses are settled in a one-time cash payment at contract maturity, usually in the most liquid international currency such as USD, making it efficient and convenient.

In simple terms, NDF is like a “bet” on future exchange rates. The stake is the difference between the agreed exchange rate and the market exchange rate at maturity. The winner receives the difference, and the loser pays it. The entire process is clean and straightforward, without involving actual currency exchange.

Main Differences Compared with Traditional Forward FX (DF)

To understand NDF more clearly, the following table compares its key differences with traditional forward foreign exchange (DF):

Comparison Item

NDF (Non-Deliverable Forward)

DF (Deliverable Forward)

Settlement Method

Only settles the exchange rate difference via cash settlement (Cash Settlement)

Requires physical exchange of principal in two currencies under the contract (Physical Delivery)

Applicable Currency

Currencies subject to capital controls and not freely convertible (e.g. CNY, TWD, KRW, INR)

Internationally widely circulated major currencies (e.g. EUR, JPY, GBP, AUD)

Trading Market

Mainly in offshore financial centers (e.g. Hong Kong, Singapore, London)

Both onshore and offshore markets

Main Purpose

Exchange rate hedging, speculation, and bypassing capital controls

Actual trade or funding needs, exchange rate hedging

Regulatory Complexity

Relatively lower, as it does not involve actual cross-border currency movement

Strictly regulated by the financial regulations of both parties’ jurisdictions

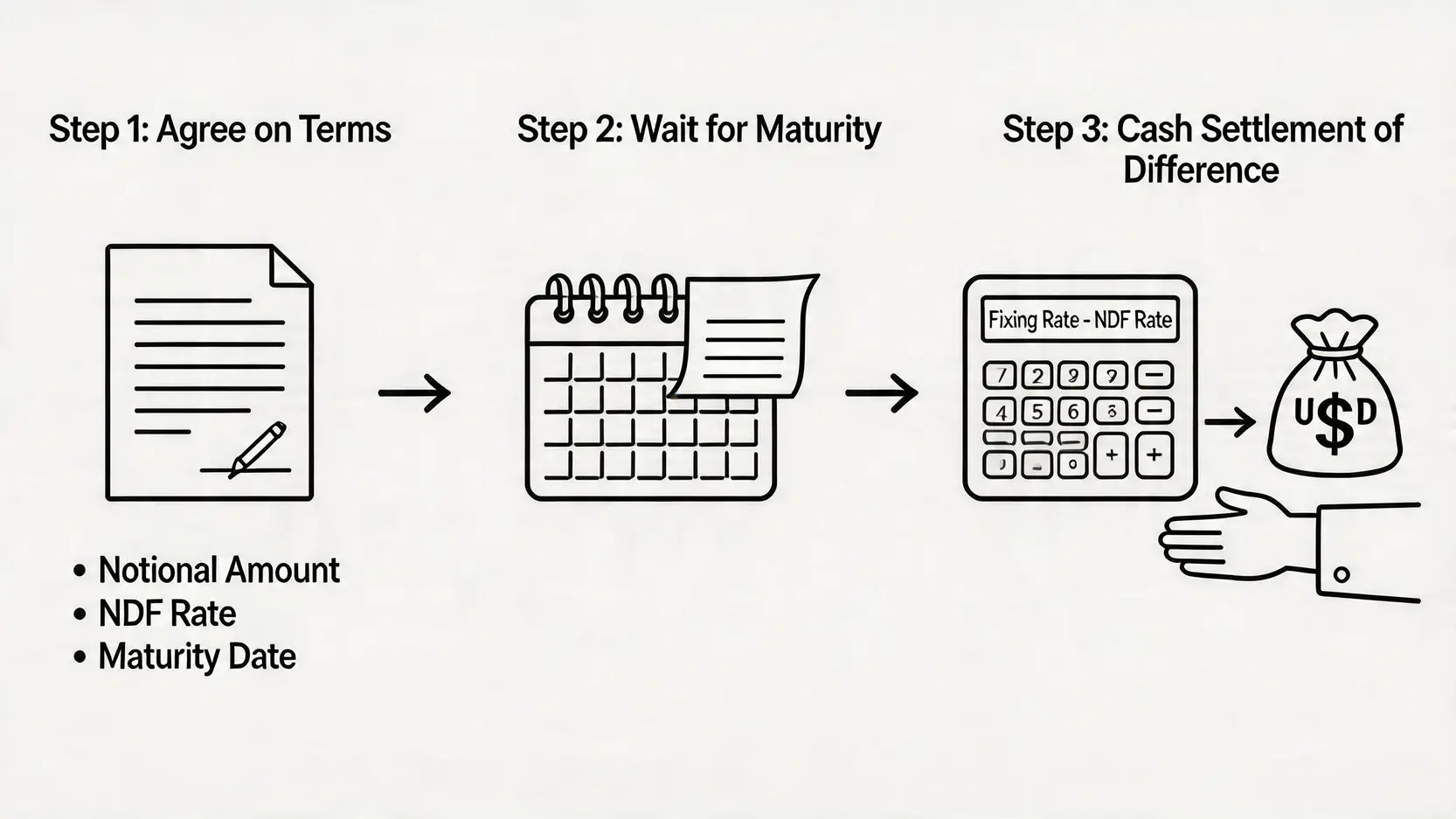

How Does NDF Trading Work? A Breakdown of a Complete Transaction Process

Figure 2: A Complete NDF Transaction Process

Understanding the operating mechanism of NDF is key to mastering its applications. A complete NDF transaction mainly consists of two stages: contract initiation and maturity settlement. Let us break down the entire process with a practical example.

Step 1: Entering into an NDF Contract (Agreed Exchange Rate, Notional Principal, Maturity Date)

Assume a Taiwanese exporter expects to receive a USD 1,000,000 payment in three months. The company is concerned that the New Taiwan Dollar may appreciate (e.g. from 32.00 to 31.50), which would reduce the converted value in NTD. To lock in profit, the company decides to enter into a three-month USD/NTD NDF contract with a bank.

Transaction Direction: The company sells USD and buys NTD.

Notional Amount: USD 1,000,000.

Agreed Rate (NDF Rate): Assume the bank quotes a three-month forward rate of 32.20.

Trade Date: The day the contract is signed.

Fixing Date: Usually two business days before maturity, where both parties reference a publicly recognized and authoritative exchange rate source (e.g. a specific Reuters page) as the final settlement rate.

Settlement Date: The final settlement date of the contract.

At this stage, the contract is established, and both parties wait for the fixing date three months later.

Step 2: Settlement Mechanism at Maturity (Fixing Rate vs. Agreed Rate)

Three months later, on the fixing date, assume the USD/NTD spot exchange rate (Fixing Rate) is 31.80.

The result is negative, meaning the bank must pay USD 12,578.62 to the exporter. This payment offsets part of the loss caused by the appreciation of the New Taiwan Dollar during the actual conversion, achieving the hedging effect.

Conversely, if the New Taiwan Dollar depreciates to 32.50 at maturity, the exporter would need to pay the difference to the bank. However, the USD 1,000,000 receivable would convert into more NTD, and the loss from the NDF would be offset by gains in the actual exchange.

NDF Pricing Mechanism Explained: How Forward Points Affect Pricing

You may wonder how the “agreed rate” in an NDF contract is determined. It is not arbitrarily quoted but derived from the spot exchange rate plus or minus “forward points”.

Forward points primarily reflect the “interest rate differential” between two currencies over the contract period. This is based on the Interest Rate Parity theory.

High-interest-rate currency: If a currency has a higher interest rate, its forward rate typically trades at a discount, meaning the forward rate is lower than the spot rate.

Low-interest-rate currency: Conversely, a lower interest rate currency typically trades at a premium, meaning the forward rate is higher than the spot rate.

For example, if the US interest rate is 5% while the New Taiwan Dollar interest rate is 2%, holding NTD yields lower interest returns. The market would expect NTD to appreciate in the future to offset this difference. As a result, the USD/NTD forward rate (how much NTD one USD can buy in the future) will be higher than the spot rate, reflecting a premium. Banks incorporate this by adding the corresponding forward points to the spot rate when quoting.

This pricing mechanism ensures that NDF prices reflect market expectations of future interest rates and exchange rates, making it an effective indicator of market sentiment.

Offshore RMB (CNH) NDF Market Deep Dive

Among global NDF markets, the most active is the offshore RMB (CNH) NDF market. This is closely tied to China’s unique currency policy.

Why Does Offshore RMB Require an NDF Market?

Figure 3: The Key Role of NDF in the Offshore RMB (CNH) Market

The RMB circulating within mainland China is referred to as “onshore RMB (CNY)”, and its exchange rate is strictly managed by the People’s Bank of China (central bank), with limited daily fluctuation. However, RMB circulating outside China (mainly in Hong Kong) is referred to as “offshore RMB (CNH)”, and its exchange rate is primarily determined by market supply and demand, making it more flexible.

Because CNY is not freely convertible and is subject to capital controls, it is very difficult for international investors and companies to hedge their RMB-denominated assets or liabilities. The CNH NDF market emerged to provide a perfect solution:

Hedging channel: It provides an effective tool for international companies holding RMB assets or with future RMB payment obligations to hedge exchange rate risk.

Investment tool: It allows global investors to speculate on the future direction of RMB without actually holding RMB.

Price discovery: CNH NDF pricing is not interfered with by the People’s Bank of China and purely reflects the international market’s true expectations of future RMB exchange rates.

How Does CNH NDF Reflect Market Expectations of RMB?

CNH NDF pricing is an important window for observing international market expectations of RMB appreciation or depreciation. Its pricing often leads the trend of onshore RMB (CNY).

When depreciation is expected: When international investors are broadly bearish on the Chinese economy or expect RMB to depreciate, they will heavily buy USD/CNH NDF contracts (i.e. long USD, short offshore RMB). This pushes NDF prices higher, significantly above spot CNH levels, reflecting strong depreciation expectations.

When appreciation is expected: Conversely, when the market is bullish on RMB, investors sell USD/CNH NDF contracts, suppressing NDF prices and reflecting appreciation expectations.

Therefore, tracking CNH NDF pricing and trading volume helps analysts and traders gauge shifts in offshore market sentiment toward RMB, making it an important reference in reports from major financial institutions.

Arbitrage Opportunities and Risks Between Onshore (CNY) and Offshore (CNH) NDF Markets

Because CNY and CNH are separated but interconnected markets, price discrepancies often arise, creating arbitrage opportunities. When CNH NDF implies significantly stronger depreciation expectations than CNY, arbitrageurs may attempt “long CNY, short CNH”, and vice versa.

However, such arbitrage is not without risks:

Policy risk: The People’s Bank of China may introduce new currency policies at any time to intervene in exchange rates, causing sudden narrowing or widening of the CNY-CNH spread, potentially leading to strategy failure or losses.

Liquidity risk: During periods of high market volatility, offshore liquidity may dry up rapidly, leading to sharply increased trading costs.

Execution risk: Cross-border and cross-market execution inherently involves delays and operational risks.

Therefore, although theoretical arbitrage opportunities exist, actual execution requires high-level modeling and strong risk management capabilities.

Main Applications and Investment Strategies of NDF

As a flexible financial instrument, NDF is widely used in corporate hedging and financial speculation.

Corporate Use: Exchange Rate Hedging for Import and Export Trade

This is the most classic use case of NDF. For companies with frequent trade in emerging markets, exchange rate volatility is a major source of uncertainty affecting profit.

Example scenario: A Malaysian furniture importer orders goods worth 5,000,000 RMB from China, payable in six months. To avoid higher procurement costs due to potential RMB appreciation in six months, the importer can enter into a six-month USD/CNH NDF contract to lock in the future RMB exchange rate. This ensures that regardless of future exchange rate movements, procurement costs are predetermined, facilitating financial planning.

Investor Use: Speculation and Arbitrage Based on Exchange Rate Expectations

For professional investors and hedge funds, NDF is an ideal tool for directly expressing directional views on emerging market currencies.

Directional speculation: If an investor expects the Indian Rupee (INR) to appreciate due to economic growth, they can sell a USD/INR NDF contract. If INR appreciates (USD/INR falls), the investor profits without needing to physically hold INR.

Carry trade: Combining interest rate differentials between currencies, NDF can be used in more complex carry trade strategies.

Three Key Risks Before Investing in NDF

Although NDF offers flexibility, it remains a professional derivative product with significant risks:

Counterparty risk: NDF is traded over the counter (OTC), not on standardized exchanges. If the counterparty (usually an investment bank) defaults or becomes insolvent, you may not receive expected profits. Choosing reputable and well-capitalized institutions is critical.

Basis risk: The fixing rate used for settlement may not fully match the actual exchange rate available at maturity when you convert funds, creating a small but sometimes amplified discrepancy under extreme conditions.

High leverage risk: NDF transactions often involve high leverage, allowing large notional exposure with relatively small margin. While this amplifies gains, it also significantly increases losses and may exceed initial margin.

Frequently Asked Questions About NDF (Non-Deliverable Forward)

Q: Is NDF trading legal? How can it be accessed in Hong Kong?

A: NDF trading is a fully legal financial derivative transaction in major international financial centers (such as Hong Kong, Singapore, and London). In Hong Kong, investors can participate in NDF trading through major investment banks or securities firms licensed for derivatives trading. However, such transactions usually have a relatively high capital threshold and are mainly aimed at institutional investors and high-net-worth professional investors.

Q: What is the typical margin requirement for NDF?

A: There is no fixed standard for NDF margin requirements. It depends on several factors, including the counterparty (bank) policy, contract tenor, notional amount, and volatility of the underlying currency. Generally, the higher the currency volatility and the longer the contract duration, the higher the margin requirement, which may range from 2% to 10% of the notional amount.

Q: Besides RMB, which other currencies have active NDF markets?

A: In addition to the most active offshore RMB (CNH) market, many other currencies subject to capital controls or with lower liquidity also have mature NDF markets. Common examples include New Taiwan Dollar (TWD), Korean Won (KRW), Indian Rupee (INR), Indonesian Rupiah (IDR), Malaysian Ringgit (MYR), Philippine Peso (PHP), and some Latin American currencies (such as Brazilian Real BRL).

Q: Can retail investors participate in NDF trading?

A: Direct participation in interbank NDF over-the-counter markets is highly difficult for retail investors. However, some forex brokers offer Contract for Difference (CFD) products that provide similar exposure, allowing retail investors to trade emerging market currency movements with leverage. It should be noted that CFD trading rules and risk characteristics differ from standard NDFs, and investors should fully understand the product before investing.

Conclusion

In summary, Non-Deliverable Forwards (NDF) provide a flexible and efficient tool, particularly for managing exchange rate risks in currencies with capital controls such as offshore RMB. It serves not only as a hedge for multinational corporations but also as a powerful instrument for professional investors to capture market expectations. By understanding its non-deliverable cash settlement nature, interest-rate-driven pricing mechanism, and the unique structure of offshore markets, both businesses and market participants can better utilize NDF for hedging or strategic trading. Given its complexity and inherent risks, seeking professional financial advice is a prudent step before implementing any FX strategy.

Complete Analysis of USD/CHF as a Safe Haven: In 2026, Which Is the True Safe-Haven King, the US Dollar or the Swiss Franc? When global markets are volatile, finding a safe haven for capital becomes investors’ top priority. As a classic safe-haven currency pair, USD/CHF often moves in ways that...

What Should You Do When Risk-Off Sentiment Rises? Understand Four Key Signals and Three Asset Allocation Strategies From Scratch Amid recent international turmoil and persistently high inflation data, unease has spread across the market, and the term “rising risk-off sentiment” has appeared frequently. What exactly does it mean? When markets...

How to Get Started with Bitcoin? The Complete 2026 Bitcoin Buying Guide for Beginners After watching Bitcoin repeatedly reach new highs in recent years and successfully pass spot ETF reviews in the US and Hong Kong in 2024, officially entering mainstream financial markets, many investors have turned their attention to...