Total Return = Capital Gains (Price Difference) + Dividend Income

Annualized Return: How to Fairly Compare Different Investment Products

If you invest in product A for 3 years and earn 30%, and invest in product B for 5 years and earn 45%, which performs better? This is where annualized return becomes useful. It converts returns over different periods into a comparable annual average.

- Formula: Annualized return = [(1 + total return)^(1/number of years)] – 1

Example:

Continuing the example, assume product A has a total return of 30% (1.3) over 3 years, and product B has a total return of 45% (1.45) over 5 years.

- Product A annualized return = [(1.3)^(1/3)] – 1 ≈ 9.14%

- Product B annualized return = [(1.45)^(1/5)] – 1 ≈ 7.71%

After calculation, although product B has a higher total return, product A actually has better annual growth efficiency. For more details on annualized return calculations and applications, you can refer to this leveraged investment guide: Can You Make Money by Borrowing to Invest? 5 Key Steps and Risk Analysis.

Practical Tools Recommendation: Popular Fund Return Rate Inquiry Websites and Calculators

While manual calculation helps you understand the principles, using tools can improve efficiency. The following are some widely recognized resources:

- Fund company official websites and prospectuses: The most authoritative sources, providing historical performance and fee structures.

- Broker or bank apps: Most platforms offer basic portfolio return analysis functions.

- Third-party financial data websites: Morningstar is a globally recognized fund rating and data provider, offering detailed fund information, including historical returns, risk ratings, and expense ratio analysis, making it an essential tool for professional investors.

Further Reading (Highly Recommended)

Gold Investment Beginner Guide: Analysis of 5 Major Channels, Advantages, and Risks

Fund Trading Process Guide: From Subscription to Redemption, Master 5 Key Steps (With Fee Overview)

The Devil Is in the Details: How the Total Expense Ratio Erodes Your Returns

After learning how to calculate returns, the next step is controlling costs. The total expense ratio (TER), also known as the “internal expense ratio”, is a key factor affecting long-term returns, yet often overlooked by beginners.

What Is the Total Expense Ratio (TER)? What Hidden Costs Does It Include?

TER refers to the percentage of a fund’s total assets used annually to cover operational and management expenses. This cost is directly deducted from the fund’s net asset value, and investors do not receive a bill, making it easy to overlook. It mainly includes:

- Management fee: Paid to the fund management team for research and portfolio management, and usually the largest component.

- Custodian fee: Paid to financial institutions responsible for safeguarding the fund’s assets.

- Administrative fee: Covers accounting, legal, registration, transfer agent, and other operational expenses.

- Other costs: Such as audit fees, legal fees, and index licensing fees.

It is important to note that TER does not include transaction fees, subscription fees, redemption fees, or switching fees. These are “additional costs” that investors must pay separately.

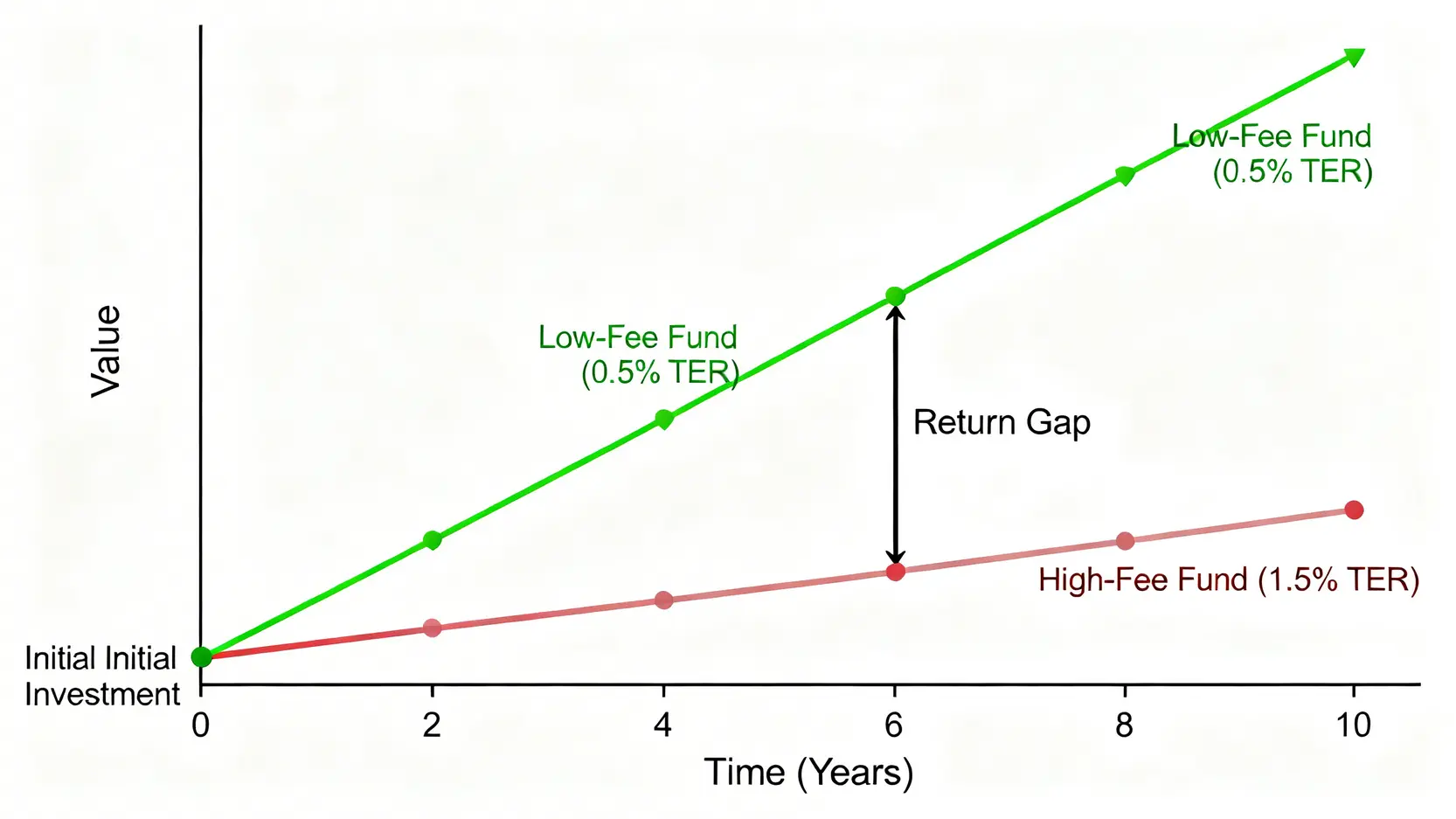

Case Study: How TER Gradually Impacts Returns Over 10 Years

Although fees may seem insignificant, under the effect of “compounding”, the long-term difference can be substantial. Consider a simple example:

Assume both Fund A and Fund B have an annual return of 8% (before fees). Fund A has a TER of 0.5%, while Fund B has a TER of 1.5%. If an investor invests 1,000,000 and holds for 10 years, what will be the outcome?

| Item |

Fund A (Low Cost) |

Fund B (High Cost) |

Difference

|

| Annualized Total Return |

8% |

8% |

– |

| Total Expense Ratio (TER) |

0.5% |

1.5% |

– |

| Investor’s Net Annualized Return |

7.5% |

6.5% |

– |

| Final Value After 10 Years |

Approximately 2,061,032 yuan |

Approximately 1,877,137 yuan

|

183,895 yuan |

A mere 1% difference in fees can result in a profit gap of over 180,000 after 10 years. If the time horizon extends to 20 or 30 years, this gap will grow exponentially. This is precisely why investment masters like Warren Buffett place such strong emphasis on low-cost investing.