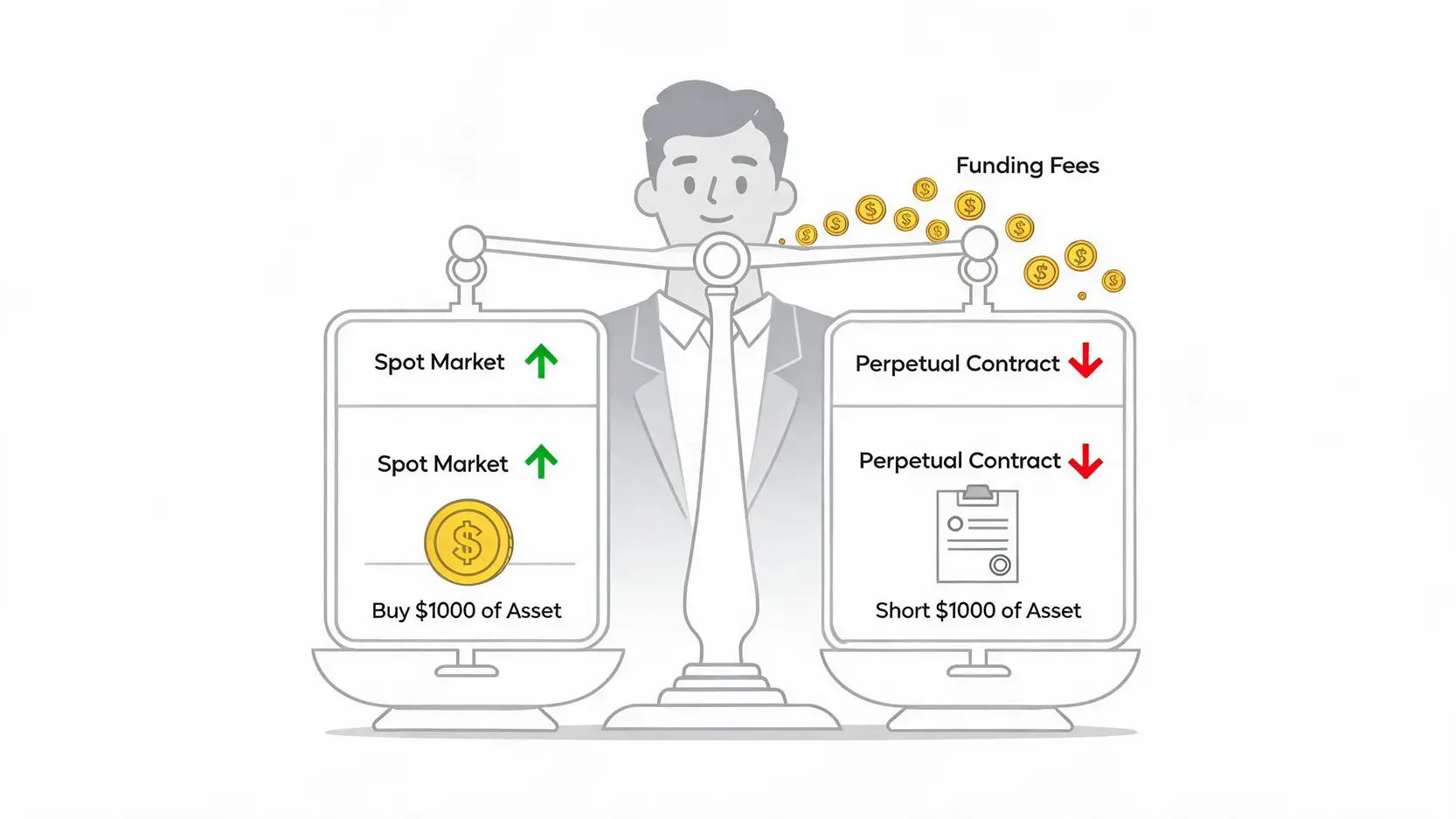

Execution:

- Buy spot: Purchase $1,000 worth of Bitcoin in the spot market.

- Short futures: Simultaneously open a $1,000 Bitcoin short position in the perpetual futures market.

Hedging effect:

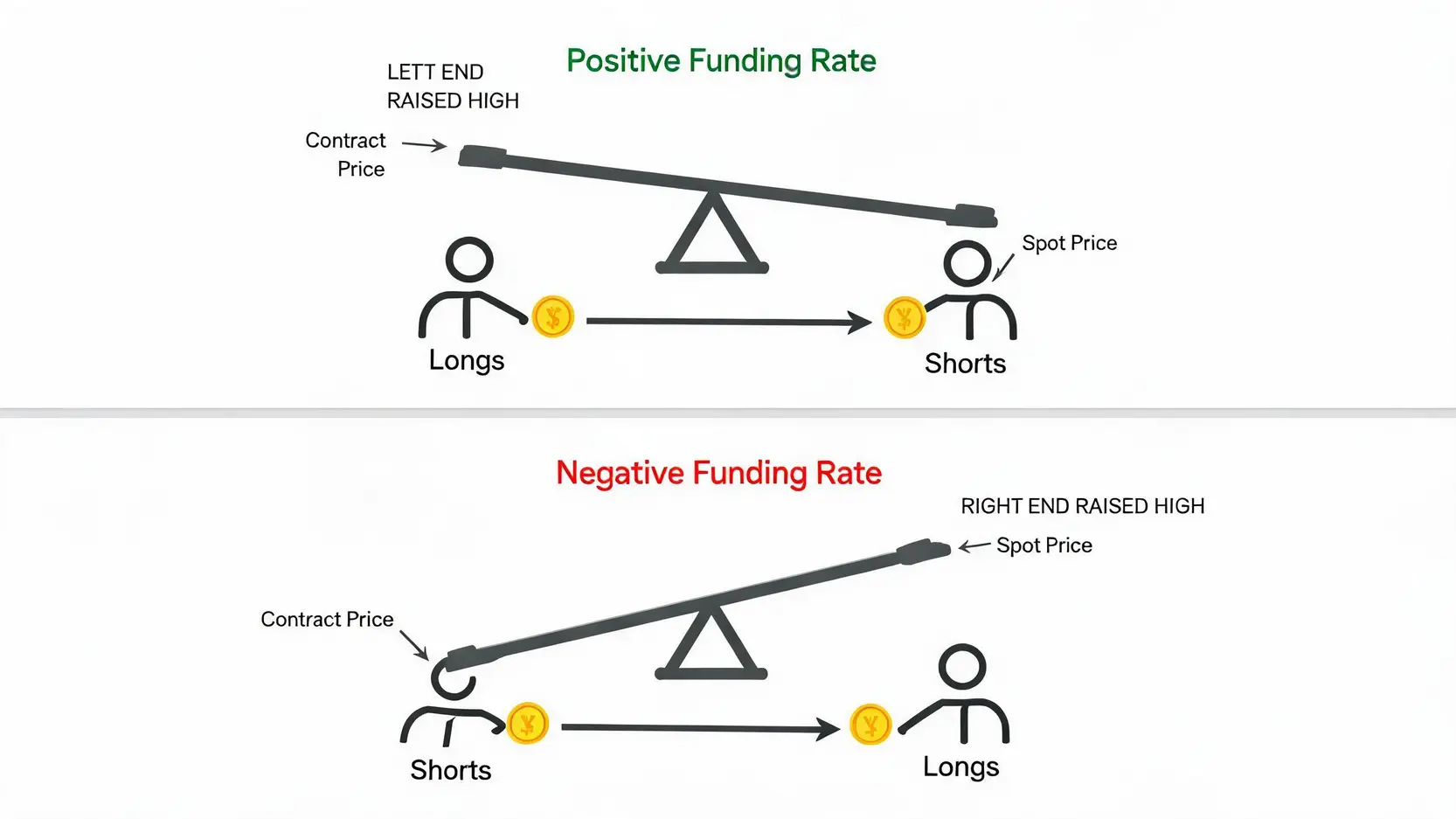

- If Bitcoin rises by 10%, your spot position gains $100, while your futures short loses $100, resulting in a net zero impact.

- If Bitcoin falls by 10%, your spot loses $100, while your futures short gains $100, again offsetting each other.

After this step, your total portfolio value is no longer affected by price fluctuations. Your only profit source becomes the periodic funding payments (usually settled every 8 hours).

Step 3: Accurately Calculate Expected Returns: How Much Profit Remains After Fees?

The key detail lies in costs. Funding rate income is not pure profit and must be calculated after deducting all trading fees.

Main costs include:

- Opening fees: Exchanges charge trading fees (taker or maker) when opening spot and futures positions.

- Closing fees: Fees are also charged when closing both positions.

- Slippage: In volatile markets, actual execution prices may differ from expected prices.

Example calculation:

Assume you use $10,000 for arbitrage with a funding rate of -0.05%, settled every 8 hours. Trading fees for both spot and futures are 0.1%.

- Single funding income: 10,000 × 0.05% = $5

- Daily funding income: $5 × 3 = $15

- Total opening cost: (10,000 × 0.1%) + (10,000 × 0.1%) = $20

- Break-even time: $20 / $15 ≈ 1.33 days

This means you must hold the position for more than 1.33 days before generating net profit. Always calculate carefully before entering a trade to ensure funding income covers all costs.

Step 4: Practical Execution and Risk Management (Slippage and Price Volatility)

In practice, it is recommended to use “limit orders” to reduce slippage. Since you are holding both spot and short futures positions, you must closely monitor “margin levels”. Even though the position is hedged, extreme price movements can still trigger liquidation due to insufficient margin. It is advisable to use low leverage (e.g. 1–3x) and be prepared to add margin when necessary.

Risks and Pitfall Guide for Negative Funding Rate Arbitrage: 3 Major Hidden Risks

Although it is considered a low-risk strategy, negative funding rate arbitrage is by no means “risk-free”. Understanding and avoiding the following three major risks is key to achieving long-term stable returns.

Risk 1: Liquidation Risk Caused by Extreme Price Volatility

This is the primary risk. Even if your position is perfectly hedged 1:1, when the market moves sharply against your futures position (i.e. prices rise), your short futures position will incur significant unrealized losses. If your margin is insufficient to maintain the position, it may be forcibly liquidated. Once the short position is liquidated, your spot holdings will be fully exposed to market risk, and the hedge will no longer be effective.

Avoidance guide:

- Use low leverage or no leverage: This is the most effective risk control method. The lower the leverage, the wider the price range your position can withstand.

- Maintain sufficient margin: Do not use all your capital as margin. Always keep extra funds as a buffer for extreme market conditions.

Risk 2: Profit Erosion from Trading Costs (Fees and Slippage)

As shown in earlier calculations, trading costs are the biggest enemy of arbitrage strategies. When funding rates are not high or holding periods are short, high fees and slippage can easily turn profits into losses.

Avoidance guide:

- Choose exchanges with lower fees: Compare fee structures carefully before opening an account.

- Focus on higher funding rate opportunities: Do not arbitrage for the sake of arbitrage. Target opportunities where expected APR significantly exceeds total trading costs.

- Use limit orders: Reduce additional slippage caused by market orders.

Risk 3: Exchange Stability and Liquidity Risks

All operations depend on the stability of the exchange. If the exchange experiences server downtime, API delays, or extreme market “wicks” (sudden price spikes or drops), your strategy may fail. In addition, if the trading pair has low liquidity, you may face significant slippage when entering or exiting positions.

Avoidance guide:

- Use top-tier exchanges: Prioritize globally ranked, reputable exchanges with strong liquidity and deep order books.

- Diversify funds: For larger capital, consider spreading positions across 2–3 high-quality exchanges to reduce single-platform systemic risk.

FAQ: Frequently Asked Questions About Negative Funding Rate Arbitrage

Q: How often is the funding rate settled?

A: Most cryptocurrency exchanges settle funding rates every 8 hours, specifically at 00:00, 08:00, and 16:00 UTC. However, some exchanges or specific contracts may have different settlement intervals (such as every 4 hours or even every 1 hour). It is essential to confirm the exact rules of the platform you are using before trading.

Q: Is negative funding rate arbitrage risk-free?

A: No. It is a “low-risk” strategy, not a “risk-free” one. As explained above, it still carries risks such as liquidation risk, cost risk, and platform risk. Without proper risk management, investors may still incur losses. The key is to understand the sources of risk and apply appropriate mitigation measures.

Q: Where can I check real-time Funding Rate data?

A: There are many reliable third-party data platforms that help monitor funding rates across the market. Common options include Coinglass, CoinGecko, and CryptoQuant. These platforms typically provide clear charts and sorting functions, allowing you to quickly identify potential arbitrage opportunities.

Q: How much capital is needed for negative funding rate arbitrage?

A: There is no strict minimum requirement in theory, but due to fixed trading fees, very small capital will result in significant profit erosion. Generally, it is recommended to start with at least 1,000 USDT to achieve meaningful returns after covering costs. The larger the capital, the lower the proportion of fixed costs, and the more efficient the strategy becomes.

Q: Is this strategy suitable for beginners?

A: For complete beginners with no experience in spot and futures trading, this strategy may be challenging to execute directly. It is recommended that beginners first understand spot trading, shorting mechanisms in futures, and margin concepts, and then practice with small amounts. For investors with some trading experience, this is a relatively accessible low-risk strategy.

Conclusion

In summary, negative funding rate arbitrage is a relatively stable cryptocurrency investment strategy that leverages the pricing mechanism of perpetual futures to earn returns from the sentiment gap between long and short positions while hedging market price risk. Through this perpetual futures funding rate guide, you should now understand the full process from how Funding Rate is calculated to practical execution. The key to success lies in patiently identifying opportunities, accurately calculating costs and returns, and always prioritizing risk management. You can now begin monitoring market data and looking for your first arbitrage opportunity.