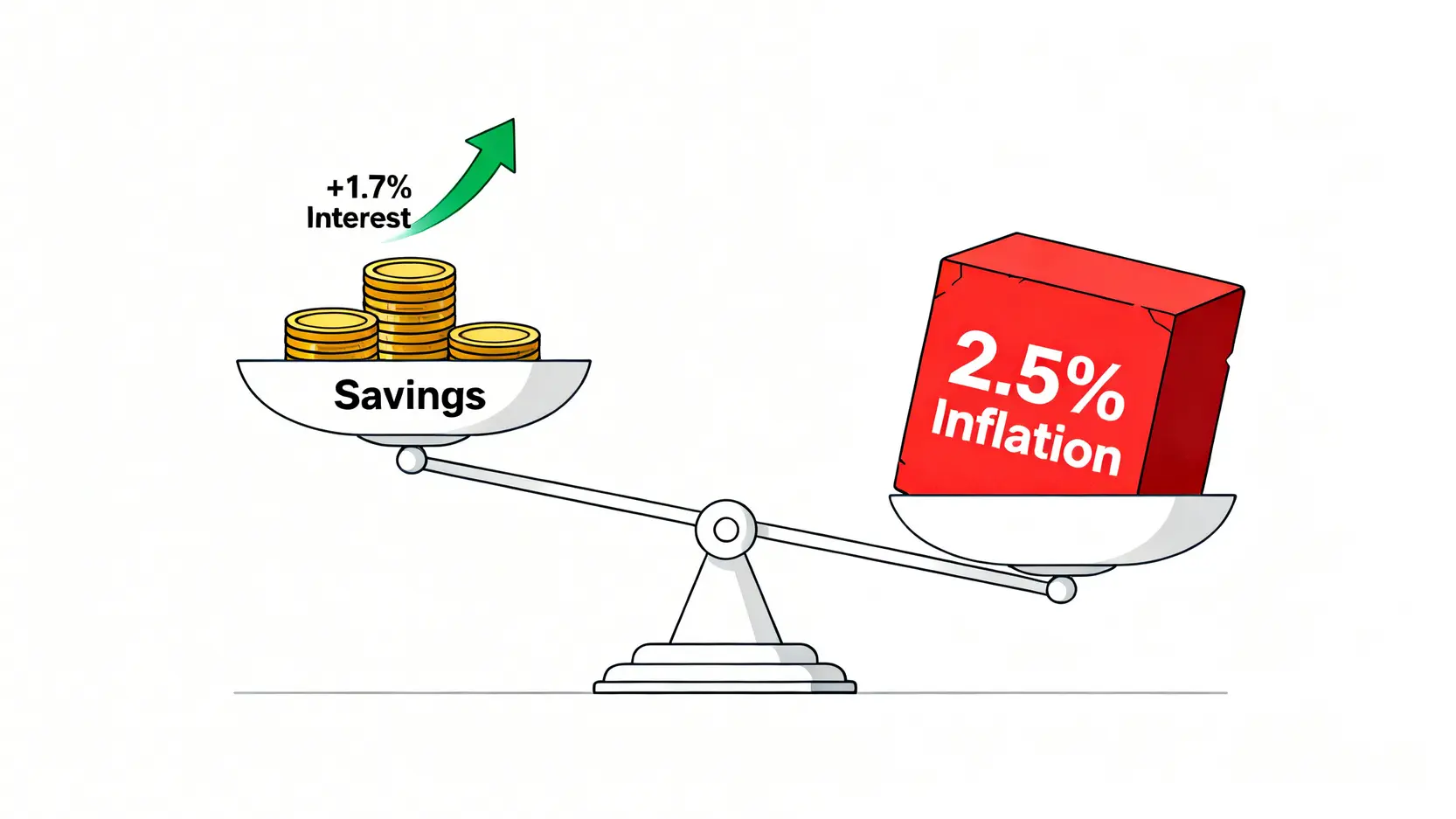

The hidden killer of time deposits: when the inflation rate (2.5%) exceeds the time deposit rate (1.7%), your money is effectively shrinking.

Risk 2: Interest Loss from Early Termination and Key Considerations

The essence of time deposits is exchanging “time” for “interest”. If you “terminate the deposit early” due to urgent cash needs, the bank will return your principal, but the interest will not be calculated based on the original time deposit rate. Typically, the bank will treat the deposit period as a savings account or apply a discounted rate (usually around 80%) to calculate the interest. This means you will lose most or even all of the expected interest. Therefore, before placing a time deposit, ensure that the funds will not be needed during the agreed period, or consider splitting a large sum into multiple smaller deposits to retain some liquidity.

Risk 3: Opportunity Cost from Locked-In Funds

This is a form of “opportunity cost”. When your funds are locked in a three-year time deposit, if the stock market rises significantly or other higher-yield, manageable-risk investment opportunities emerge during that period, your funds cannot participate. When making long-term deposit decisions, you need to evaluate your outlook on market opportunities. For highly conservative investors, stable interest may be more attractive than uncertain opportunities. However, for those willing to take some risk, locking all funds into long-term deposits may not be the optimal choice.

Frequently Asked Questions About TWD Time Deposits (FAQ)

Do I need to pay tax on interest from TWD time deposits?

Yes. According to tax regulations, deposit interest is classified as “interest income” and must be included in personal income tax filings. However, each individual has an annual “savings and investment special deduction” of TWD 270,000. This means that if your total interest income across all financial institutions does not exceed TWD 270,000, you generally will not need to pay tax. For most salaried individuals, this threshold is more than sufficient.

Will the principal and interest automatically roll over after maturity?

This depends on the agreement you made with the bank at the time of deposit. Typically, there are three options:

1. Principal rollover: Upon maturity, the interest is credited to your savings account, and only the principal is rolled over for another term at the prevailing rate.

2. Principal and interest rollover: Upon maturity, both principal and interest are combined into a new principal and rolled over, reflecting the concept of compound interest.

3. No rollover: Upon maturity, both principal and interest are transferred to your savings account.

It is generally recommended to choose “principal and interest rollover” to maximize long-term compounding effects.

Should I choose a one-year or three-year time deposit?

The choice of deposit term should be based on your “fund usage” and expectations of “future interest rate trends”.

Fund usage: If the money may be needed within one year (e.g. for a car purchase or travel), choose a one-year term. If the funds are for long-term savings (e.g. retirement or education), consider a three-year term to lock in the rate.

Interest rate outlook: As mentioned earlier, if rate hikes are expected, opt for shorter terms (e.g. one year) so you can reinvest at higher rates later. If rate cuts are expected, choose longer terms (e.g. three years) to lock in current higher rates.

Are digital banks’ TWD time deposit rates really higher? What should I watch out for?

Yes. Digital banks often offer very attractive high-yield savings or time deposit promotions to attract new customers, with rates typically higher than traditional banks. However, these promotions usually come with “conditions”, such as:

1. Deposit cap: High rates may only apply up to a certain amount, such as TWD 100,000 or TWD 300,000.

2. Time limit: Promotional rates may only last for 3 to 6 months.

3. New customer requirement: Some high-rate offers are only available to new account holders.

Be sure to carefully review all terms and conditions before applying to ensure you can fully benefit from the promotion.

Conclusion

In summary, TWD time deposits are a stable cornerstone in asset allocation, particularly suitable for conservative investors or as a parking place for emergency funds. Through the comprehensive TWD time deposit rate comparison and TWD investing risk assessment in this article, you can see that choosing a bank with both competitive rates and strong credibility is crucial, while also being aware of potential risks such as inflation, early termination, and opportunity cost. Start planning your first high-yield time deposit today based on your financial goals and risk tolerance!