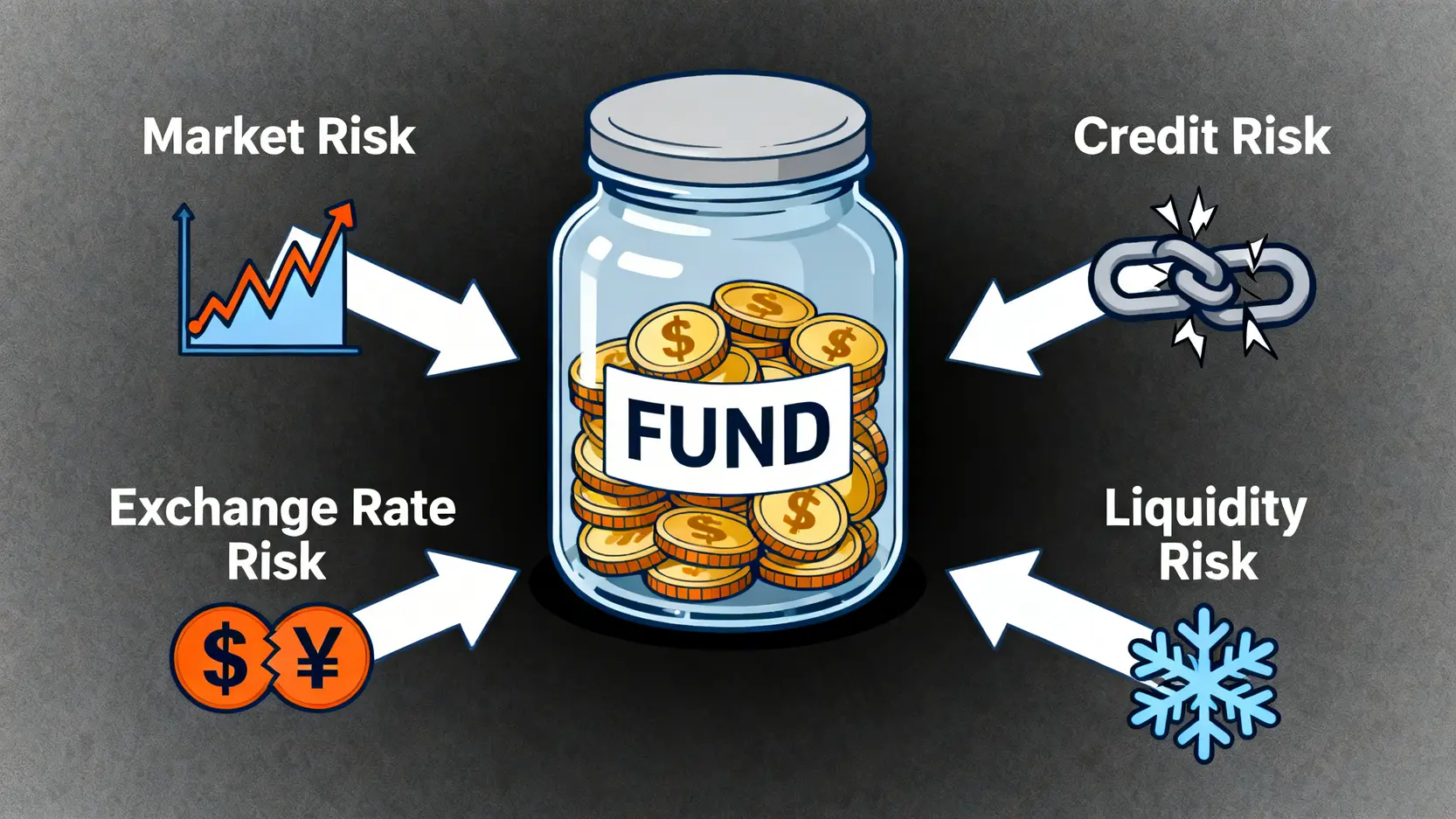

The four core risks faced in fund investing affect your assets from different dimensions.

Market Risk: The Inevitable Challenge of Economic Fluctuations

Market risk is the most common risk and is also known as systematic risk. It originates from changes in the overall economic environment, such as interest rate movements, economic recessions, inflation pressures, and political instability. When the broader market environment deteriorates, even the strongest company stocks or bonds may decline, affecting the fund NAV. This type of risk cannot be completely eliminated through diversification within a single asset class and is something all investors must face.

Credit Risk: A Hidden Concern Particularly for Bond Funds

Credit risk mainly exists in bond funds. It refers to the risk that the bond issuer (which may be a government or a corporation) fails to pay interest or repay the principal on time, also known as “default risk”. If a bond held by a fund defaults, its value will decline significantly. Generally, government bonds have extremely low credit risk, while high-yield bonds (also known as junk bonds) carry relatively higher credit risk. Therefore, before investing in a bond fund, it is important to review the credit rating distribution of its portfolio. To understand bond-related risks in greater depth, you may refer to 2025 US Treasury Investment Guide: Understand What US Treasuries Are and How to Buy Them.

Exchange Rate Risk: A Required Lesson When Investing in Overseas Funds

When the fund you invest in is denominated in a foreign currency, you face exchange rate risk (Exchange Rate Risk). For example, if a Hong Kong investor purchases a US equity fund denominated in US dollars, even if the fund itself performs well, a depreciation of the US dollar against the Hong Kong dollar would reduce the actual return when converting profits back into Hong Kong dollars and may even turn gains into losses. For investors with globally diversified portfolios, exchange rate fluctuations are one of the key variables affecting final returns.

Liquidity Risk: Why Sometimes a Fund Cannot Be Sold Even If You Want to Sell It?

Liquidity risk (Liquidity Risk) refers to the risk of being unable to sell assets quickly at a reasonable price when needed. Some funds may invest in stocks with low trading volume, unlisted companies, or certain types of bonds. When panic selling occurs in the market, fund managers may find it difficult to sell these assets quickly to meet investor redemption requests. This may eventually result in redemption delays or forced sales of assets at extremely unfavorable prices, thereby harming the fund NAV.

Further Reading (Strongly Recommended)

What Are Bond Risks? A Comprehensive Analysis of Fund Investment Risks With Risk Management Strategies

2025 US Treasury Investment Guide: Understand What US Treasuries Are and How to Buy Them

Practical Application: How to Perform Fund NAV Lookup?

After understanding the risks, the next step is to learn how to track and evaluate fund performance. Fund NAV lookup is a fundamental task that should be performed regularly, as it is the most direct indicator for measuring fund value.

What Is Fund NAV? Why Is It Key to Evaluating Performance?

Fund Net Asset Value (NAV) represents the asset value of each unit of a fund. Its calculation formula is:

(Total Fund Assets – Total Fund Liabilities) / Total Fund Units Issued

NAV is usually calculated and published after the close of each trading day. It reflects the real-time market value of all assets within the fund portfolio. Observing the long-term NAV trend chart allows investors to clearly understand the fund’s growth trajectory, volatility level, and performance across different market cycles. A consistently and steadily rising NAV curve usually indicates strong fund management capability.

Commonly Used by Hong Kong Investors: 3 Recommended Platforms for Fund NAV Lookup

There are many reliable channels for checking fund NAV. The following are several commonly used platform types among Hong Kong investors:

- Fund company official websites: The most accurate and up-to-date source of information. Every fund company publishes the daily NAV of all its funds on its official website.

- Major financial information websites: Platforms such as Bloomberg, Reuters, and local financial media websites usually provide comprehensive fund databases, allowing investors to compare products across different companies.

- Independent fund rating agencies: Platforms such as Morningstar not only provide NAV data but also offer in-depth analysis, ratings, and historical performance information, making them one of the best tools for researching funds.

Selecting Quality Funds: How to Interpret Fund Performance Rankings?

Among the many funds available, how can you quickly identify potential top performers? Fund performance rankings provide an objective reference standard, but they must be interpreted wisely to avoid the common mistake of focusing only on short-term returns.

Where Can You Find Authoritative Fund Performance Rankings? (For Example Morningstar)

To find authoritative fund rankings, internationally recognized independent rating agencies are the preferred sources. Among them, Morningstar is widely regarded as the industry gold standard. It evaluates funds based on risk-adjusted returns and assigns star ratings (from one star to five stars), with five stars being the highest rating. In addition, many major banks and brokerage trading platforms integrate these ranking data, allowing clients to filter funds directly.

The Wisdom of Interpreting Rankings: Short-Term vs Long-Term Performance, Which Matters More?

One of the most common mistakes made by beginner investors is chasing short-term “top-performing funds”. However, strong short-term performance (such as over three months or one year) may simply result from good timing or benefiting from a specific market trend. What truly reflects the strength of a fund management team is long-term and consistently stable performance.

Investment Philosophy: Rather than focusing on a short-distance champion, it is better to choose an experienced marathon runner. When screening funds, priority should be given to whether the fund’s ranking over the past 3, 5, or even 10 years has consistently remained within the top 25% among similar funds (commonly referred to as being in the top quartile of the “quartile ranking”). Such funds usually indicate that their investment strategy can withstand the cycles of bull and bear markets.

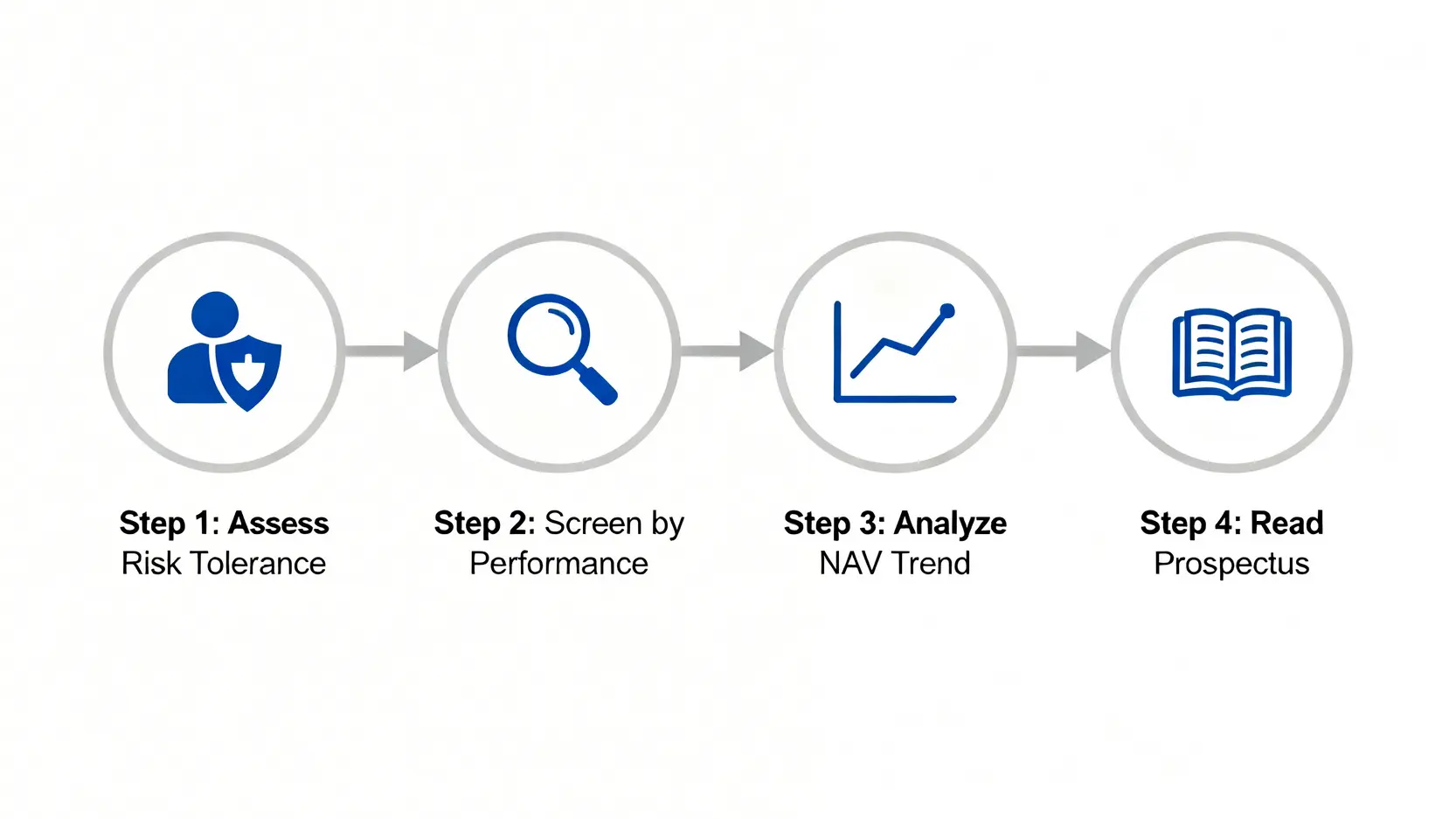

Comprehensive Evaluation: Combine Indicators in Four Steps to Select the Most Suitable Fund for You

After mastering the knowledge above, you can integrate it into a clear four-step screening process to help you select the most suitable fund from the beginning.