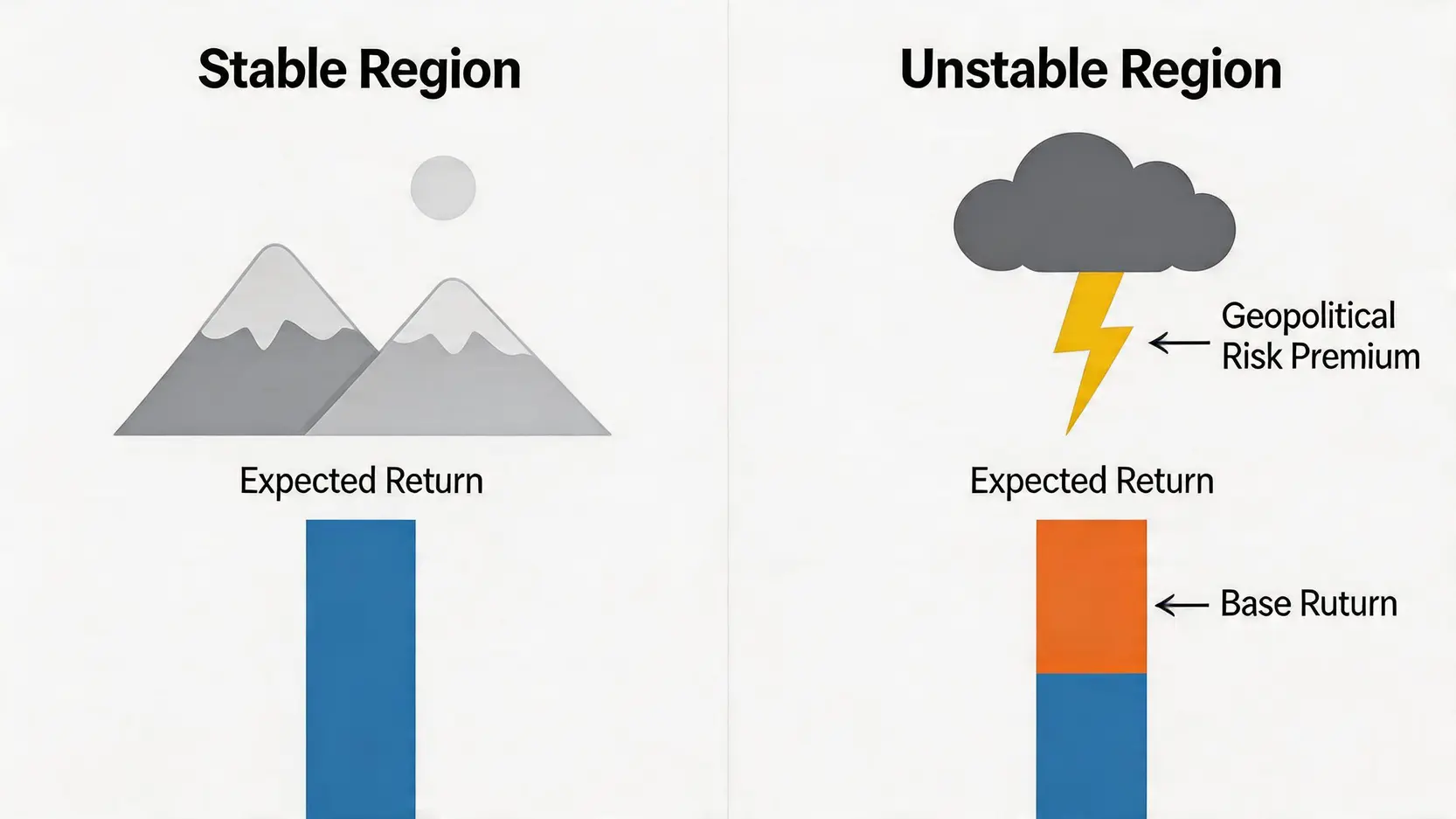

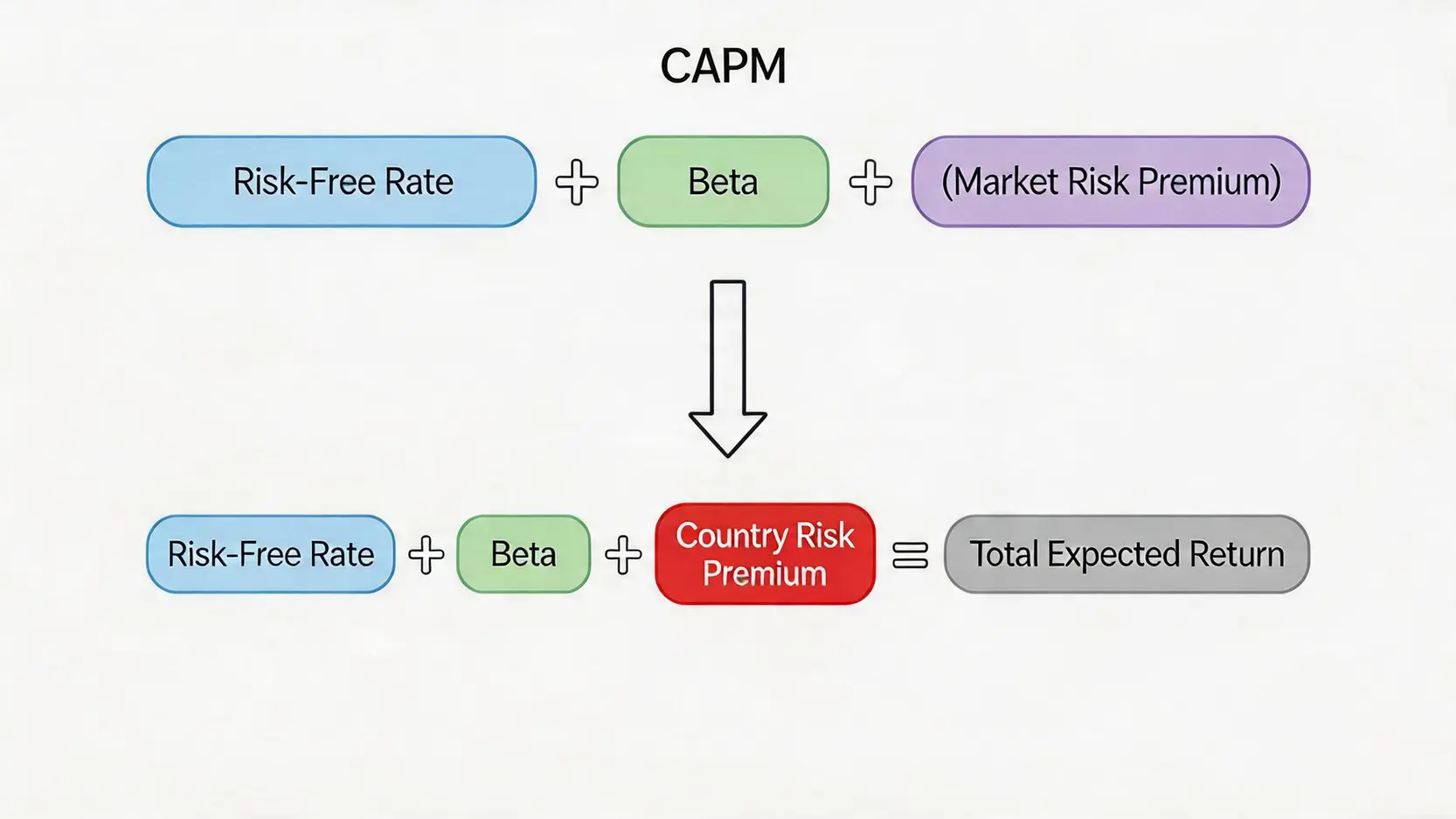

In the adjusted CAPM model, an additional Country Risk Premium (CRP) is added on top of traditional market risk to reflect geopolitical uncertainty.

Here, the Country Risk Premium (CRP) is the key variable used to capture geopolitical risk. It represents the total additional risk required to invest in a specific country (compared to a mature and stable market such as the US), and this includes geopolitical risk.

Key Variable Estimation: How to Derive and Apply Country Risk Premium (CRP) for a Specific Market

Estimating the country risk premium is one of the most challenging parts of investment risk premium calculation. Below are two commonly used methods:

- Sovereign Bond Default Spread Method: This is a relatively straightforward approach. It is calculated by subtracting the yield of a US (or German) government bond with the same maturity from the yield of a sovereign bond issued by that country in US dollars (or euros). This spread reflects the market’s pricing of sovereign default risk, which implicitly incorporates an assessment of political and economic stability.

For example: If Brazil’s 10-year USD bond yield is 8%, while the US 10-year Treasury yield is 4%, the sovereign bond spread is approximately 4%.

- Relative Equity Volatility Method: This method, popularized by valuation expert Aswath Damodaran, is more precise. It considers not only the bond market’s view but also incorporates stock market volatility.

CRP = Sovereign Bond Default Spread * (Annualized Standard Deviation of the Country’s Equity Market / Annualized Standard Deviation of the Country’s Sovereign Bond Market)

The logic behind this formula is that a country’s stock market is usually more volatile than its bond market, so the volatility ratio is used to adjust the spread, providing a more accurate reflection of the risk faced by equity investors.

In practical application, investors can refer to country risk premium data regularly published by authoritative institutions such as the NYU Stern School of Business, and directly input these values into valuation models, making investment risk premium calculations more aligned with real market conditions.

For example, when evaluating a company located in the Middle East, even if its business is unrelated to oil, you still need to include the country risk premium in the CAPM model to reflect the potential impact of regional conflicts on its operating environment, supply chain, and even legal stability. Just as Middle East conflicts often trigger global oil price volatility, studying crude oil investment fundamentals can also help you better understand how geopolitical risk is transmitted through commodity markets into the global economy.

Frequently Asked Questions (FAQ)

Q: Where can I find the latest data for the Geopolitical Risk Index (GPR)?

A: The original GPR data and charts are typically available on the personal website of its creator, Dario Caldara, or on relevant research pages of the Federal Reserve Board. In addition, professional financial data providers such as Bloomberg, Reuters, and certain academic research databases also periodically update or reference this data.

Q: Is the calculation of risk premium absolutely precise? What are the limitations?

A: No, it is not absolutely precise. Any model-based calculation has its limitations. First, the CAPM model itself is based on several assumptions (such as market efficiency and rational investors), which may not fully hold in the real world. Second, the estimation of Country Risk Premium (CRP) relies on historical data and may not fully capture sudden “black swan” events. Therefore, the result should be treated as a rational “anchor” rather than absolute truth, and should be combined with qualitative analysis (such as policy direction and leadership behavior) for comprehensive judgment.

Q: Besides equities, how does geopolitical risk affect bond and real estate markets?

A: The impact is significant. In the bond market, rising geopolitical risk can lead to a downgrade in sovereign credit ratings, causing yields to spike (and prices to fall) as investors demand higher compensation for default risk. In the real estate market, prolonged geopolitical instability can deter foreign direct investment (FDI), leading to capital outflows and negatively affecting commercial property and high-end residential demand. Conversely, countries perceived as “safe havens” may benefit from inflows of capital into their real estate markets.

Q: How can individual investors respond to increasingly frequent geopolitical risks?

A: Individual investors can adopt the following strategies to manage risk:

- Global diversification: Avoid over-concentrating assets in a single country or region by investing in global ETFs or funds to spread geopolitical risk.

- Allocate safe-haven assets: Include a certain proportion of traditional safe-haven assets such as gold, US dollar, or Swiss franc in the portfolio to provide a buffer during market turbulence.

- Focus on sector impact: Analyze how different geopolitical events affect specific industries. For example, defense, energy, and cybersecurity sectors may benefit during certain conflicts, while aviation and tourism may be negatively affected.

- Maintain a long-term perspective: Avoid frequent trading based on short-term political news. Focus on the long-term value of quality assets rather than trying to predict every political crisis outcome.

Conclusion

In summary, understanding and mastering geopolitical risk premium pricing methods is a key skill for navigating today’s volatile markets. This is not merely an academic exercise but a practical strategy that directly affects investment outcomes. By applying tools such as the Geopolitical Risk Index (GPR) for quantitative analysis and incorporating the adjusted Capital Asset Pricing Model (CAPM) for investment risk premium calculation, you can more accurately assess potential returns and hidden risks. Remember, successful investing is not about completely avoiding risk, but about learning how to price it properly. Apply these strategies to your investment analysis process and protect your assets in an uncertain world.