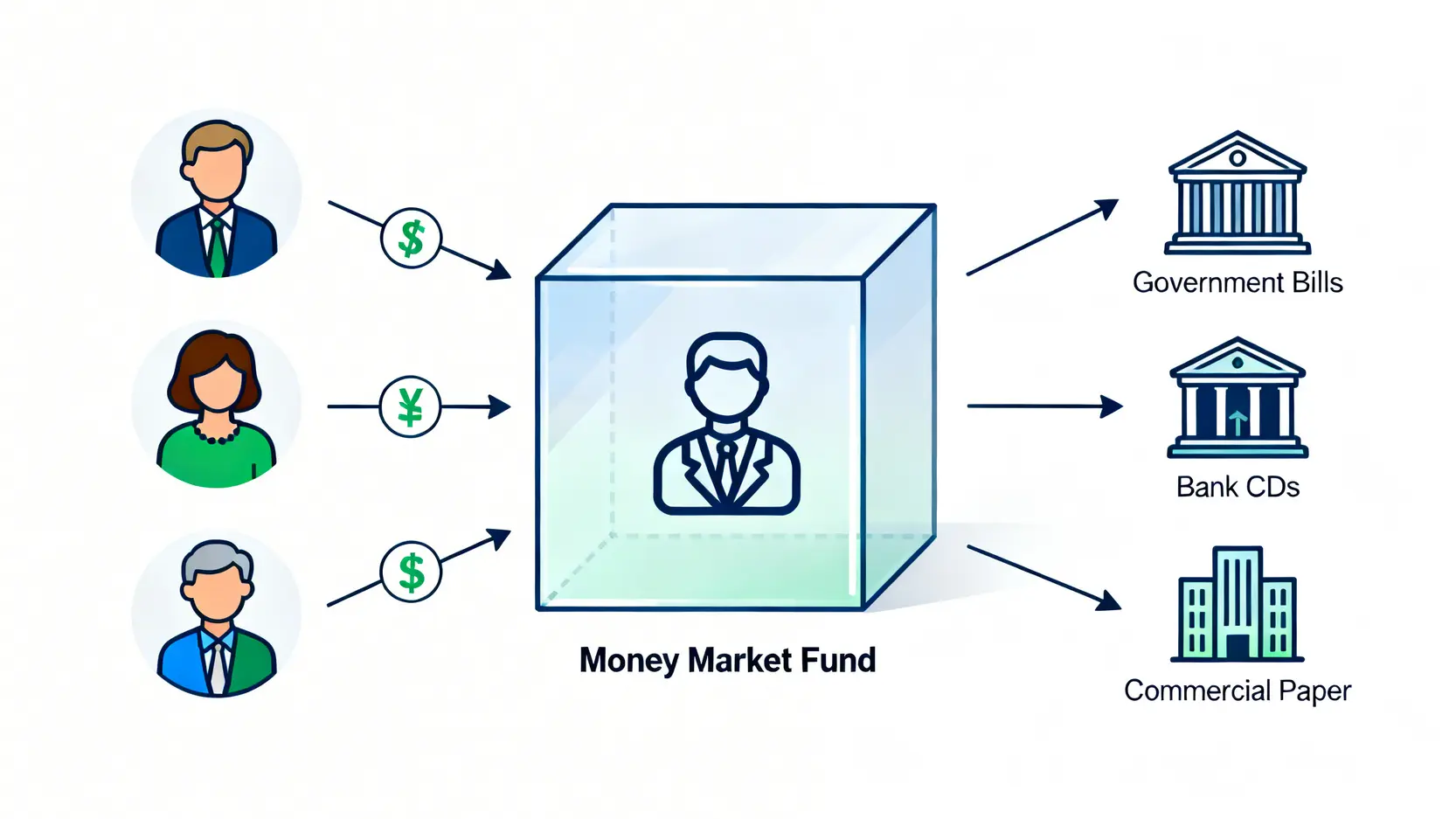

Use money market funds as a cash transit hub to ensure every idle dollar continues to grow.

After understanding the risks and returns, let us now look at how money market fund uses can play a role in your financial planning. It is not just a savings tool, but also an efficient cash management hub.

Use 1: A Growth Tool for Short-Term Idle Funds

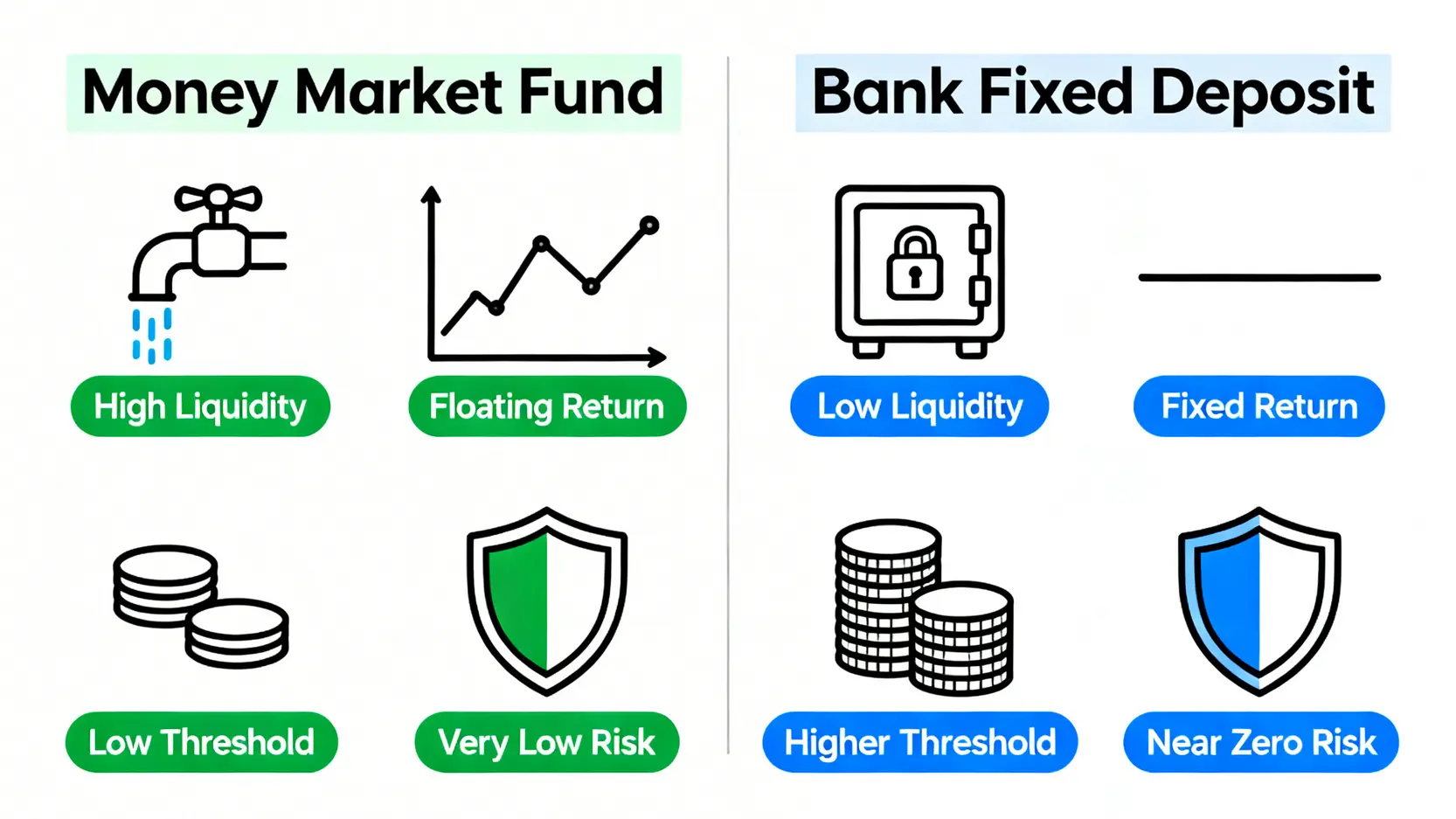

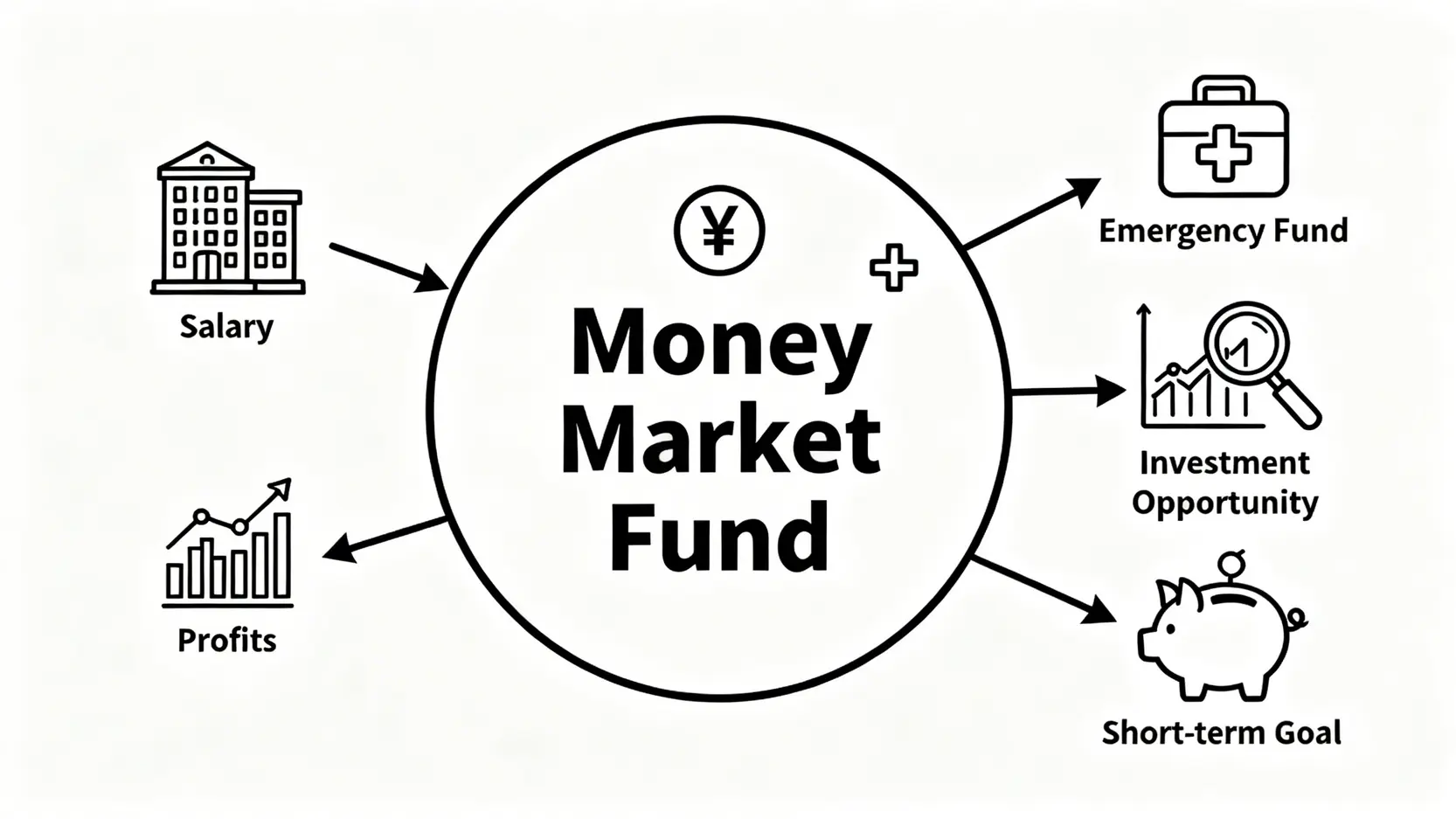

For funds that remain temporarily unused after receiving your salary, money set aside for insurance premiums or tax payments, or even a budget reserved for upcoming expenses, leaving them in a savings account yields almost no return. By transferring these funds into a money market fund, even if held for just a few days or weeks, you can earn returns several or even dozens of times higher than a savings account, truly achieving the effect of “accumulating small gains into a larger sum”.

Use 2: Building a Highly Liquid Emergency Reserve

Financial experts often recommend setting aside 3-6 months of living expenses as an emergency fund. The key for this fund is “safety” and “immediate accessibility”. Traditionally, people place this in savings accounts, but this means giving up the time value of money. By placing your emergency fund in a money market fund, you can maintain high liquidity while allowing the funds to continue growing and combating inflation.

Use 3: A Capital Transit Hub While Waiting for Market Entry Opportunities

Stock market fluctuations require patience to identify good entry points. When you take profits from selling stocks or are waiting for a market correction, you may hold a large amount of cash. Parking these “reserves” in a money market fund avoids idle funds and ensures that when opportunities arise, you can quickly redeem the funds (usually settled on T+1) and deploy them into the market, achieving “both offense and defense”.

Use 4: A Stable Core in Conservative Investment Portfolios

For investors with lower risk tolerance, or when building an investment portfolio, money market funds serve as an excellent stabilizing component. They can act as the cash portion of a portfolio, helping to reduce overall volatility. During market downturns, their stability provides a buffer; when rebalancing is needed, they provide sufficient liquidity.

How to Buy and Sell Money Market Funds in Hong Kong? Comparison of Three Main Channels

In Hong Kong, investing in money market funds is very convenient, mainly divided into the following three channels, each with its own advantages and disadvantages.

Further Reading (Highly Recommended)

2026 Hong Kong High-Interest Savings Accounts and Credit Cards Guide

Through Securities Platform Apps (for example: Futu “Cash Plus”)

- Advantages: Extremely convenient operation, seamlessly integrated with stock trading accounts. Deposits and redemptions usually incur no fees, with fast redemption speed. Some platforms allow instant redemption for stock trading use. Very low entry threshold, suitable for beginners and active traders.

- Disadvantages: Limited fund selection, mainly consisting of products from a few large fund companies partnered with the platform.

Through Robo-Advisors (for example: Stashaway Simple™)

- Advantages: Designed specifically for cash management, with a simple interface and one-click operation. Usually selects the most competitive money market funds in the market for clients, eliminating the need for personal research.

- Disadvantages: May charge a certain percentage of management fees (although typically low) and redemption time may be slightly longer than securities platforms.

Through Traditional Banks or Fund Companies

- Advantages: Offers a very wide selection of funds, providing access to products from different fund companies. Professional relationship managers are available to provide consultation.

- Disadvantages: Subscription and redemption processes may be more complex, requiring form submissions or operation through online banking fund platforms. There are more types of fees, such as subscription fees, redemption fees, and platform fees, which may erode returns.

FAQ Frequently Asked Questions

Q: Is there a chance of loss when investing in Hong Kong money market funds?

A: Theoretically possible, but the probability is extremely low. Historically, only in extreme financial crises (such as 2008) have a very small number of money market funds fallen below par value. For funds investing in high-quality short-term government and corporate debt, the risk of capital loss is minimal. Choosing funds managed by large and reputable fund companies can further reduce risk.

Q: Are returns from money market funds distributed daily?

A: Returns are calculated daily, but are usually settled monthly and reinvested as “dividend reinvestment”, increasing your fund units. Therefore, you will notice an increase in your fund units at the beginning of each month, which represents the interest earned.

Q: What fees are involved in purchasing money market funds in Hong Kong?

A: The main fees are “management fees” and “custodian fees”, which are deducted daily from the fund assets. The annualized return you see is the net return after these fees. Through securities platforms or robo-advisors, there are usually no additional subscription or redemption fees, but purchasing through traditional banks may involve such charges. It is important to fully understand the fee structure before investing.

Q: What is the difference between Hong Kong dollar money market funds and US dollar money market funds?

A: The main difference lies in the currency and underlying assets. Hong Kong dollar money market funds invest in HKD-denominated short-term debt instruments, with returns mainly influenced by the Hong Kong Interbank Offered Rate (HIBOR). US dollar money market funds invest in USD assets, with returns closely linked to the US federal funds rate. Under the linked exchange rate system, the interest rate trends of both are highly correlated, but short-term spreads may occur due to market supply and demand.

Conclusion

In summary, Hong Kong money market funds, as an efficient cash management tool, offer high liquidity and relatively stable returns, making them a strong alternative to traditional bank deposits. They are particularly suitable for investors seeking low risk and flexible capital allocation, whether used as an emergency reserve, a holding place for funds while waiting for market entry opportunities, or a stabilizer in conservative investment portfolios, all of which play an important role. With a clear understanding that they are not risk-free, making good use of the various functions of money market funds can effectively enhance your capital efficiency. Review your cash allocation now and discover the growth potential that money market funds can bring.