When investing in warrants or futures, have you ever felt that an invisible hand in the market is controlling prices, commonly referred to as the “dealer”? In reality, behind this is a sophisticated and complex risk management mechanism operated by market makers. They are not simply betting against retail investors, but instead hedge risk through a strategy known as “Delta Hedging”, a warrant market maker hedging strategy that is also commonly used as a futures market making hedging approach. This article will fully unveil the mystery of warrant market makers and clearly explain the principles of dealer Delta Hedging, helping you understand the real logic behind the market.

Who Are the “Dealers”? Deconstructing the Hedging Role of Market Makers in Warrants and Futures

In financial markets, particularly in the derivatives sector, “dealers”, more professionally known as “market makers” play an indispensable role. They are the gears that keep the market operating, rather than the simple counterparty many retail investors imagine.

The Dual Role of Market Makers: Providing Liquidity and Managing Their Own Risk

Market makers have two core responsibilities, and these two roles are closely interconnected:

Providing liquidity: market makers simultaneously quote a bid price and an ask price, ensuring that there is always a trading counterparty in the market. Whether you want to buy or sell a specific warrant, the market maker has the obligation to take the opposite side of the trade. This significantly narrows the bid ask spread (Bid-Ask Spread), reduces trading costs for investors, and ensures the market does not stall due to the absence of counterparties.

Managing risk: when investors buy a Call warrant from a market maker, the market maker effectively holds a short position. If the price of the underlying asset rises, the market maker will face losses. To hedge this risk, they must adopt a series of complex hedging strategies, the most important of which is Delta Hedging. Their objective is not to bet on a single directional move, but to earn stable profits through the bid ask spread while managing risk.

Why Must Derivatives Markets (Warrants, Futures) Have Market Makers?

Unlike stocks, derivatives do not have a physical underlying asset supply, and their supply can be almost unlimited. Without market makers, an ordinary investor attempting to buy a specific warrant might not find any willing seller. The market would become extremely illiquid, and prices could experience large and unreasonable jumps, which would be fatal to overall market stability. Therefore, according to exchange regulations, every listed warrant must have a designated liquidity provider (namely a market maker) to ensure market fairness and efficiency.

Delta Hedging, also known as Delta neutral hedging, is the foundation upon which all derivatives market makers rely. Understanding it is equivalent to obtaining the key to interpreting dealer behavior. The core objective of this strategy is to reduce the “directional risk” of positions to the lowest possible level and achieve what is known as “Delta Neutral”.

Basic Concept of Delta: Measuring Sensitivity to Price Changes

In the world of options and warrants, Delta is a Greek letter (Δ) used to measure the sensitivity of a warrant’s price relative to changes in the underlying stock price. Its value ranges between -1 and 1.

Call Warrant: Delta is positive (0 to 1). For example, if a Call warrant has a Delta of 0.5, it means that for every 1 unit change in the underlying stock price, the theoretical price of the warrant will change by 0.5 units.

Put Warrant: Delta is negative (-1 to 0). For example, if a Put warrant has a Delta of -0.4, it means that for every 1 unit change in the underlying stock price, the theoretical price of the warrant will move inversely by 0.4 units.

Simply put, Delta represents the “speed” at which a warrant follows movements in the underlying stock. The deeper in the money a warrant is, the closer the absolute value of Delta is to 1. The further out of the money it is, the closer the absolute value of Delta is to 0.

How Is Delta Neutral Achieved? Practical Hedging Operations Using Stocks or Futures

The objective of market makers is to keep the total Delta value of their entire portfolio as close to 0 as possible, known as “Delta Neutral”. In this way, regardless of whether the underlying stock price rises or falls, the overall value of their portfolio theoretically remains relatively stable, thereby locking in profits. They operate as follows:

Hedging after selling Call warrants: suppose a market maker sells 1 million Call warrants of a certain stock to the market, each with a Delta of 0.6. The market maker’s Delta exposure is then -600,000 (-1,000,000 × 0.6). To hedge, the market maker must buy 600,000 shares of the corresponding underlying stock in the market (Delta equals 1), making the total Delta equal to -600,000 + (600,000 × 1) = 0.

Hedging after selling Put warrants: if a market maker sells 1 million Put warrants with a Delta of -0.4, the Delta exposure becomes +400,000 (-1,000,000 × -0.4). To hedge, the market maker must short sell 400,000 shares of the corresponding underlying stock or related futures contracts so that the total Delta becomes +400,000 – (400,000 × 1) = 0.

Illustration: The Four Core Steps of Delta Hedging by Market Makers

This approach of “selling warrants while buying or selling the underlying stock” represents the essence of Delta Hedging. It also explains why, at times, a particular stock may experience significant buying or selling pressure near the market close without any news. This is often the result of market makers hedging warrants sold during the trading day.

Delta Hedging Example: A Popular Index Warrant

Let us illustrate with a more concrete example:

Product: A Call warrant tracking a major market index.

Parameters: Conversion ratio 10000:1, Delta equals 0.5.

Scenario: Market sentiment is extremely bullish, and a large number of investors buy this Call warrant. The market maker sells a total of 100 million units.

Hedging calculation: 1. Calculate the total Delta of the warrants: 100 million units / 10000 (conversion ratio) = equivalent to 10,000 index futures contracts. 2. Calculate Delta exposure: 10,000 × 0.5 (Delta) = 5,000. Because the market maker sold Call warrants, the Delta exposure is -5,000. 3. Execute the hedge: to neutralize Delta, the market maker must buy 5,000 index futures contracts in the futures market for hedging.

This operation not only protects the market maker from the risk of an index rise, but the substantial buying itself may also contribute to upward pressure on the index.

How Do Market Maker Hedging Activities Influence the Broader Market?

When thousands of market makers are simultaneously executing Delta Hedging, these independent hedging activities accumulate and can significantly influence overall market price movements. This is not only a technical process and can sometimes trigger chain reactions in the market.

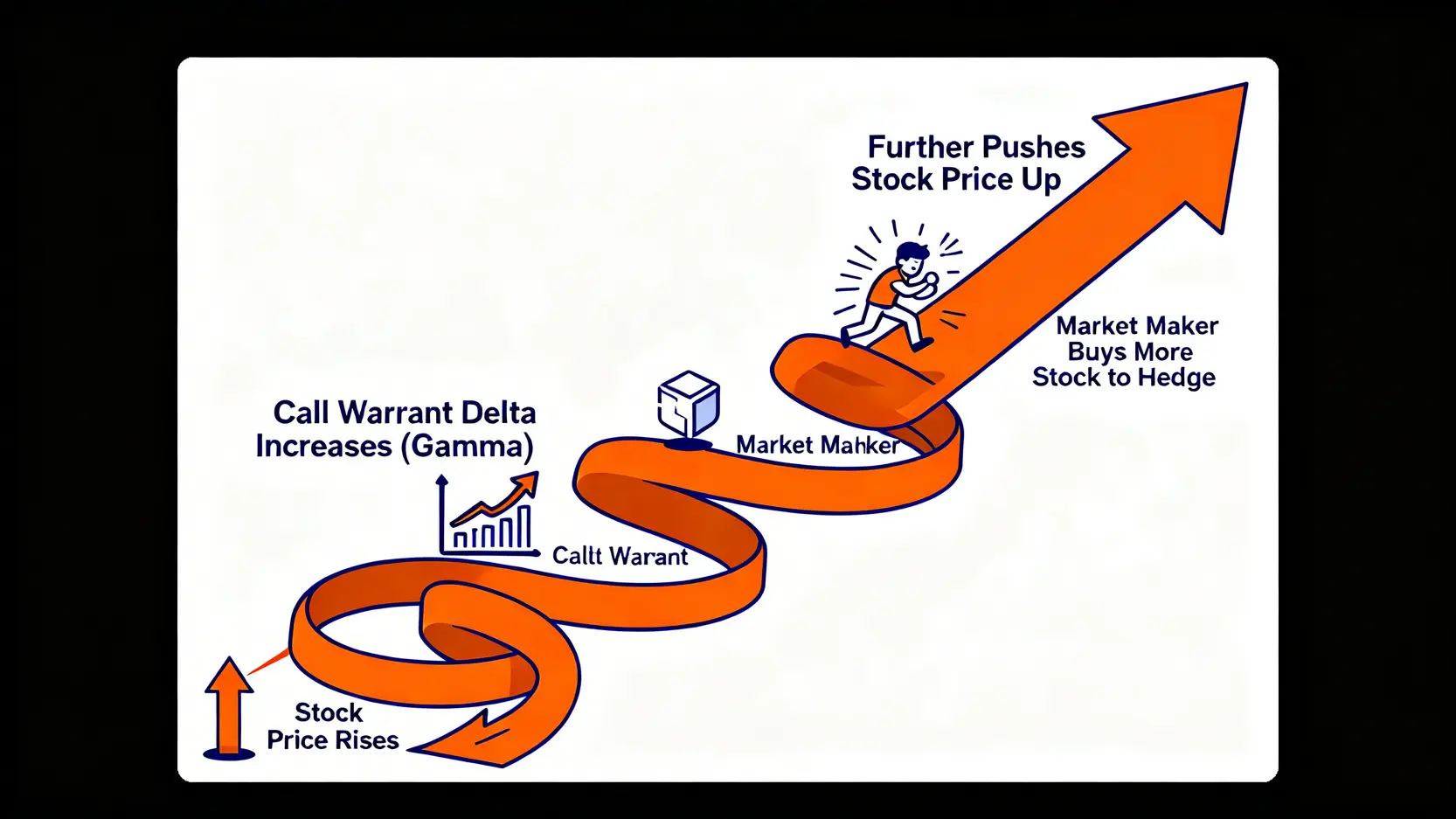

From Gamma Risk to Gamma Squeeze: When Hedging Triggers Market Chain Reactions

Here we introduce a more advanced concept: Gamma (Γ). Gamma measures the rate of change of Delta. In other words, Gamma is the acceleration of Delta.

When the underlying stock price rises, the Delta of Call warrants increases (for example from 0.5 to 0.6), while the negative Delta of Put warrants becomes smaller in magnitude (for example from -0.5 to -0.4).

Market makers must continuously adjust their hedging positions to maintain Delta neutrality, a process known as “Dynamic Hedging”.

Gamma Squeeze is the extreme manifestation of this dynamic hedging. When a large concentration of warrants or options gathers around a certain price level:

Suppose a large number of investors buy out of the money Call warrants on a stock. As the stock price begins to rise and approaches the strike price, the Delta of these Call warrants increases sharply (Gamma effect). Market makers who sold these Call warrants are forced to buy more underlying shares in the market to maintain hedging. This powerful buying pressure further pushes the stock price higher, causing Delta to rise even more and form a vicious cycle (or a virtuous cycle, depending on your position). This phenomenon is known as a Gamma Squeeze, which can produce sharp one directional market moves in a very short period of time.

Gamma Squeeze: A Market Accelerator Triggered by Hedging

As a Retail Investor, How Can You Identify Potential Trading Signals From Dealer Hedging Footprints?

Although retail investors cannot precisely know the positions of market makers, they can infer possible dynamics by observing certain public data and thereby gain trading inspiration:

Observe warrant or option open interest: the higher the open interest level at a certain price level, the greater the concentration of long and short forces. When prices approach these key levels, market maker hedging activity may become unusually active, amplifying market volatility.

Monitor changes in implied volatility: implied volatility reflects the market’s expectation of future volatility and is also a key factor used by market makers when pricing warrants. If the implied volatility of a warrant rises significantly without a major change in the underlying stock price, it may indicate that market makers expect greater future volatility or are adjusting their risk models.

Analyze capital flow during large trading days: when an index or individual stock experiences strong one directional movements, observe the inflow or outflow of funds into corresponding warrants. If a large amount of capital flows into warrants in one direction, the opposite hedging activity by market makers is likely to become very frequent, which may provide trend following opportunities for short term traders.

Conclusion

In summary, the “dealers” in the warrant and futures markets, namely market makers, have the core responsibility of providing market liquidity, and Delta Hedging is the key hedging strategy on which they rely to operate. Understanding this helps dispel misconceptions about dealers and allows us to view market volatility more rationally. Although retail investors cannot fully replicate the professional strategies used by market makers, observing clues from their hedging behavior, such as open interest distribution and changes in implied volatility, can provide deeper insight into market dynamics and help develop more comprehensive investment plans.

FAQ – Common Questions About Warrant Market Makers and Delta Hedging

Q: What are the sources of profit for market makers? Do they always make money?

A: The profits of market makers mainly come from three aspects: 1. Bid-Ask Spread: this is the most stable source of income. 2. Theta Decay: the value of warrants decreases as time passes, which benefits warrant sellers, namely market makers. 3. Vega Trading: they profit by trading implied volatility, buying when volatility is expected to expand and selling when volatility is expected to contract. However, market makers do not always profit. If the market experiences extreme gap movements (Gap Open), they may suffer significant losses because they cannot adjust hedging positions in time.

Q: Is it necessary for retail investors to learn and apply Delta Hedging?

A: For the vast majority of retail investors, directly applying Delta Hedging is neither practical nor necessary, as it requires substantial capital, complex calculation systems, and extremely low trading costs. However, understanding the concept of Delta Hedging is crucial. It helps you understand the deeper operating mechanisms of the market, identify potential trading opportunities or risks caused by market maker hedging behavior, and make more informed decisions.

Q: Are warrant prices arbitrarily controlled by dealers?

A: No. Warrant prices are mainly determined by a widely accepted option pricing model (such as the Black-Scholes model). The input variables include the underlying stock price, strike price, expiration date, interest rate, dividends, and implied volatility. Although market makers cannot arbitrarily set prices, they can adjust the key variable of “implied volatility” based on market supply and demand and their own risk conditions, thereby influencing the final quotation of the warrant. Therefore, their pricing is a professional adjustment within a defined framework of rules, rather than arbitrary control.

Q: What is the greatest risk faced by market makers?

A: The greatest risks for market makers are “gap risk” and “volatility risk”. When the market experiences a large gap up or gap down due to sudden news (such as earnings warnings or wars), the Delta Hedging strategy of market makers can instantly fail, because they cannot perform hedging adjustments along a continuous price path, which may result in significant losses. This is also why market makers typically raise the implied volatility of warrants before major announcements to compensate for the additional risk they bear.

US PPI Comes in Below Expectations: Is Inflation Cooling? Understand the Impact on the Stock Market, Interest Rate Hikes, and Your Wallet The recently released US Producer Price Index (PPI) once again came in below market expectations, sparking optimism that inflation is cooling. What exactly does this key US PPI...

PPI and CPI Surge: Is the Inflation Monster Coming? Understand the Two Key Indicators and Protect Your Wallet! Have you recently felt that your money is worth less and less, with the price of everything rising except your salary? Everyone is talking about “inflation”, but where exactly does this monster...

When Oil Prices Rise, Which Currencies Benefit? Understanding Investment Strategies for Crude Oil Currency Pairs What Are Crude Oil Currencies? Uncovering the Relationship Between Oil Prices and Forex As volatility in the global energy market intensifies, every movement in crude oil prices affects the foreign exchange market. For perceptive investors,...