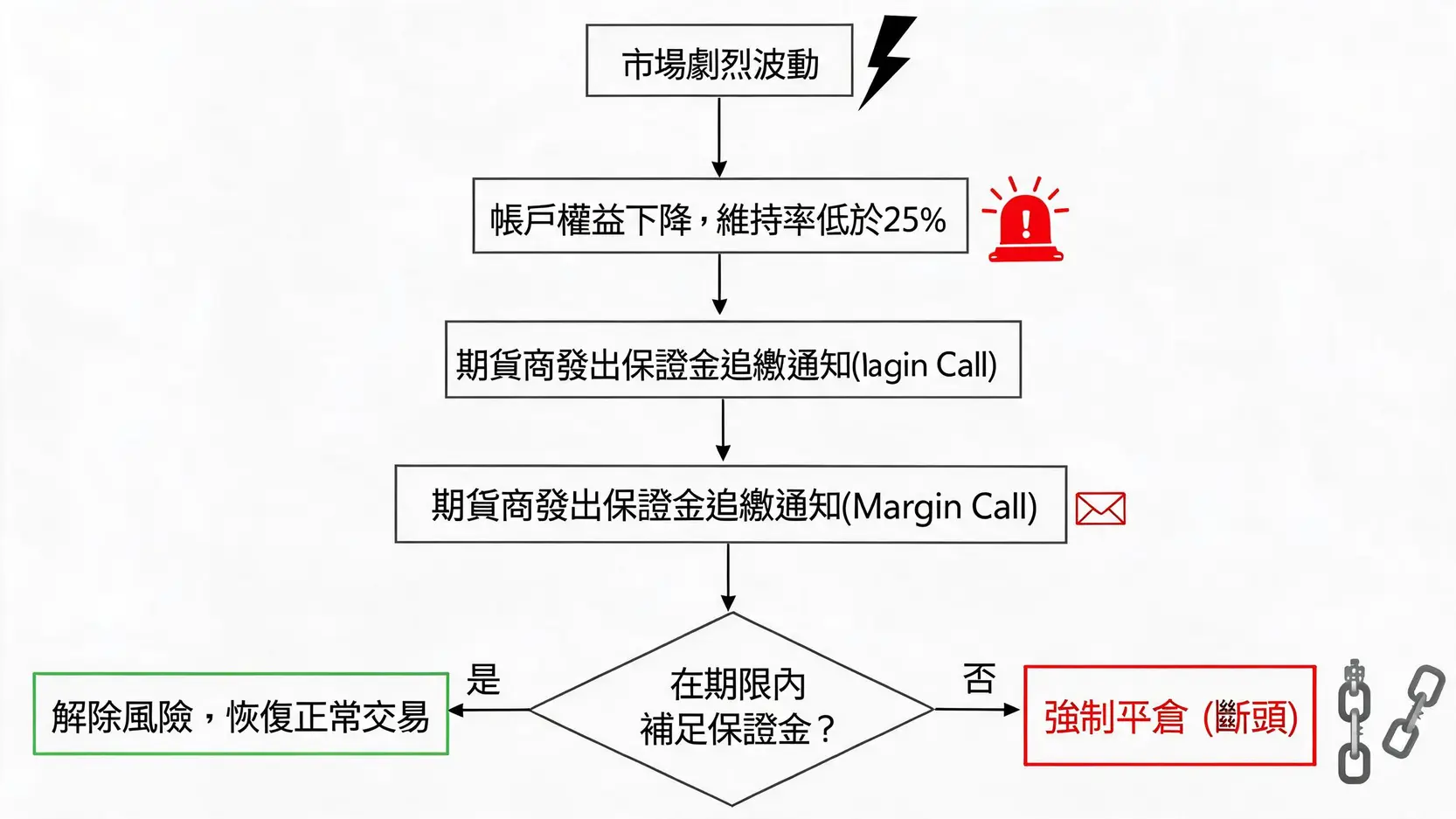

The Chain Reaction of Insufficient Margin: From Margin Calls to Forced Liquidation

What Is the Maintenance Ratio? The Danger Signal Below 25%

In your trading account, there is an extremely important indicator called the “Risk Indicator” or “Equity Maintenance Ratio”. Its calculation formula is:

Maintenance Ratio = (Total Account Equity / Total Required Margin for Open Positions) * 100%

This ratio represents the extent to which your account’s net value covers the required margin. According to Taiwan Futures Exchange regulations, when this figure falls below 25% after settlement, the futures broker must issue a “Margin Call” notice.

The Margin Call Process During Intraday Volatility

Receiving a margin call means you must replenish funds before 12:00 PM on the next business day to restore the account to the “initial margin” level, meaning the maintenance ratio must return above 100%. If you fail to replenish the funds in time, the futures broker has the right to proceed to the next step: forced liquidation.

It is worth noting that although official regulations only require a margin call when the post-settlement ratio falls below 25%, many futures brokers’ risk management departments closely monitor clients’ maintenance ratios during market hours. If intraday market conditions deteriorate severely and the maintenance ratio drops rapidly, an “intraday margin call” emergency situation may occur.

The Execution Mechanism and Consequences of Forced Liquidation

If you fail to replenish the margin within the required timeframe, the futures broker will execute “forced liquidation”, commonly known as being “wiped out”.

- Execution Method: The futures broker will directly force-sell (or buy back) your open contracts from your account at market price or the nearest available price until your maintenance ratio rises above 25%.

- Terrifying Consequences: You have absolutely no control over the liquidation price. During periods of poor liquidity or violent price swings, execution prices may be extremely unfavorable, causing your actual losses to far exceed expectations. Worse still, if losses after liquidation exceed your total account equity, a “negative balance” situation will occur, and you will still need to repay the deficit to the futures broker.

Black Swan Stress Test: If the Market Crashes 3,000 Points, Is Your Margin Enough?

No amount of theory is more impactful than a real market shock. A mature seller trader must conduct stress testing on positions and prepare for the worst-case scenario.

Simulated Scenario: Using the March 2020 Market Crash as an Example of Seller Margin Changes

Looking back at March 2020, global stock markets collapsed within a short period due to panic surrounding the COVID-19 pandemic. Taiwan stocks fell nearly 3,000 points from their peak within just a few weeks. Under such extreme market conditions:

- Implied Volatility Surged: Market panic spread rapidly, causing options implied volatility (IV) to spike from 20% to over 60%, leading to a sharp increase in premium prices and dramatically expanding unrealized losses on seller positions.

- Margin A Value Increased: In response to rising risks, the Taiwan Futures Exchange urgently raised the margin A Value. This meant that even if your position remained unchanged, the required margin automatically increased, further compressing your maintenance ratio.

Under this double impact, out-of-the-money seller positions that originally appeared safe could face margin calls or even forced liquidation within just a few days.

How to Calculate Your Maximum Risk Tolerance

Before establishing any seller position, ask yourself one question: “If the index suddenly surges or crashes 1,000 or 2,000 points against my position tomorrow, what will happen to my account?”

You can use your broker’s simulation tools or manually calculate:

- Estimated Losses: Calculate the theoretical losses on your options positions under extreme price scenarios.

- Estimated Margin Changes: Consider the possibility of rising volatility and increased A Values, then estimate the additional required margin.

- Review the Maintenance Ratio: Subtract the estimated losses from your account equity, then divide it by the increased total required margin to determine whether the maintenance ratio remains within a safe range.

Defensive Strategies: The Importance of Spread Orders and Dynamic Hedging

When facing unpredictable black swan events, the best defense is preparation in advance. Instead of simply selling naked positions, it is better to establish controllable-risk strategies from the start:

- Spread Orders: As mentioned earlier, constructing Call or Put spread orders is the most effective method for converting unlimited losses into limited losses.

- Dynamic Hedging: When the market begins showing unfavorable signals, you can hedge by buying futures or further out-of-the-money options to reduce the overall Delta risk of your portfolio.

Conclusion

In summary, understanding and respecting the margin risks of Taiwan Index options sellers is an essential step toward becoming a mature seller trader. This article not only breaks down the details of options margin calculation formulas, but also emphasizes the absolute importance of seller-side risk management during extreme market conditions through stress-testing scenarios. Options seller strategies are indeed powerful tools, but only after establishing comprehensive defensive mechanisms and capital management plans can you consistently collect premiums in the market, instead of being mercilessly carried out during the next black swan event.

FAQ

Q: What Is the Difference Between Margin Calculation for Selling Calls and Selling Puts?

A: The calculation formula is exactly the same, which is “Premium Market Value + Max(A Value – Out-of-the-Money Value, B Value)”. The only difference lies in how the “Out-of-the-Money Value” is calculated. For selling Calls, the out-of-the-money value is “Strike Price – Current Index Price”; for selling Puts, the out-of-the-money value is “Current Index Price – Strike Price”.

Q: If Margin Is Insufficient, Will the Futures Broker Immediately Force Liquidate My Position?

A: Not immediately. Under the standard process, when your account’s “post-settlement” maintenance ratio falls below 25%, the futures broker will issue a margin call notice on the same day. You must replenish the required funds “before 12:00 PM on the next business day”. If the funds are not replenished before the deadline, the futures broker will then begin executing forced liquidation. However, please note that during periods of extreme market volatility, some futures brokers may adopt stricter intraday risk control measures.

Q: Does a Spread Order Combination Always Require Less Margin?

A: Yes, in the vast majority of cases, spread orders (such as Bull Call Spreads or Bear Put Spreads) require significantly lower margin than selling a single naked options position. This is because the long position within the spread provides protection for the short position, locking in the maximum possible loss. As a result, the risk deposit (margin) charged by the futures broker is naturally much lower.

Q: How Can I Check the Latest Taiwan Futures Exchange Margin Requirements?

A: The best way to check the latest and most accurate margin A, B, and C Values is to visit the official Taiwan Futures Exchange website directly and navigate to the “Clearing Services” > “Margin Requirement Table” page. Any announcements from futures brokers should be verified against the official exchange information.